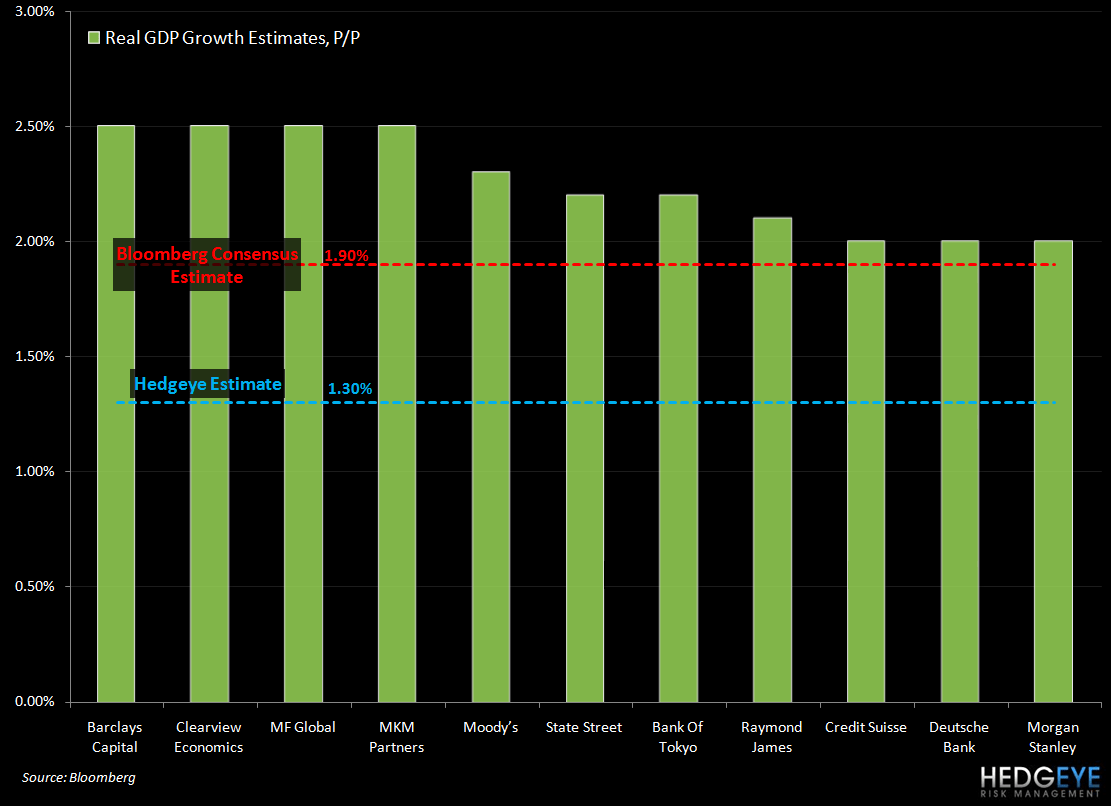

Conclusion: Looking at the macro data, it makes little sense to us that consensus 3Q GDP growth is at 1.9% (per Bloomberg). Retail Sales, Industrial Production, and Housing indicate to us that a sequential slowdown is more likely what occurred.

We cannot make sense of consensus. Can you?

As it stands currently, the consensus is showing 2Q GDP growth of 1.9% according to Bloomberg. Hedgeye is expecting growth of 1.3% and that number could be revised downward, with the potential for an outright contraction in the fourth quarter. The BEA is expected to release the advance estimate of 3Q GDP on Friday, October 29th. There is a significant chance that this GDP report is close to consensus expectations as it is the last major piece of economic data before the midterm elections. The economic data reported of late suggests that. However, reporting risk remains for a downside surprise to those expectations and here is why.

