The guest commentary below was written by Jeff Snider of Alhambra Investments. This piece does not necessarily reflect the opinions of Hedgeye.

For a short while, with reflation being traded in almost every corner of the global bond market, the Bank of Japan started to get “those” questions again. Almost of the humble brag variety.

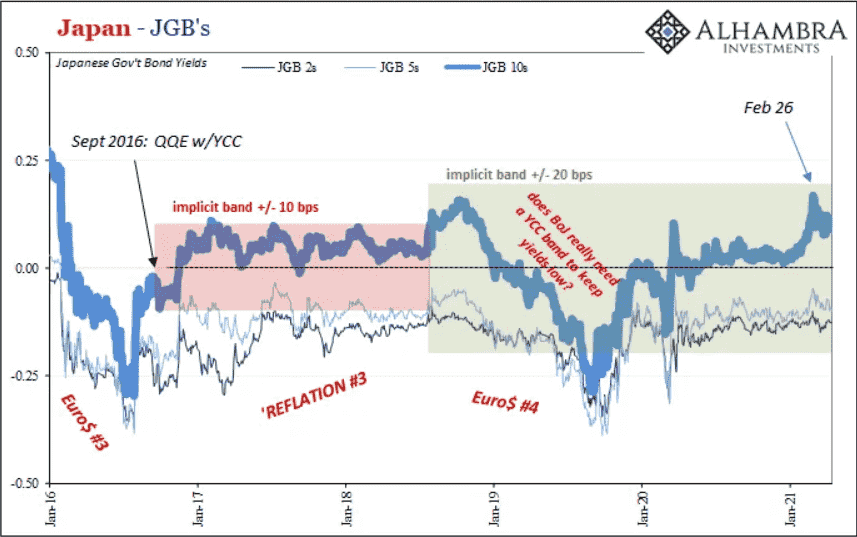

A few years ago, Japan’s central bank had widened what it considered to be an acceptable trading range for its 2016 QQE addendum of Yield Curve Control (YCC). In 2018, Haruhiko Kuroda’s regime stated that it would “allow” 10-year JGB yields anywhere between -20 bps and +20 bps.

By late February 2021, optimism worldwide became such that the JGB 10s took off (sold off) in a trajectory that made it appear likely to test Kuroda’s power and commitment to YCC in its current iteration. Making it to 17 bps, yields then fell backward down toward 10 bps or so all over again.

To the media, and to Kuroda, this was a(nother) sign as to just how effective YCC must be in the hands of skilled monetary pioneers like those at BoJ; after all, they came up with QE twenty years ago and inaugurated this version of yield caps.

Hail to the experiment!

|

MISSION ALREADY ACCOMPLISHED? |

Already, you can spot their problem; if it had been a “global bond rout” which was responsible for pushing up Japan’s government interest rates, could it have really been YCC that then kept them under “control?” Perhaps, but only if Japan’s experience turned out to be unique.

Of course it wasn’t. As has been the case time and again, the market – not the central bank, any central bank – determines what and where bond yields trade. QE’s, QQE’s, and YCC’s are all just characters in an increasingly stale, uninteresting puppet show only the mainstream media (and the “analysts” it quotes) finds useful.

To begin with, notice what sticks out on the JGB chart: February 26.

While pundits had latched onto YCC for the JGB market’s sudden reversal anyone actually paying attention to that “global bond rout” has known perfectly well just how often February 24-25-26 has come up in almost every one of these markets including Japan’s.

Japanese YCC would have had absolutely nothing to do with, say, German bunds or UST TIPS real yields.

Instead, it’s another pertinent example from another key market which blatantly switched out of reflation and into some weird sort of pause in it. Maybe it progresses and eventually forms a more complete inflection, maybe reflation restarts at some point. For now, it is a globally synchronized short run problem.

Why a problem?

Because during this same almost two months, that has been when everything has been supposedly going right; not just right, darn near perfect. You don’t need me to recite the list yet again, vaccines et al.

Even more than that, though, why Feb 24-25-26? On the 25th, ugly, violent selloff in the US Treasury portion of the marketplace which spilled over into other segments – including, as you can see above, JGB’s whose 10s added nearly 5 bps in two trading days (25th and 26th) which is an eye-catching short-term move in that place.

Here’s the thing; if that UST selloff was simply the market eyeing some seriously increasing probability of inflation, a deepening and rising sense of the reflationary trading already underway, why did it suddenly stop in all these other markets immediately after that violent selloff happened?

You’d think that Treasury yields shooting upward because of growing confidence in the inflation story (therefore negative for safe, liquid instruments) would only confirm the idea for all the markets closely related to it.

Instead, just the one. There really should not have been such a key global divergence.

