Conclusion: Ruby Tuesday has seen a solid start to their fiscal year; time will tell how the new business pans out.

RT’s fiscal 1Q11 top-line and bottom line results came in better than I was expecting, but relatively in line with street estimates. Same-store sales grew +1.2% during the quarter, which implies a 50 bp acceleration in two-year average trends from the prior quarter. This performance is impressive given that Knapp trends decelerated 10 bps on a two-year average basis during the same timeframe. During the quarter, RT widened its gap to Knapp to +2.5% on a two-year average basis versus -1.8% in the year ago quarter.

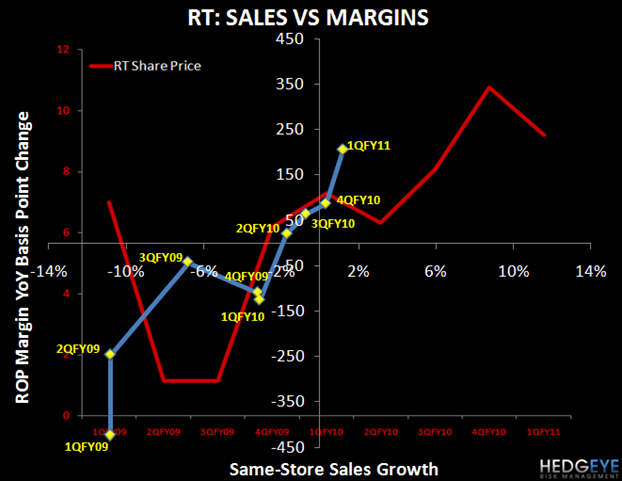

Restaurant-level margin improved 210 bps YOY to 18% (excluding the $1.7 million in accounting gains from franchise partner acquisitions). I was expecting restaurant margin to improve in 1Q11, but this growth exceeded my expectations, largely as a result of better-than-expected comp growth and “lower levels of promotional activity.”

Given this positive margin and comp growth, RT operated in the Nirvana quadrant of our restaurant sigma chart for the second consecutive quarter. Going into the quarter, I thought the company could fall out of Nirvana as early as 2Q11, but given the strong current trends, RT could potentially remain in Nirvana in the next quarter (if the company can sustain its current sales momentum). The margin comparisons, however, do get more difficult in the back half of the year. For reference, RT is now guiding to flat full-year restaurant-level margin versus its prior guidance of a slight YOY decline. This flat guidance implies that the company will have to give back some of the gains achieved in fiscal 1Q11 as it progresses through the year.

Management maintained both its full-year same-store sales growth guidance of flat to +2.0% and its EPS outlook of $0.76-$0.86 (street is at $0.85). Although RT got a head start during the first quarter in achieving this comp goal relative to my expectations, I continue to believe that this target, particularly the high end of the range (street is at +1.9%), will be difficult to accomplish as it implies a continued improvement in trends on a two-year average basis for the balance of the year. The Hedgeye view is that the consumer will face increased pressure in calendar 4Q10 and into calendar 2011. At the same time, RT will face increasingly more difficult comparisons as it progresses through the year, particularly in the back half of fiscal 2011.

RT seems to be doing all of the right things to increase its guest satisfaction scores, add sales layers and improve operations within its four walls. The company has made a lot of progress in growing same-store sales and started the year with a lot of momentum. To that end, my concern around the company’s ability to achieve the high end of its comp guidance, as expected by the street, is more a function of the economic environment and the potential for a further slowdown in top-line trends for the casual dining industry as a whole.

Howard Penney

Managing Director