We continue to see some pretty spectacular moves in agricultural commodities, which have been triggered by adverse weather events around the world that have caused production shortfalls. At the same time the free monies policies of the Federal Reserve are leading to increased speculation in commodity markets. This is similar to the scenario that unfolded in 2007 when the Federal Reserve began to cut rates and flood the system with liquidity in response to the subprime crisis.

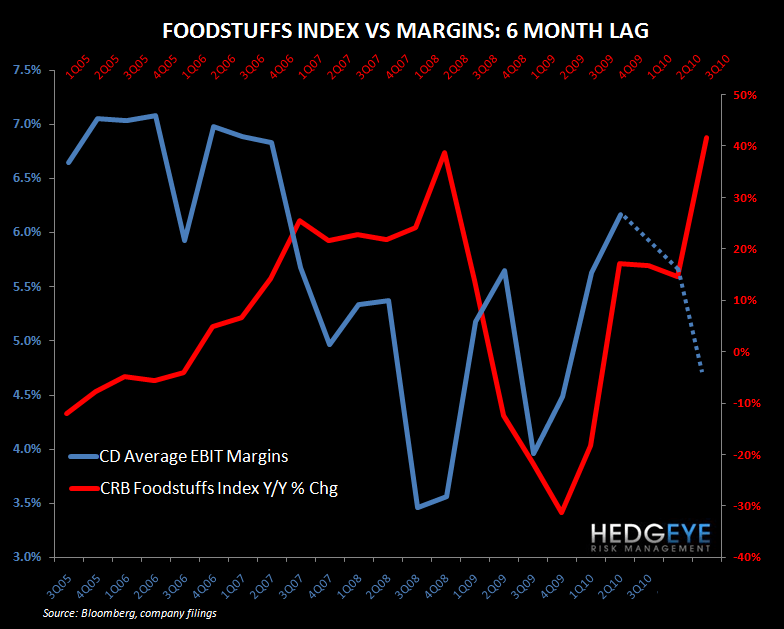

The unlimited supply of money (including derivatives) created by the Fiat Fools can dwarf the limited supply of hard commodities. We are seeing that occur right now with the price of food stuffs, as represented by the CRB Foodstuffs Index, reaching new highs in terms of year-over-year growth.

How is this consistent with the Federal Reserve dual mandate of full employment and price stability?

The unintended consequence here is that the restaurant industry is going to feel margin pressure in the not-too-distant future. The last time corn was at $6, Casual Dining margins were over 200 basis points lower than they were in 2Q10! Additionally, news that the EPA is expected to sign off on higher concentrations of ethanol in gasoline for newer vehicles, raising the maximum blend from 10% to 15%, is further supportive of corn prices.

Consumers on Main Street might get the complexities of derivative markets, but they do understand the ramifications of paying higher prices food and gas.

Howard Penney

Managing Director

(