And it wasn’t the entire Treasury market, either. As noted before, the TIPS chorus with its fundamental “real” yields went with Germany and Japan post-Feb 25 rather than sticking with the direction of UST nominals. In other words, that Treasury event really could not have been a reflation-related selloff otherwise this would have been reflected by continuing higher yields all around its backyard as well as the rest of the world.

Even if rates haven’t fallen that much since, they very clearly stopped rising right at that point with UST TIPS fingering the likely suspect.

What that leaves for us considering the possible nature of and root underlying concern for this reflation pause is a very thin list. There’s really only the one candidate – Fedwire Feb 24.

One key component of the Treasury rout on the 25th was a “poorly” visited auction of 7-year notes. Dealers who had dependably bid up and for whatever Yellen was selling previously suddenly seem to have abandoned the poor Treasury Secretary:

|

A big move came in the early afternoon when an auction for $62 billion of 7-year notes by the U.S. Treasury showed poor demand, with a bid-to-cover ratio of 2.04, the lowest on record according to a note from DRW Trading market strategist Lou Brien who called the result “terrible.” |

Again, if lack of dealer (and foreign) bidding was, as was claimed, due to inflation fears or even supply angst, then it just can’t explain the global bond market’s contrary trading from that point forward; especially TIPS real yields.

Fedwire, however, could – starting with the absence of dealers on this particular day in question.

The interbank payment disruption itself wasn’t really that big of a deal. But, just like September 2019 repo, it exposed serious, unresolved cracks in the façade, reminding the global system that it is held together still today by a very fragile framework where, again like 2019, when something unanticipated happens the dealers ungracefully exit and leave liquidity to its own spotty devices.

Backed up by the previous day’s unsettled Fedwire transactions, dealers (somewhat) sat out the 7s and the rest is (short run) history.

Nominal UST’s, even the hitherto unstoppable 5-year TIPS inflation breakevens, each have now spent several weeks joined with the rest of the bond market’s reflation “pause.”

Fragile means anti-reflation because it has the potential to, yet again, interrupt and eventually fully corrupt even the most virulent and otherwise apparently robust reflationary trends if left unchecked (which, due to exclusive dependence on puppet shows, is always the base case).

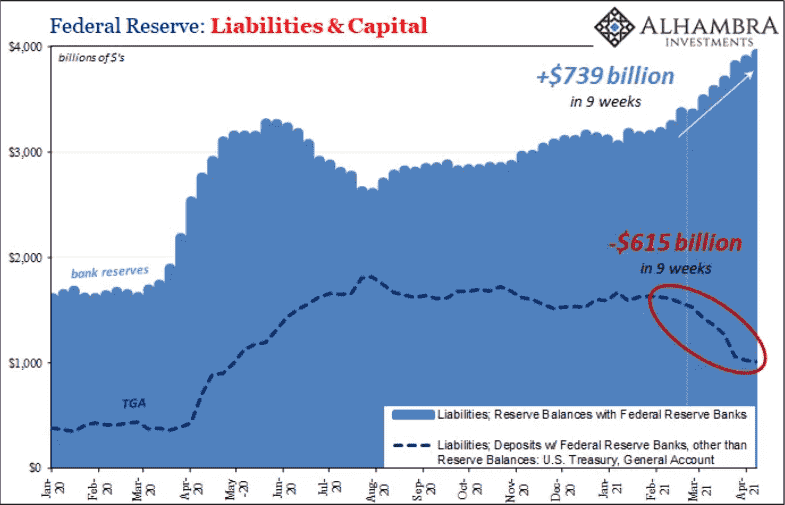

Money and dollars trump everything; if you haven’t figured it out over the last fourteen years, liquidity risk continues to be paramount no matter how many trillions of inert, mostly useless bank reserves.

Stretching all the way toward mid-April, closing in on 2 months, it remains the most dominant aspect of every important chart (obviously disqualifying those pertaining to the stock market). While everyone is talking about inflation and “stimulus”, the roaring economy right around the corner, the one thing across the entire global bond market has been and continues to be Feb 24-25-26.

It sure wasn’t YCC (LOL).

That UST selloff wasn’t reflation – it was illiquidity at perhaps the worst possible moment. And, I think, it shows just how fragile the underlying situation really is: everything going right except this one seemingly teeny, tiny thing.

But that’s the point; appearing to be nothing, like Mandelbrot warned, how quickly it spiraled into “something.” A globe-trotting something.

That is fragility. Say it in English. Say it in German. Say it in Japanese. They’re all spelled in (euro)dollar.

EDITOR'S NOTE

Jeff Snider is Head of Global Investment Research for Alhambra Investments. Jeff spearheads the investment research efforts while providing close contact to Alhambra’s client base. This piece does not necessarily reflect the opinions of Hedgeye.