Conclusion: I remain bullish on a long-term basis but the stock is flashing overbought in the immediate term.

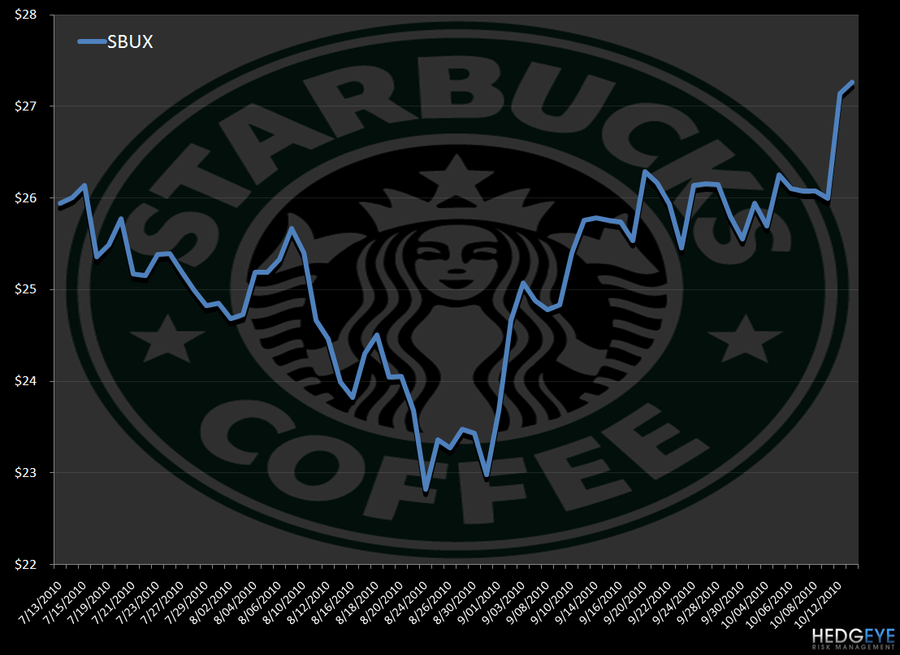

There seems to be lot of investor optimism going into SBUX ‘s fiscal 4Q10 earnings report scheduled to be released in three weeks on Thursday, November 4th after the market closes. In the last week alone, the stock is up over 5% and as shown below, for the second day this week, the company’s call options are active, trading up 225% today relative to the 20-day average. That being said, earlier this week on Tuesday morning, Keith’s model flagged the name as overbought in the immediate term.

I remain bullish on SBUX on a long-term basis and we are still long the name in the Hedgeye virtual portfolio as the company stands to benefit from continued leverage of its existing store base, international growth, its increased investment in marketing and its pursuit of additional platforms of growth (largely VIA and Seattle’s Best Coffee).

The timing of Keith’s overbought level being triggered lines up with my fundamental view as the company will be lapping its most difficult top-line comp and year-over-year EBIT margin comparisons of fiscal 2010 in its current fiscal 4Q10. For the past six quarters, the company has posted sequentially better comps on a one-year basis but I believe it is unlikely that the next reported quarter will continue that trend (reported +9% in 3Q10). I would not be surprised, however, to see the company post another quarter of sequentially better trends on a two-year average basis (SBUX needs to report a +4% comp or better in the U.S. to maintain two-year average trends from the third quarter). The company laps its first positive comp in the U.S. in 1Q11.

As same-store sales comparisons get increasingly more difficult in fiscal 2011, the company will also be facing higher costs. As we noted in our September 23rd post titled “SBUX – INFLATION FORCES STARBUCKS HAND”, these costs are becoming too high to absorb with the company recently announcing a need to raise some prices “due to the recent dramatic increases in the price of green arabica coffee, currently close to a 13-year high, as well as significant volatility in the price of other key raw ingredients, including dairy, sugar and cocoa.” The company reaffirmed its fiscal 2011 EPS guidance of $1.36 to $1.41, saying that the targeted price adjustments should mitigate the impact from more recent rising costs. For reference, the company’s guidance had anticipated a $0.04 per share hit from higher commodity costs, largely attributable to higher coffee prices.

I think same-store sales and margin growth will continue to materialize in FY11 but the rate of growth will slow and the company’s ability to continue to surprise to the upside from both top-line and bottom-line perspectives will likely diminish as expectations have caught up with the company (the street is already at $1.43 per share for FY11, $0.02 per above the high-end of management’s guided range).

Howard Penney

Managing Director