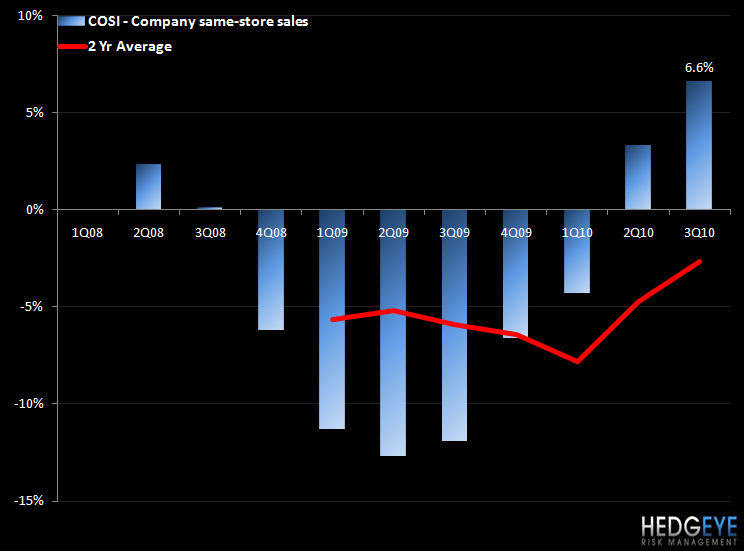

CONCLUSION: COSI released 3Q10 sales results last night; the results were impressive and support our bullish case.

Cosi same-store sales results came in strong for 3Q with company-owned stores seeing a 205 bp sequential improvement in two-year average trends as comparable sales grew 6.6% in the quarter. System-wide same-store sales grew 5.2% versus 3Q09. In early September, I wrote a note titled, "ALL ROADS POINT NORTH", and these results are right in line with that thesis.

Howard Penney

Managing Director