This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst on March 29th, 2021. This piece does not necessarily reflect the opinion of Hedgeye.

What a difference a year makes.

Twelve months ago, some of the industry’s largest independent mortgage banks (IMBs) were in danger of tipping over due to the liquidity wave unleashed by the Federal Open Market Committee in response to COVID.

We hear that a federal rescue nearly occurred for several IMBs a year ago. These same firms are flush after a year of feasting on record lending volumes, but today face a labyrinth of risk in resolving delinquent loans now under the protection of the CARES Act and state lending moratoria.

While the number of loans in forbearance is dropping fast, by the summer there will still be many hundreds of thousands of loans that have not exited successfully and will likely go to modification or foreclosure. How these loans are resolved is crucially important to both consumers and the investors that hold the paper on these mortgages.

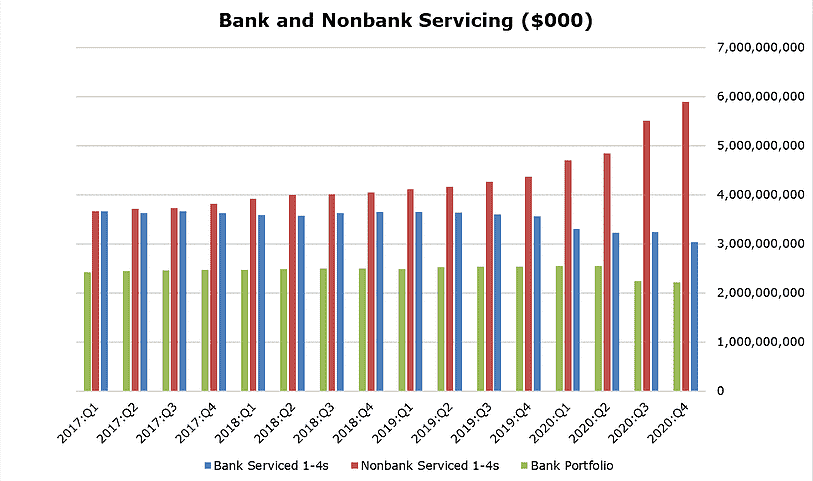

Given that IMBs now service two-thirds of all 1-4 family residential mortgage loans, the risk to the nonbanks from COVID is significant and growing.

Note in the chart below that the flight of commercial banks from owning and servicing 1-4 family loans continues unabated, a trend due entirely to Dodd Frank, Basle III and regulation of mortgage lending.

Note particularly the huge decline in servicing assets under management (AUM) for banks in Q3 2020 due to loan prepayments. The IMBs captured these loan refinance events.

Source: MBA/FFIEC

Few policymakers in Washington understand that the mortgage servicer acts on behalf of the note holder and is legally bound by the investor’s rules and contractual provisions.

The CARES Act represents an illegal intrusion into that private contractual relationship, part of a larger attack on private contracts and business that is a core strategy of the progressive political agenda.

The losses incurred by bank and nonbank servicers as a result of the CARES Act and state forbearance laws arguably represent an unconstitutional taking from these private companies and their owners.

Members of Congress and state officials need to appreciate that without investors and the loan servicers who represent their interests, there is no housing finance market. The cavalier imposition of loan forbearance laws via the CARES Act, no matter how well justified in terms of compassion and immediate human need, has an enormous cost that has largely been ignored by elected officials.

Last year the Federal Housing Finance Agency under Director Mark Calabria decided to subsidize part of this cost of dealing with COVID for the GSEs by imposing an “adverse market” fee on new mortgage refinance loans.

This policy implemented by FHFA is an overt and decidedly progressive transfer of value from stronger borrowers to the weak. As refinance volumes fall, however, this relatively painless fix is disappearing along with the revenue and liquidity float that enabled the industry to deal with COVID in 2020.

Source: MBA

Private mortgage servicers, however, have been left hanging by consumer-fixated progressive politicians in Washington and around the nation.

Progressives effectively expect IMBs and banks to spend part or all of their income from record lending volumes in 2020 to help consumers. Politicians are largely oblivious to the longer-term consequences to the markets and the US economy of their false generosity.

In legal terms, bank and nonbank mortgage servicers must follow the credit waterfall defined by the investor in the Fannie Mae, Freddie Mac or Ginnie Mae security. In finance, under a waterfall payment scheme in a typical private mortgage security, senior lenders receive principal and interest payments from a borrower first, and subordinate lenders receive principal and interest payments after the seniors are paid in full.

In agency and government mortgage-backed securities (MBS), all of the investors are treated equally in terms of allocations of principal, interest and, most important, expenses.

In representing the investor in MBS, mortgage servicers face a conflicting maze of private contractual requirements, agency rules and CARES Act and state laws. For example, even if a delinquent borrower qualifies for a program higher up on the credit waterfall in terms of losses to investors, servicers often do not have an option to offer a program – even if it may be in the consumer’s best interest long term (i.e, a partial claim vs loan modification).

Servicers are required to review a borrower’s eligibility for programs set forth by the investor and insurer of the loan (Fannie Mae, Freddie Mac or the FHA). In instances where the borrower does not qualify for federally mandated investor/insurer programs, servicers may still be required to offer them a permanent solution required under state law. Every servicer must prepare their servicing executives and systems for all of these potential scenarios.

Many states have enacted legislation that requires a mortgage servicer to offer a forbearance program to the delinquent borrower if they do not otherwise qualify for relief.

Servicers are forced to comply with state law and offer the program, even if the program conflicts with the contractual duty to the note holder and/or the rules set forth by the federal agency that insures the loan.

