It's been a year since we began to see toning sales ramp from its infancy and less than 1% of the US athletic footwear market to a significant category accounting for ~7% of the industry. So where does this leave the category in terms of its size and growth outlook? Additionally, share loss at the industry leader (SKX) implies the domestic category will have to grow by 50%-75% for SKX EBIT not to contract next year. Such growth is doubtful. Adi’s outlook on the other hand is positive. Let's take a walk…

Sizing up the Market:

By our estimates, toning is a $1.2Bn category accounting for ~7% of the athletic footwear market. In the process of sizing the market, we took a detailed look into NPD Group's reported sales in the toning category YTD. Then based on the recent deceleration in the category over the last few months, we are assuming that toning stabilizes at roughly 7% of the athletic footwear, or even less as new product flows through reaccelerating the overall industry.

While NPD captures a broad sample of retailers throughout department store and national chains, shoe chains and athletic specialty/sporting goods channels, this sample captures most, but not all sales. As such, we estimate is captures roughly 70% of toning sales. Therefore, assuming ~$695mm in estimated sales in 2010 accounts for only ~70% of sales through those channels, we get to $1Bn on the year. In addition, NPD's sample does not account for owned retail such as Skechers, Payless, or New Balance stores for which we've added another $160mm to arrive at our ~$1.2Bn sales estimate for 2010 – on the low end of the $1.2-$1.5bn range commonly referenced in the trade.

To get to $1.5bn, we’d need to assume a straight-line approach to the category’s trajectory through the summer months towards a 10% share of the industry assuming 5%+ growth through year-end. At this point, the ramp needed to achieve the incremental sales are clearly unlikely.

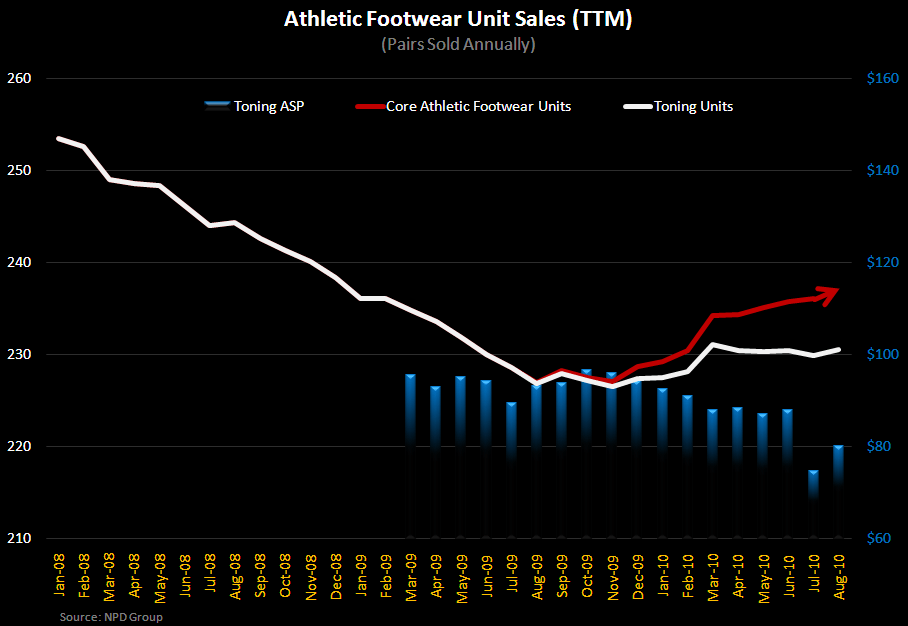

Notice the stability in sales of core athletic footwear both before and after the introduction of the toning. This suggests the category is indeed incremental and not cannibalizing other categories. This is true with the exception of the broad and generalized athletic casualty category, which has lost some of its share.

Share within Athletic Footwear:

The deceleration in toning sales relative to the industry in August has been cause for concern as the category is just now facing tough comps. We suspect this is primarily due to the timing of BTS shopping when parents (i.e. Mom's) are more focused on outfitting their kids than themselves.

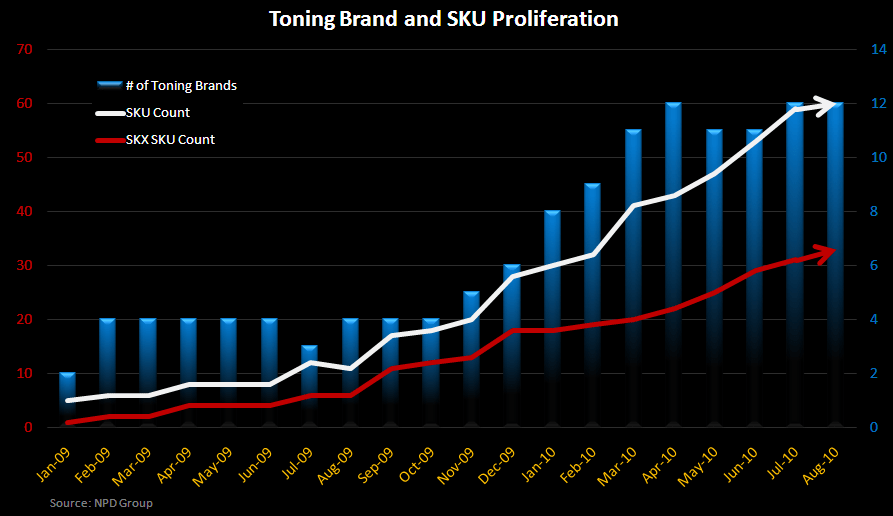

Brand Proliferation (2009 - Present - Future):