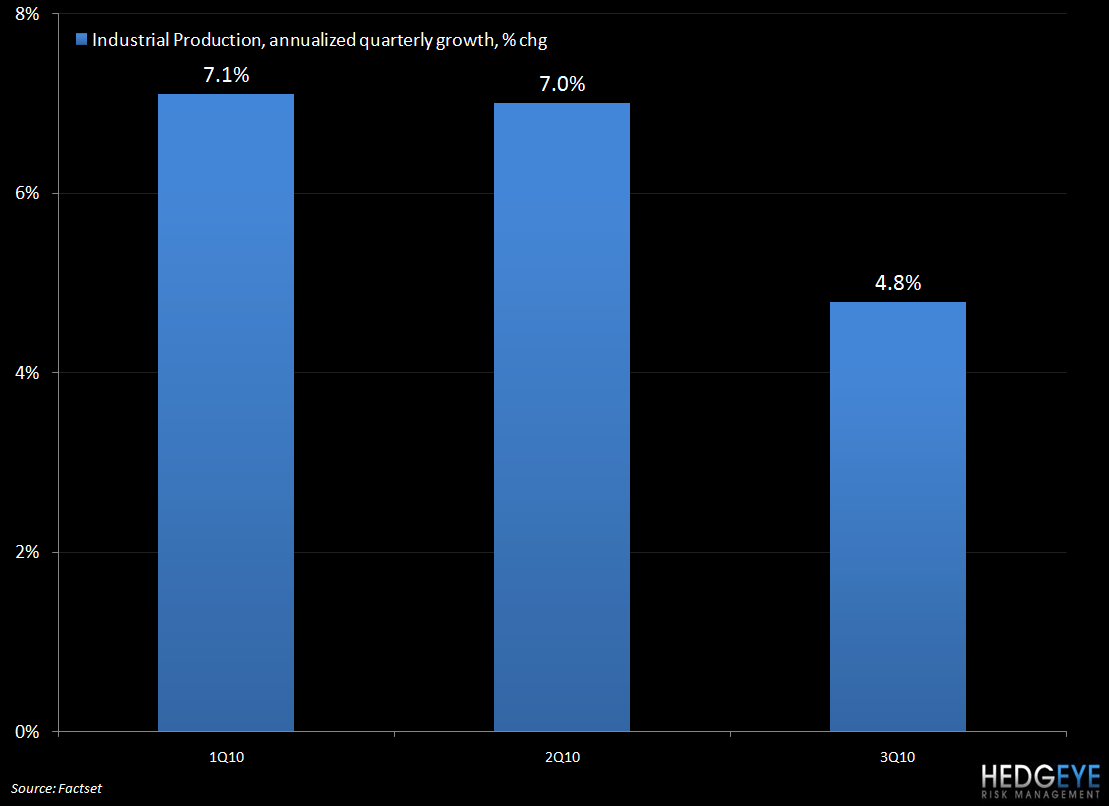

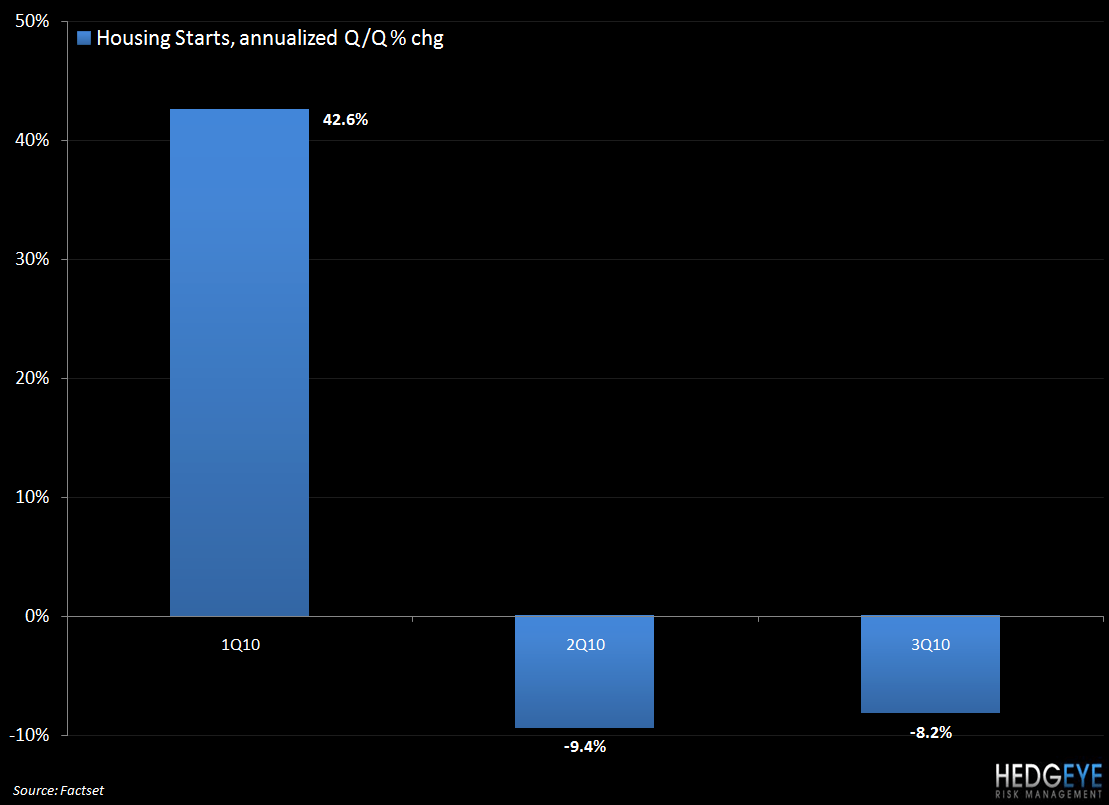

As you can see clearly from the charts below:

- 3Q10 retail sales slowed sequentially

- For the third-quarter, seasonally-adjusted industrial production reportedly grew at annualized pace of 4.8%, down from a 7.0% pace in the second-quarter.

- During the third-quarter, seasonally-adjusted housing starts contracted at an annualized pace of 8.16%, versus a 9.38% annualized contraction in the second-quarter.

In addition to all of this, the August trade deficit was definitely bad enough to reduce the upcoming estimate by nearly 1%. With a slowdown fully established, the need for inventory building also slows. From 1Q10 to 2Q10 the contribution to percentage change in real GDP from “change in private inventories” slowed from 2.64% to 0.82%; the 0.82% represented 47% of total GDP growth in the second quarter.

As a point of reference, when consumer demand contracted in the fourth quarter of 2008, the contribution to percentage change in real GDP from “change in private inventories” dived as low as -2.31%. Real GDP contracted 6.8% P/P in 4Q08.

Before we get the politicized GDP report a week from Friday, we will get two more data points on housing, both of which we think will be BOMBS. On Monday, we get the September existing home sales followed by new home sales on Wednesday. Hedgeye’s financials sector head, Josh Steiner, believes that next Tuesday’s Case Shiller print will be negative for home prices.

Lastly, on 9/27 we noted that new orders for durable goods were (as of July and August's data), seeing a sequential slowdown versus 2Q of 0.3%, while still growing ear-over-year. While the durable goods number missed overall expectations, when transportation and aircraft were stripped away it beat.

So how could all these institutions (shown in the chart below) have a 3Q GDP growth number above 2%? If you can offer explanation, please let me know.

Howard Penney

Managing Director