States such as Massachusetts, for example, have created a template that now competes with the FHA, the GSEs, VA and USDA. All have different programs and normative templates for offering relief. The timing of the end of forbearance and foreclosure relief is crucial for servicers, both in terms of helping consumers and protecting themselves from a myriad of risks. By no coincidence, many lenders now refuse to do business in states such as Massachusetts and New York.

For example, what is the current timeline (under existing relief measures and agency guidance) for borrowers to begin rolling off of CARES Act forbearance and/or foreclosure moratoria? Do servicers have obligations to the borrower, for example, ahead of the expiration of forbearance relief in terms of notices or communication?

Questions: If the servicer gets these steps for dealing with COVID forbearance loans wrong, could they face loan repurchase demands from the GSEs or a refusal to honor insurance claims from the FHA? A: Yes.

If the servicer gets these steps wrong, will they face state sanctions? A: Yes.

The GSEs specifically require servicers to contact a borrower in forbearance 30 days before the program ends, but the loan insurers require such a contact “prior to the end of forbearance or at the end of forbearance.”

Which timeline should the servicer follow? All of the above.

As the largest cohort of delinquent customers begin rolling off forbearance in Q2 2021, twelve months after the majority of the customer base of banks and IMBs requested debt relief, servicers will face the challenge of managing multiple channels for dealing with distressed consumers.

Extensions will help spread the timing of the of end of consumer forbearance, but this also means that an even larger portion of the population will now exit between Q2 and Q3 of 2021.

Indeed, the many possible borrower scenarios must be scripted by the servicer, which in turn must roll out training, compliance and IT support for all of these permutations of borrower distress. Keep in mind that servicers are debt collectors working for the investors (and, indirectly, the US government as guarantor of the MBS), not credit counselors or social workers trained to advise troubled debtors.

When Congress asks servicers to play babysitter to delinquent borrowers, they unilaterally impose the operational and compliance cost of this task upon the mortgage industry and do so without compensation or apology.

As Director Calabria said to Congress last September, if you don’t like the adverse market fee, then pay for the CARES Act. Members of Congress did not respond to Calabria’s challenge.

As the federal and state forbearance periods end, the industry will get hit from all sides by operational and political hazards caused by the political act of debt moratoria. If foreclosure moratoriums last longer than loan payment forbearance, for example, servicers will struggle to meet investor timelines & state law regulations.

Servicers will blow through contractual obligations to investors and guarantors because of the conflicting requirements of the CARES Act and state law moratoria. Further, because of the vast disruption to the legal community caused by loan forbearance in 2020, servicers, attorneys, custodians and courts will not be able to handle the surge in foreclosure caseload. Delays and errors will result in operational issues and consumer confusion and anger – all because nobody in Washington bothered to ask what debt relief under the CARES Act and state law moratoria would really cost.

After a year of minimal foreclosure volumes, law firms will be unable to execute according to investor and insurer timelines. Between one third and half of law firm staff related to foreclosures were furloughed during the past year, according to some estimates.

It will be difficult for foreclosure firms to ramp up in advance of the moratorium end date, especially since nobody in Congress or the states seems to know when that will be precisely.

Court backlogs and delays will extend the foreclosure timelines, creating increased costs to investors, insurers and servicers. The debt collection part of a mortgage servicer’s business will suddenly be taken from zero to 100% capacity and more. A lack of orderly wind down from foreclosure moratoria could flood the market with housing stock, result in abandoned properties and neighborhood blight, something that has not been seen since the great financial crisis of 2008.

What can be done to improve this situation and speed the resolution of COVID forbearance loans that do not get back on track?

First, the FHFA and FHA should eliminate trial modifications for all payment forbearance and foreclosure programs for conventional and government loans. Most of these trial modifications do not succeed with profoundly troubled borrowers and add complexity to the process.

Second, enable and empower the mortgage servicers to provide the customer up front with all options available to them and allow the consumer to choose what's best for their circumstance. By putting aside the idea of trial modifications and instead immediately acting in the best interest of the consumer, the interests of the note holder and guarantor will often be best served as well. That is, 1) protect the home and 2) act to maximize the net present value of the note.

The proposal to embrace a national policy for streamline refinance may seem obvious, but there remains a lot of resistance to embracing a broad national refinance strategy instead of loan modifications because large MBS investors dislike prepayments.

As we’ve noted previously in The Institutional Risk Analyst, the effective yield on MBS is currently negative due to high rates of prepayments ("Negative Returns are Now In US Mortgages"). If you pay 104 for the MBS thanks to QE from Fed Chairman Jay Powell and the FOMC and get prepays at par, then you are losing money.

All investors and insurers should mirror the FHA in opening up COVID streamline options regardless of delinquency status. By refinancing all agency and government loans down to current market rates, mortgage industry can enhance the credit of the entire national portfolio and save some, but not all, borrowers from foreclosure.

Ultimately it is the bond holders that are picking up the cost of COVID c/o the FOMC, but we think the folks at PIMCO, Black Rock (NYSE:BLK) and the Bank of China can fend for themselves. By kicking the can down the road, we at least buy time for the borrower and also allow the servicers to generate more revenue by re-pooling the new loan into a new MBS.

More than anything else, simplifying how we deal with COVID forbearance loans will save IMBs and the entire mortgage industry, including MBS investors, time and heartache in terms of risk and litigation.

Of course, progressives will never agree to such a streamline refinance strategy, no matter how good it may be for consumers, because members of the trial bar are one of the main sources of political contributions to the Democratic Party.

Yet unless we simplify and focus the role of the servicer when it comes to COVID loans on serving the best interests of investors and consumers both, IMBs and global investors may soon follow the example of commercial banks in fleeing the world of mortgage finance. Again, without IMBs and large bond investors, there is no US housing market.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.