This chart says it all. After highly successful pilot tests by Skechers and Reebok early in 2009, several companies noting the trend began the 9-month process to engineer, design, produce, and then ultimately ship goods to the U.S. for sale in the late fall/spring of 2009/2010. While others were ramping up their supply chains, Skechers enjoyed a decided first mover advantage for the majority of 2009.

Clearly, the competitive landscape has ramped substantially over the last 12-months – see the chart below. In addition to the newest entrant – Fila, both Puma and Crocs have also recently announced plans to enter the category.

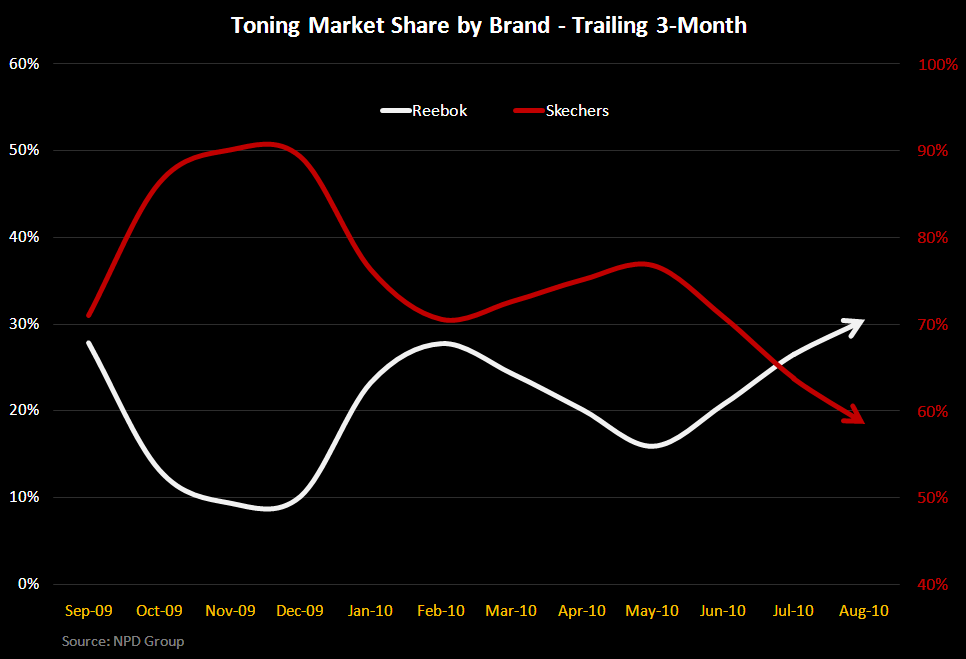

Market Share within Toning:

While Skechers dominated toning for much of 2009 with 90%+ share of the category, Reebok hit the ground running in the fall quickly capturing a sizeable share of the market. Ever since, the two have been trading share with significant variability; however the trends reflect lower highs and lower lows for Skechers while Reebok is the exact opposite. Additionally, several smaller brands are on their way to establishing 5%+ share. We’d also note that Skechers’ share is likely overstated while Reebok is probably understated by +/- 5%. As competition heightens, we expect Skechers to account for roughly 45% of the category in 2011 relative to ~60% in 2010. Based on Reebok’s upward trajectory, category extensions, and its increased commitment to spending more on the brand through the 2H than it did in the 1H, we expect the brand to account for more than 30% of the market in 2011 compared to 28% in 2010.

Skecher's and Reebok's sales as a percent of total brand sales in these channels now represent 43% and 37% for each brand respectively. It's important to note that this category accounts for less than 5% of total sales at companies like Adidas (Reebok), PSS (Champion) and New Balance though at Skechers it’s closer to 25% making it far more susceptible to potential trend deterioration. We’d also note that even the brands where it’s seemingly less relevant, this has been a hot category with A) little advertising requirements relative to sales, and B) hungry retailers looking to diversify away from Skechers.

Sales by Channel:

Distribution has evolved in the category as the brands have. While the percent of sales sold through athletic specialty channel is largely unchanged, considerably more product has been sold through department and national chain stores with increasingly more value priced product now in the market – a trend we expect to continue, and most notably…a trend consistent with a new product/technology moving towards a much more competitive part of the maturation curve.

