This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. This piece does not necessarily reflect the opinion of Hedgeye.

|

"A remarkable consensus has developed among modern central bankers ... that there's a new 'red line' for policy: a 2 percent rate of increase in some carefully designed consumer price index is acceptable, even desirable, and at the same time provides a limit. I puzzle at the rationale. A 2 percent target, or limit, was not in my textbooks years ago. I know of no theoretical justification." |

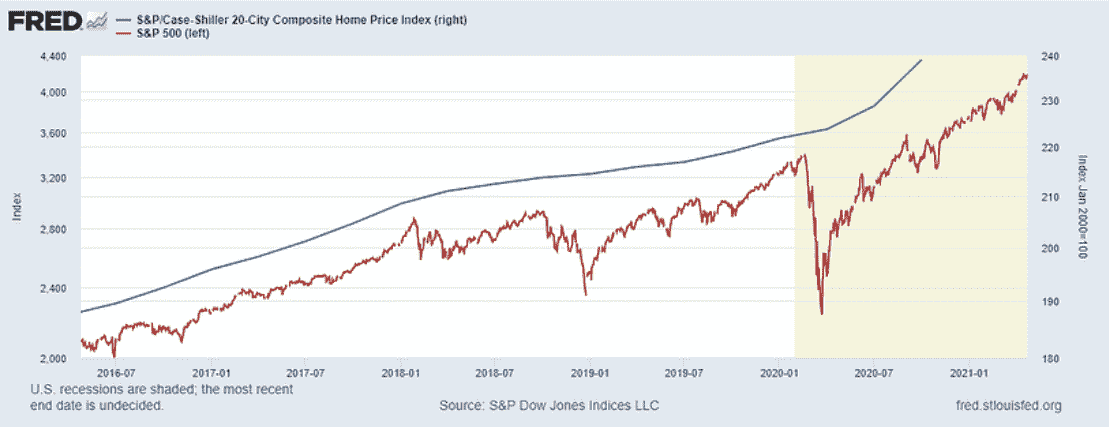

There is a growing awareness on Main Street that inflation is a problem. Everybody knows about the run-away markets for financial assets and single-family homes.

It seems that the stocks with the least substance are likely to benefit the most in the current interest rate environment. But vendors and suppliers are starting to raise prices in the face of scarcity in supply chains, the precursor to a significant increase in inflation.

The growing gap in valuations between different stocks is starting to drive a feeding frenzy, from SPACs to plain old M&A. Sometimes liquidity crazed buyers are taking out higher valued stocks.

Witness the spectacle of New York Community Bank (NYSE:NYCB), trading 10% below book value, taking out Flagstar Bancorp (NYSE:FBC) at a substantial premium over book.

And as our friend and fishing buddy Ed Pinto at AEI has long warned, the combination of low interest rates and easy credit from lenders is killing affordability and creating future credit losses for the Treasury.

Just in time, President Joe Biden is offering a $15,000 tax credit for first-time home buyers. This nonsensical policy will only make matters worse when these borrowers default in a couple of years. For the same reason, BTW, we just can't see NYCB keeping that gnarly FBC Ginnie Mae servicing book.

Of course, the common thread in this story is inflation, plain old excess demand for limited assets. Given that the elasticity of supply seems to have yet to reach a boundary, however, it appears that the culprit here is the excessive liquidity created by global central banks.

The financial markets, confirming Say’s Law, proves that creating assets of whatever dubious quality or substance generates demand. But the creation of liquidity by the Fed plays an important role besides merely dealing with short-term market volatility.

The creation of assets, some better than others, is part of the oldest part of the playbook for the Federal Open Market Committee, namely the recipe for avoiding global debt deflation. Irving Fisher’s famous work on “debt contraction deflation” is the masterpiece on the Great Depression and the foundation of later studies by which former Fed Chairman Ben Bernanke rescued the world in 2007.

“We must,” our friend Fred Feldkamp likes to remind us, “NEVER forget the Fisher/Bernanke combined lesson. It starts with the national income accounting identity that ‘savings’ must and always will equate with ‘investment’.

