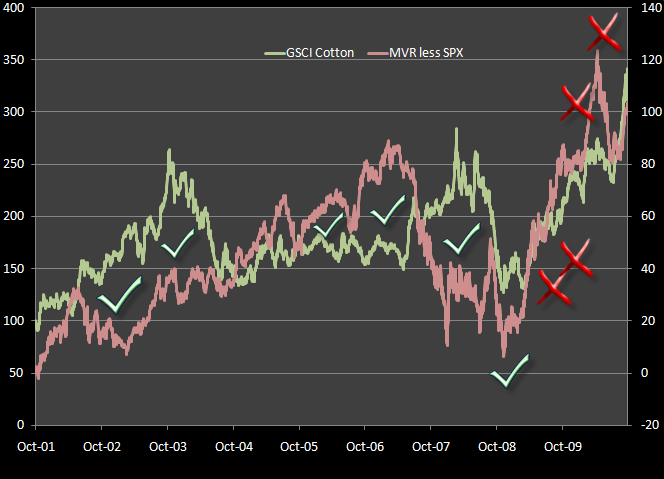

The fact that cotton prices are at record highs is not new, but then why is the market looking right through it as it relates to retail? The chart below shows the spread between the MVR (Morgan Stanley Retail Index) and the S&P500 matched against a cotton price index. Without fail, over the six notable periods from 2000-2008, retail zigged when connot prices zagged. But since early 2009, there was only zigging to be found across the board. That was easily explainable by post-recession earnings revisions that took retail up through 1Q10. But that is O-V-E-R.

We'll dive into this, as well as other salient issues on Friday at 10am est when we release our next Retail Blackbook called Consumption Cannonball: The Retail Aftermath. Please contact for details.