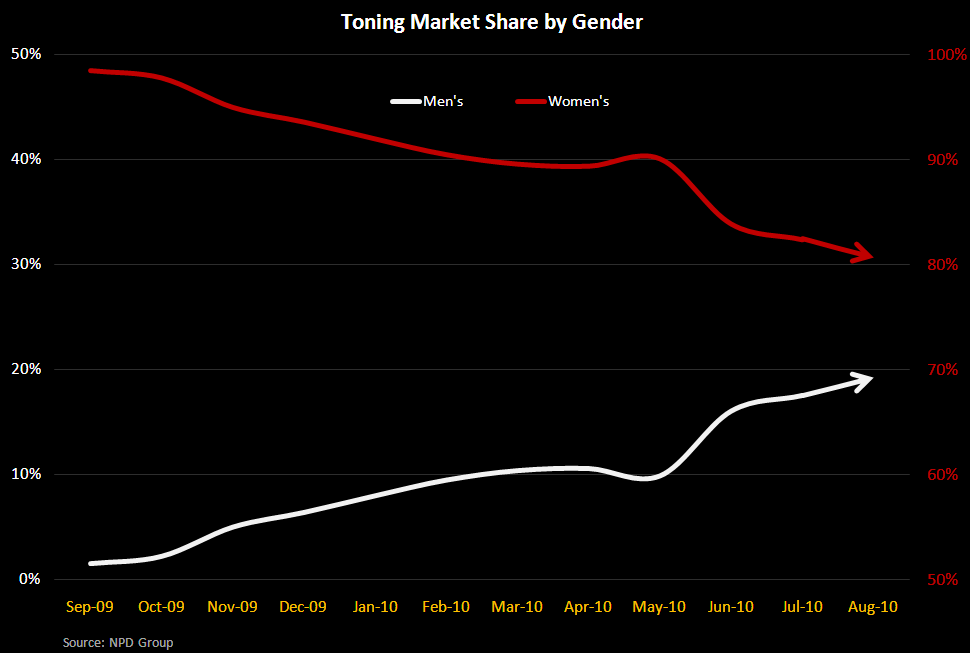

Enter the Ladies:

Arguably the most significant impact of the toning craze has been its impact on the female consumer giving women a reason to shop in the athletic channel and providing retailers with an invaluable opportunity to gain share of wallet. With a 2%+ share gain over the past year in the female demographic, spend on toning product has been almost entirely incremental to the industry. This bodes well for future demand as lower price points continue to draw more and more women into the channel.

What’s in Store for 2011?

For starters, this category has achieved a 7%+ share of the industry, but not until this past summer. With additional SKUs and extensions still coming out, we expect toning to hold at least a 6.5% share of the industry through 2011, which equates to 15% growth in category alone. Additionally, Skechers' success with the introduction of its new Resistance Runner in May has doubled its men's business – a demographic that has been slow to develop. Assuming men's continues to account for ~20% of sales next year, that would add another 5% to category sales next year. While this may sound bullish for Skechers, the math requires 50%-75% growth in year 2 for Skechers just to maintain EBIT dollars associated with the toning category. Take a look at the table below.

In looking at Skechers’ share of the industry in 2010 and gradual deterioration thereof, we assume the brand will account for ~45% of the domestic market in 2011 compared to ~60% in 2010. With price deterioration, cost inflation, and margin degradation, we estimate that incremental Shape-up margins will come in closer to 20% in 2011 from 25%-30% EBIT in 2010. The combination of share loss and compressed incremental margin is likely to reduce 2011 EBIT dollars by $40-$75mm. That’s on an base of what we estimate to be ~$170-$200mm of Shape-Ups related EBIT in 2010. In order to simply keep EBIT dollars flat, we’d have to assume that either: 1) Skechers maintains 60% share of the category, or 2) the domestic toning industry would have to grow 50%-75% in 2011 to $1.7-$2.0Bn. For many reasons, this simply will not happen. This has yet to be reflected in consensus estimates assuming mid-to-high single digit EBIT and earning declines in 2011 – we’re shaking out down 30%.

Reebok’s outlook is more positive with share gains likely to offset declines from margin degradation. Assuming a similar margin impact, revenue growth of 25%-to-30% in 2011 could net out a few cents to the positive. The bigger opportunity for the brand exists internationally where we believe it has dominant competitive position. To the extent the brand can maintain its profitability level, Reebok’s Easy Tone’s could drive $0.10-$0.15 of incremental EPS in 2011. Not exactly earth shattering, but in light of the industry bellwether’s prospect considerably more positive.

Lastly, another important observation is that unit sales in the industry have been substantially higher over the last few years suggesting the capacity for additional unit demand even in the face of retracted consumer spending is possible and would still be below recent peak levels. This is not in our estimate for category growth next year. All in we're expecting the category to grow ~25% next year domestically to $1.4Bn.

Casey Flavin

Director