YoY change will certainly look better in the coming months. We prefer to look at seasonally adjusted absolute volumes to monitor sequential performance.

There is no evidence that underlying business levels in the Las Vegas locals market have improved sequentially (or year over year for that matter). In fact, with the exception of April, actual monthly volumes have underperformed sequentially every month since October 2009 per our analysis. August revenues have not yet been released by the State of Nevada, but anything less than a 4.5% YoY volume drop in August should be seen as another disappointing month.

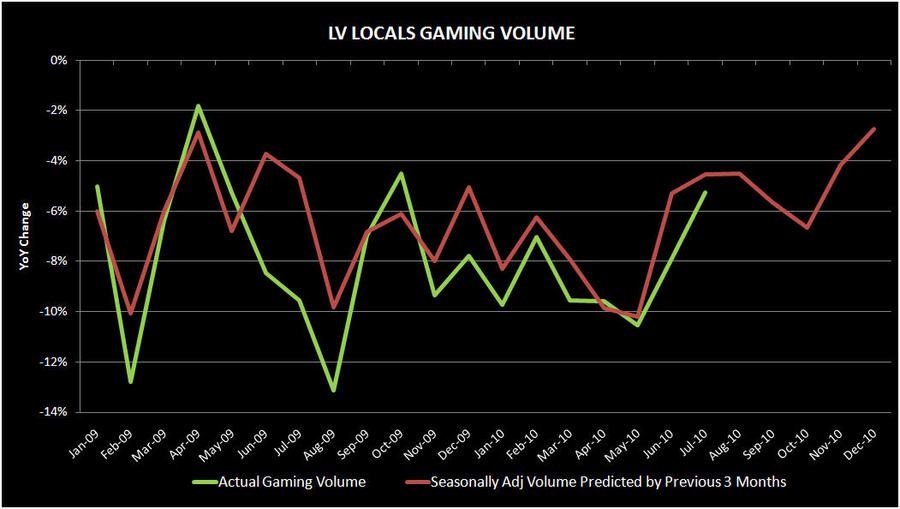

The extreme volatility since 2007 in the monthly numbers coming out of the Las Vegas market render YoY comparison analysis fairly irrelevant. As we’ve done for the regional markets and hotels, we prefer to look at seasonally adjusted sequential metrics to try and ascertain whether business fundamentals are improving. For the Locals, we focus on volumes since hold percentages can be volatile and Nevada is not consistent in its revenue counts when months end on weekends.

The chart below shows monthly YoY gaming volume changes for the LV locals market as well as a seasonally adjusted projection of where volume should have been based on the average of the previous three months. Since actual volume trailed predicted volume in most of the recent months, this is indicative of sequential slowing in seasonally adjusted volumes and is not a positive sign for the market.

The problems with Las Vegas are well known. Housing, which we’ve determined has been the number #1 driver of gaming revenues in the market historically, remains under pressure. The Las Vegas metro area suffers from one of the worst unemployment rates in the country, another statistically significant variable in determining gaming revenues. Even population growth has gone negative. Our analysis here supports the sad state of the economic environment there.

We don’t mean to pile on BYD since the stock is not expensive, short interest is high, and investor sentiment is awful. We would love to be contrarian on the name. Possible catalysts include refinancing its credit facility – we actually think they are making progress – and buying the other half of Borgata on the cheap – should happen. The real catalyst of course will be improvement in the LV locals market which, unfortunately, hasn't ocurred.