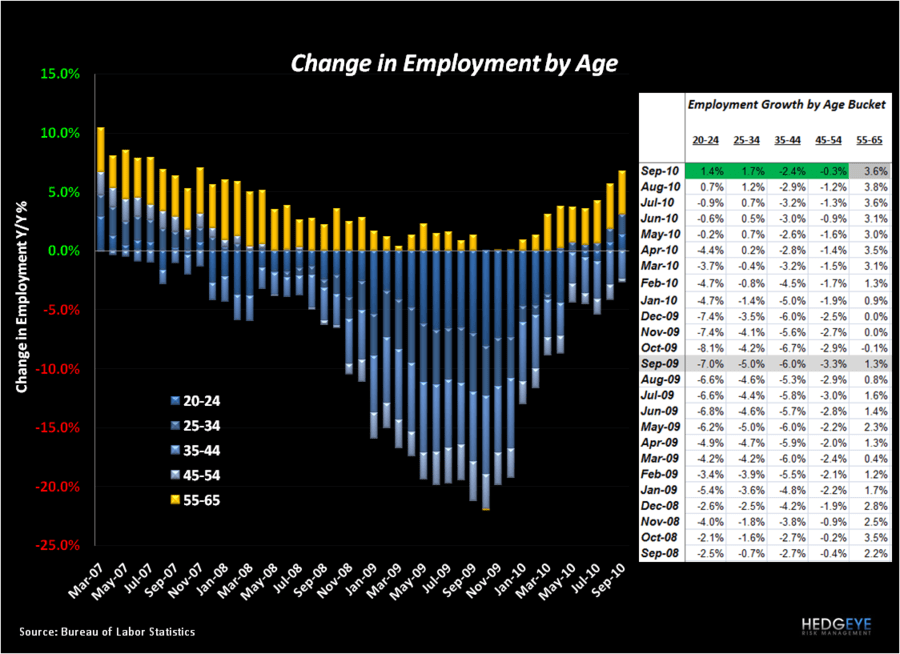

Unemployment data released this morning by the Bureau of Labor Statistics were positive for Quick Service restaurant stocks. While joblessness has been dragging consumer spending for some time now, and management teams in quick service and casual dining cite it regularly as an issue, quick service restaurants have been the most susceptible to deteriorations in the employment outlook. As I wrote on September 7th in a post entitled, “QSR: EMPLOYMENT DATA POSITIVE ON THE MARGIN”, MCD, SONC, JACK, BJC, YUM, and WEN have mentioned unemployment (particularly among younger age cohorts) as being a primary impediment to same-store sales growth.

The most recent data from the BLS, for September, reveals that 20-24 year olds saw a year-over-year uptick in employment levels for the second consecutive month. August’s improvement was the first since September 2007. It is important to keep in mind the significant headwinds facing the industry, such as increasing price competition and increasing commodity costs, but this morning’s news is positive nonetheless.

Howard Penney

Managing Director