That is an “identity” because that is how we have constructed the world’s national income accounts. It says that the total of all debt and equity must (and always will) equate with the total of all capital investment.”

Debt is always an amount set by contract but it is necessarily a “value” that fluctuates with the market by its present value, determined by “base rate plus spread,” to establish the ultimate daily market value of debt. That’s why Treasury rates and bond spreads are vital data points.

They set the day-to-day value change of total debt. Equity markets are bid up and down by investors, based on expectations regarding earnings and other factors, including the perceived actual future cash flow burden of daily market values for debt.

When either equity or debt value “crashes” as in Q1 of 2020, the value of “savings” necessarily shrinks and that necessarily undermines the value of the world’s total “investment.” What Fisher showed (and Chairman Bernanke understood) is that capital assets necessarily crash in value unless debt grows to replace any sudden market value drop. Equity values recover when confidence is restored. We have seen that recovery over the past year.

But while Chairman Bernanke advocated aggressive action to combat debt deflation, he also understood that there were limits to the FOMC’s actions. In particular, the actions taken under Fed Chairman Janet Yellen have gone further than merely restoring balance between debt and equity. The FOMC, by doing too much for too long, now attacks the very pricing mechanisms upon which the capital markets and the US economy vitally depend.

First Yellen and then Fed Chairman Jerome Powell have increased the Fed’s purchases of debt even after any danger of generalized debt deflation has disappeared. More radical members of the FOMC such as Governor Lael Brainard focus on employment for the bottom quartile of the US workforce, yet the fact is that the Fed’s job is to ensure full employment generally not in particular.

The whole point of the political compromise that led to the Humphrey-Hawkins legislation of half a century ago was not to guarantee a job for every US citizen. Perhaps Yellen and Powell should go back and read the statute as passed by Congress. Sadly, Treasury Secretary Yellen and Chairman Powell have become so cowed and politicized that they are no longer able to carry out their duties under the law.

Secretary Yellen prattles on in public about the risk of global warming, but ignores the growing sea of fraud in global financial markets. Archegos, Wirecard and Greensill, to name but three prominent financial schemes.

All of these financial failures are all the result of the FOMC’s excessive actions and the impact on risk perception by investors. These frauds have caused billions in losses to financial institutions, but Yellen and Powell remain clueless and indifferent to their legal duties as regulators.

There is no question that the FOMC needed to “go big” in December 2018 and in April of 2020. Yet none of the current members of the FOMC seem to have the personal or political courage to say no to political fashion when enough has been done. The triple mandate in the Humphrey Hawkins statute says full employment and price stability, and also stable interest rates. By failing to moderate monetary policy when these goals have been met, the FOMC is creating an inflation problem in the future.

“[W]ith the Fed undertaking one of the most radical monetary policy experiments in history, you’d think there would at least be more debate,” notes The Wall Street Journal. “All the focus on race and gender obscures that what really matters at the Fed is the value (not the color) of money.” But the bigger threat is to the credibility of the central bank.

Two decades ago, former Federal Reserve Board Chairman Alan Greenspan and his colleagues on the FOMC presided over the lowest interest rates since WWII. The terrorist attack on September of 2001 had spurred the central bank to reverse course and ease tighter policy put in place to cool the financial bubble in technology stocks. The reason for this change in interest rate policy was to arrest any negative economic response from the dastardly attack on 9/11.

But the long-term negative impact of that decision by the Greenspan Fed continues to color our economic life two decades later. No matter your good intentions as a central banker, attempting to fine tune the economy is a dangerous act of folly, especially after a major disruption such as 911 or COVID.

The bond market is delivering this message to Chairman Powell, but in the ridiculous political climate in 2021, we seem doomed to repeat past mistakes over and over again. Each excessive injection of liquidity provided by the FOMC in response to a major externality such as COVID creates the conditions for the next financial crisis, in this case a maxi housing price reset in 2024 or 2025.

At the end of the day, financial stability is a function of both Fed action to address the clear and present danger of debt deflation and also moderation to maintain some semblance of price stability in the face of political demands by extremists on either end of the spectrum.

When the economy begins to recover, that is when the FOMC should start to taper its market intervention -- not when inflation is already a problem as it is today.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.