R3: REQUIRED RETAIL READING

October 12, 2010

M&A still the topic of the day with news of Nike capturing the NFL apparel license from Reebok a close second.

RESEARCH ANECDOTES

- Score one for the “fans.” After receiving a week’s worth of backlash regarding Gap’s reinvented logo on Facebook and other blogs, the company has reverted back to its old branding. Interestingly, Gap’s president, Marka Hansen, admits that the company made a big mistake by not engaging their passionate customers BEFORE making the branding change. This will go down as a case study for other brands looking to test the waters on change. Clearly a case of Facebook viewed as a liability and not an asset.

- Rumor has it that fashion designer Alexander Wang may be working on a collaboration project with Nike. Recall that other athletic brands have historically forged relationships with high-end designer. Adidas and Stella McCartney and Puma and Hussein Chalayan are just a couple examples.

- In just 10 years, a 20 point gap in the percentage of 25-34 year olds getting married vs. staying single has reversed. As it stands now, 46% of those aged 25-34 are single vs. 45% which are married. Marketers have taken particular note of this demographic trend, which suggests teens and college students are not the only target groups which are being focused on with a “single” approach.

OUR TAKE ON OVERNIGHT NEWS

Retail M&A Activity Heats Up With GYMB, DLTR, and JCP Activism - The markets were left to digest news that The Gymboree Corp. had agreed to be taken over by Bain Capital Partners LLC, fulfilling expectations of a private equity takeover of the specialty chain geared to children and their parents, as well as Dollar Tree Inc.’s acquisition of the 85-unit Dollar Giant stores chain in Canada. And Bill Ackman's Pershing Square fund's 16.5% stake in JCP. Gymboree agreed to be acquired and taken private by Bain for $65.40 a share, or $1.8 bn. Dollar Tree’s acquisition of Dollar Giant, for $51 million, is the company’s first expansion outside the U.S. The deal is expected to close by mid-November. Dollar Giant stores average 9,000 gross square feet and operate in British Columbia, Ontario, Alberta and Saskatchewan. The retailer prices its goods and consumables at $1 or less. <wwd.com/business-news>

Hedgeye Retail’s Take: While we expected M&A would be a big story this year, we’re surprised to see deals being struck at peak margins and peak stock prices. 2007 anyone?

Wal-Mart to Benefit From Budget-Conscious Shoppers - Wal-Mart Stores Inc., the world’s largest retailer, will attract a bigger share of holiday shoppers this year as budget-conscious consumers seek discounts, according to a survey released today. The amount of consumers who said they plan to do more holiday shopping at Wal-Mart exceeded the share of those who expected to do less by 22%, according to the survey by Consumer Edge Research. The study canvassed about 2,500 people in the U.S. Consumers are curbing spending as the unemployment rate hovers near a 26-year high, prompting stores to boost promotions to draw shoppers. Other retailers that may profit from shoppers’ caution include Amazon.com Inc., EBay Inc., and Target Corp. More shoppers plan to avoid stores owned by Costco Wholesale Corp., Toys ’R’ Us Inc., and department stores like Macy’s Inc. <bloomberg.com>

Hedgeye Retail’s Take: Hard to believe that the holiday alone would drive incremental traffic to WMT given their merchandising challenges. If anything, consumers may be disappointed that prices are no longer being aggressively rolled back.

UK Based Chain Accessorize Arrives in the US - Accessorize, the U.K.-based chain, is dipping a big toe in U.S. waters with the openings in New York of a 400-square-foot store at 329 Bleecker Street on Oct. 28 and a 500-square-foot unit at 1 Union Square West on Nov. 18. With an ambitious plan, the company will take the plunge and aims to open 100 units in the U.S. by 2015. In addition to the store openings, the retailer, which is a division of the multimillion-dollar Monsoon retail group, is working to launch a U.S. transactional Web site. The UK company has existed for 27 years and has over 750 stores. The product range includes statement jewelry, bridal jewelry, watches, handbags, purses, wallets, shoes, hats, gloves, lingerie and more. Accessorize introduces 1,500 new products each season; they are well-priced and globally sourced. Stores do an average of $1,500 a square foot. <wwd.com/retail-news>

Hedgeye Retail’s Take: The UK invasion continues and it’s not just a handful of stores. With 100 Accessorize units slated to open over the next 5 years, this is definitely a trend to watch.

