Since we're always asked about the M&A market during earnings season, we've highlighted a few trends below.

MARKET TRENDS for the 3Q

- Average Key Per Price for luxury/UUP transactions in 3Q rose to $350k, which was higher than the YTD average of $300k.

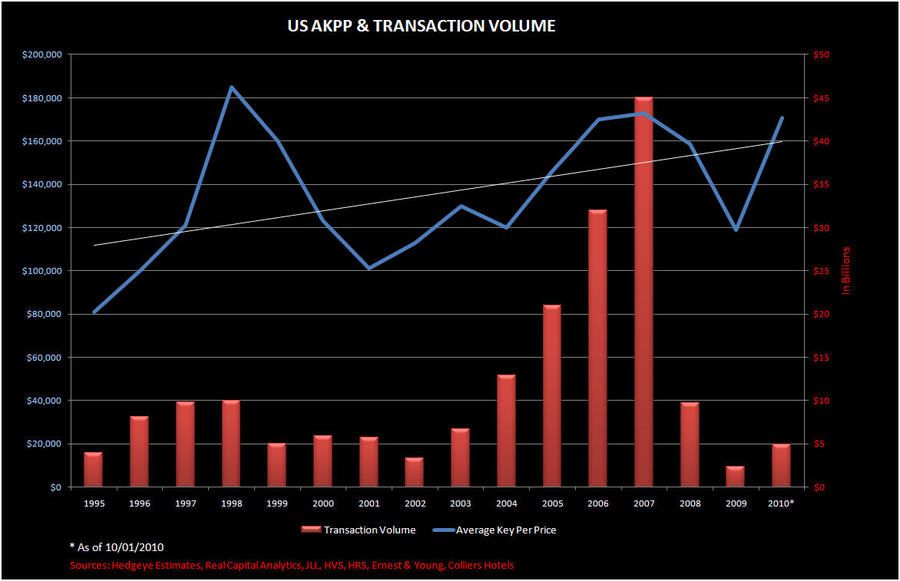

- Global transaction volume of $9.9BN topped last year’s level of $9.0BN.

- US transaction volume is closing in on $5BN, up 106% YoY. The bulk of transactions continue to be single-asset and Luxury/UUP.

- REITS (existing and newly formed) have dominated the M&A market so far.

- Access to capital continues to be limited.

- According to Fitch - CMBS hotel loans defaulted at a higher rate (20%) in August than July (18.6%)

LUXURY/UUP MARKET

- Average Key Per Price

- US $359,795 since 6/30/2010 (13 transactions)

- $301,886 YTD (33 transactions)

- International

- $279,784 since 6/30/2010 (11 transactions)

- $427,097 YTD (24 transactions)

- Cap rates/Valuation

- 5-6% range, in line with 2006 cap rates

- 9-11x EBITDA; however, two luxury hotels recently sold at 17-18x EBITDA

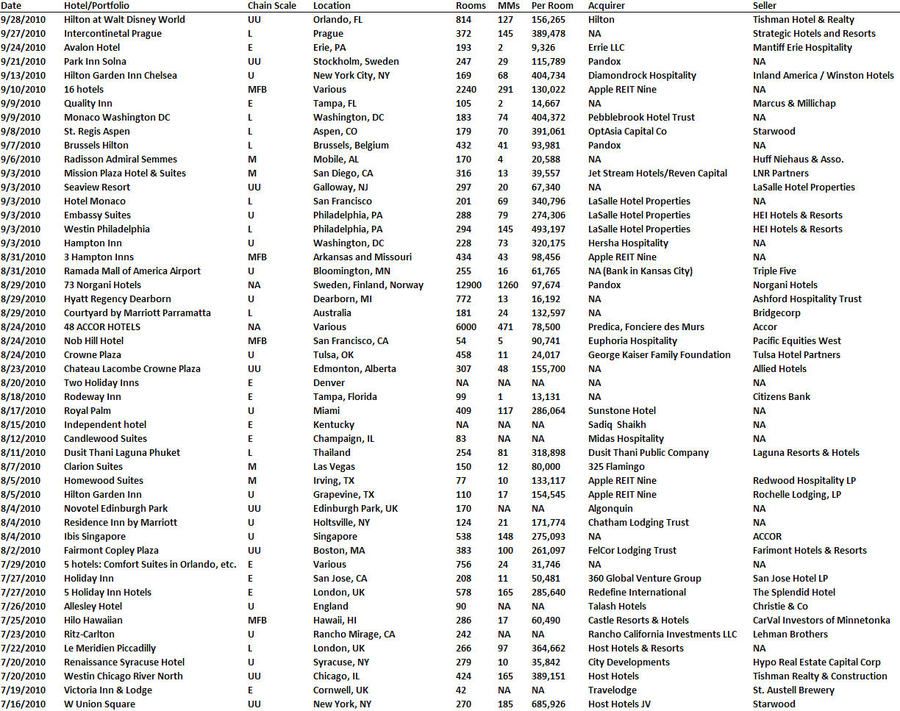

Q3 Transactions (Summary)