Portfolio: Long British Pound (FXB), bullish on EUR-USD; Short Italy (EWI)

Conclusion: citing a senior government source, Eurostat is expected to revise Greece’s budget deficit and debt in 2009 significantly upward. This announcement puts further question into the validity of Eurostat data and by extension the data from member countries. Greece’s likely upward revision ties into our forecast for continued sovereign debt risk in Europe, and underlines our call for a divergence, especially among Europe’s fiscally weaker countries. Today we sold Germany (via the etf EWG), our one bullish position in Europe. We caution on slower growth across the region into year-end.

The Eurozone’s sore thumb, Greece, could look a lot more black and blue if in fact Greece’s budget deficit and debt for 2009 are revised higher. Sources suggest the country’s deficit could be revised to 15.1% of GDP from 13.8% and the debt could be revised to 127% of GDP versus a previous calculation of 115.1%.

Clearly, a revision of this magnitude is not inconceivable given the country’s years of fiscal mismanagement, including improper book keeping. If substantiated, the revision further erodes Greek PM’s George Papandreou’s credibility and his targeted debt and deficit reduction plan over the next three years.

Our view is that Greece (and debt and deficit-laden countries like it) will remain the EU’s baby in the sense that European commissioners and heads of state will do everything in their power to prevent the immediate term failure (default) of member states for fear of the associated volatility (contagion).

Euro-crats had a good taste of contagion fears and currency destruction in the first half of the year, which led to the decision on May 9th to issue a €750 Billion package of medicine to contain it. Politics are generally local, but recently the EU’s political scene has gone global. Surely politicians in Brussels can ill afford talk of the destruction of the Eurozone!

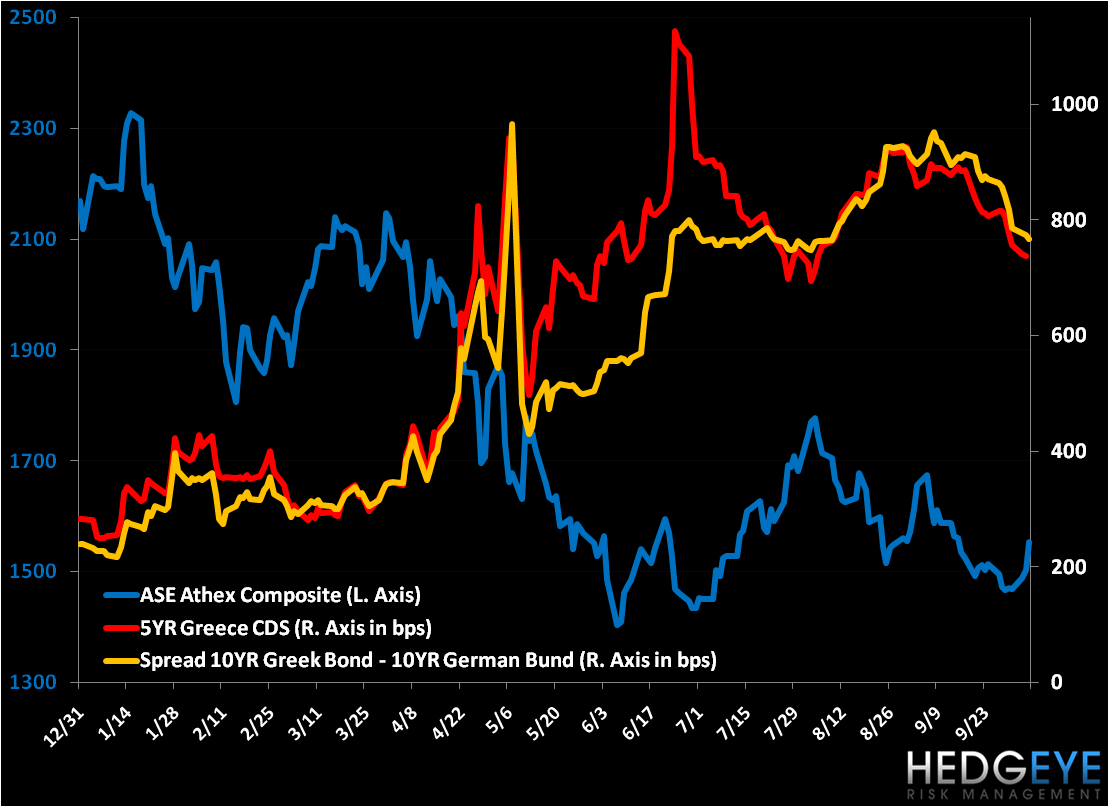

While we don’t see an outright default by member countries over the intermediate term, what is clear is that capital markets are signaling the distressed outlook for fiscally weaker nations. For instance, Greece’s Athex Composite is the worst performing equity market in the world YTD, down -29.3%. And as the charts below display, 5YR Sovereign CDS spreads have not abated significantly over recent weeks, with Portugal and Ireland holding above the 400 bps level, a critical break-out level (Shark Line) based on our analysis. Also, as the final chart shows, sovereign bond yields also remain elevated particularly for Portugal and Spain, a reflection of the risk premium investors demand to hold the country’s debt (see charts below).

Certainly there are a number of headwinds for investors to be aware of in Europe. We’re currently short Italy in the Hedgeye Portfolio and very cautious on the region as a whole. Please see our post on 9/28 titled “Why We’re Short Italy” for our fundamental view on Italy.

Matthew Hedrick

Analyst