Ralph Lauren To Open Its First UK Rugby Store - The luxury lifestyle brand will open a 5,703 sq ft Rugby store at 43 King Street in autumn next year, on a 15-year lease. The signing follows a new letting to Burberry, which will open a store on King Street in 2011. Developer of the area Capco has been striving transform the area into a more upmarket shopping destination. <retail-week.com>

Hedgeye Retail’s Take: Although its only 1 store, this is a sign of growth for RL's youthful, preppy brand which currently only has 11 stores all based in the US. Look to see RL put more support behind this brand as it looks to grow in alternative channels like the recent success of Club Monaco.

Other Countries Benefit From China's Rising Labor Costs - As the world’s manufacturing powerhouse sees the demand for higher wages and the cost of operations increase, apparel companies are starting to turn to places such as Vietnam, India and Bangladesh, as well as Central America and Mexico for production. Many already have experience in these regions even while they kept the bulk of their sourcing in China, as political and practical decisions forced their hand during the last decade. <wwd.com/business-news>

Hedgeye Retail’s Take: Not new news here, but sizing up the chart below is noteworthy. Two of the greatest beneficiaries - Bangladesh and Vietnam have considerably different wage rates reflecting the ‘premium’ retailers are willing to pay for a more developed economy and with inherently lower risks.

World Apparel Convention Discuss Cotton, Consumers, Labor Costs, and the End of Fast Fashion - Panelists at the two-day World Apparel Convention held here last week by the International Apparel Federation said higher production costs from raw materials and labor would be passed on to consumers. The rising retail prices could potentially mean the end of cheap and fast fashion, they said. Robin Anson, managing director for Textiles Intelligence claimed, "I don’t see the price [of cotton] coming down at least for the next crop year.” The increasing cost of labor is a more worrying trend that is likely to continue, not just in China but also in Vietnam and Bangladesh. Chinese workers are no longer willing to work miles away from home to only see their family once a year. Minimum wage has already increased twice in the last two years. China’s apparel industry could, over time, become more like that of Italy’s small manufacturing districts. <wwd.com/business-news>

Hedgeye Retail’s Take: If Anson’s view becomes a reality with persistently high cotton costs through next year, not only will apparel get more expensive for the consumer, but more importantly retailer margins will be compressed substantially more than what the Street is expecting in next year’s estimates.

Manufacturers and Designers Cope With Impact of Higher Costs - Designers focused on trying to limit the impact of higher costs as they sought textured goods or soft, draping fabrics for next fall’s collections at textile shows here. With mills raising prices in response to the increased costs of cotton, minerals, labor and energy, designers said they had little choice but to absorb the higher costs and shrink their profit margins. “You can’t [raise the prices of the clothing] because [there’s] too much competition from other manufacturers and stuff coming in from China is so cheap,” said Miriam Schwartz, designer for junior dress line CW Designs in Tarzana, Calif. <wwd.com/markets-news>

Hedgeye Retail’s Take: Expect to see more of these public admissions from designers and retailers alike – particularly in light of our Consumer Cannonball theme, which we’ll be hitting on in our Friday call, suggesting that consumers will not be the ones eating higher costs across retail.

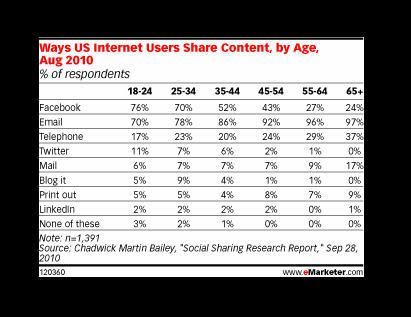

Email Still Tops Facebook for Keeping in Touch - Facebook may have more than 500 million users around the world, but in the US most people online still rely more on email to share content with friends and family. <emarketer.com>

Hedgeye Retail’s Take: With the 18-24 age group the only demographic that uses Facebook more widely than email it’s going to be years until that mix shifts up through adjoining brackets. However, given the novelty of the site, we question the sustainability of these 70% rates. That said, the fact that the site has achieved that sort of penetration over alternative legacy mediums is impressive to say the least.