Financial Risk Monitor Summary (Across 3 Durations):

- Short-term (WoW): Positive / 6 of 10 improved / 4 of 10 unchanged

- Intermediate-term (MoM): Neutral / 3 of 10 improved / 3 of 10 worsened / 4 of 10 unchanged

- Long-term (150 DMA): Negative / 5 of 10 worsened / 2 of 10 improved / 2 of 10 unchanged / 1 of 10 n/a

We are making two notable changes to the Risk Monitor this week.

1) Durations – We now look at changes over three durations: short term (TRADE), intermediate term (TREND), and long term (TAIL).

Short term: week over week

Intermediate: month over month

Long term: 1-month slope of 150 DMA

2) New Series - We are adding two new series we believe are helpful in managing risk: the Baltic Dry Index, which measure shipping rates of bulk dry goods, and Sovereign CDS.

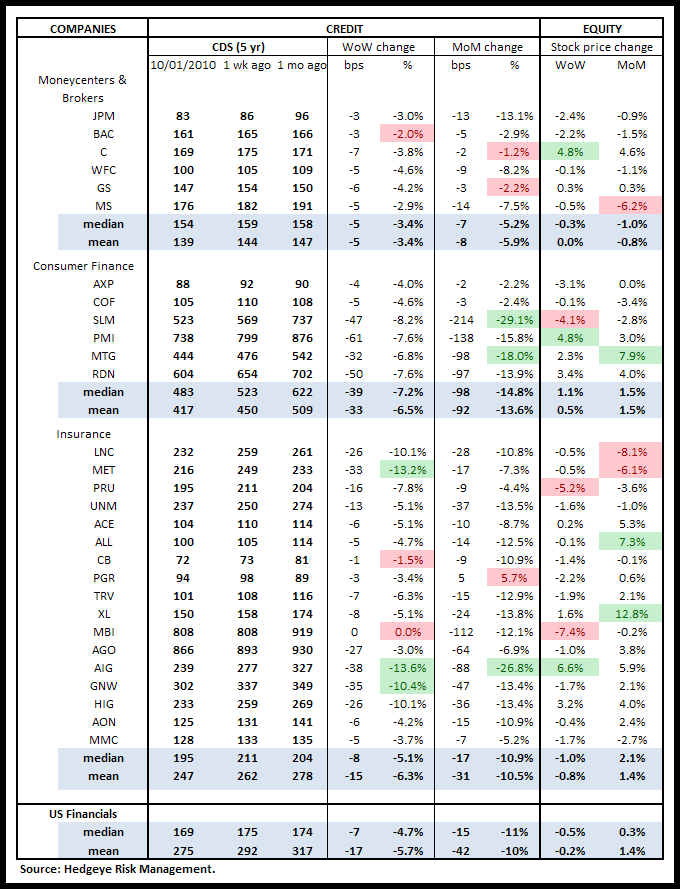

1. US Financials CDS Monitor – Swaps were nearly all positive last week. Swaps tightened for 28 of the 29 reference entities and remained unchanged for one (MBI). Conclusion: Positive.

Tightened the most vs last week: MET, AIG, GNW

Tightened the least vs last week: BAC, CB, MBI

Tightened the most vs last month: SLM, MTG, AIG

Tightened the least vs last month: C, GS, PGR

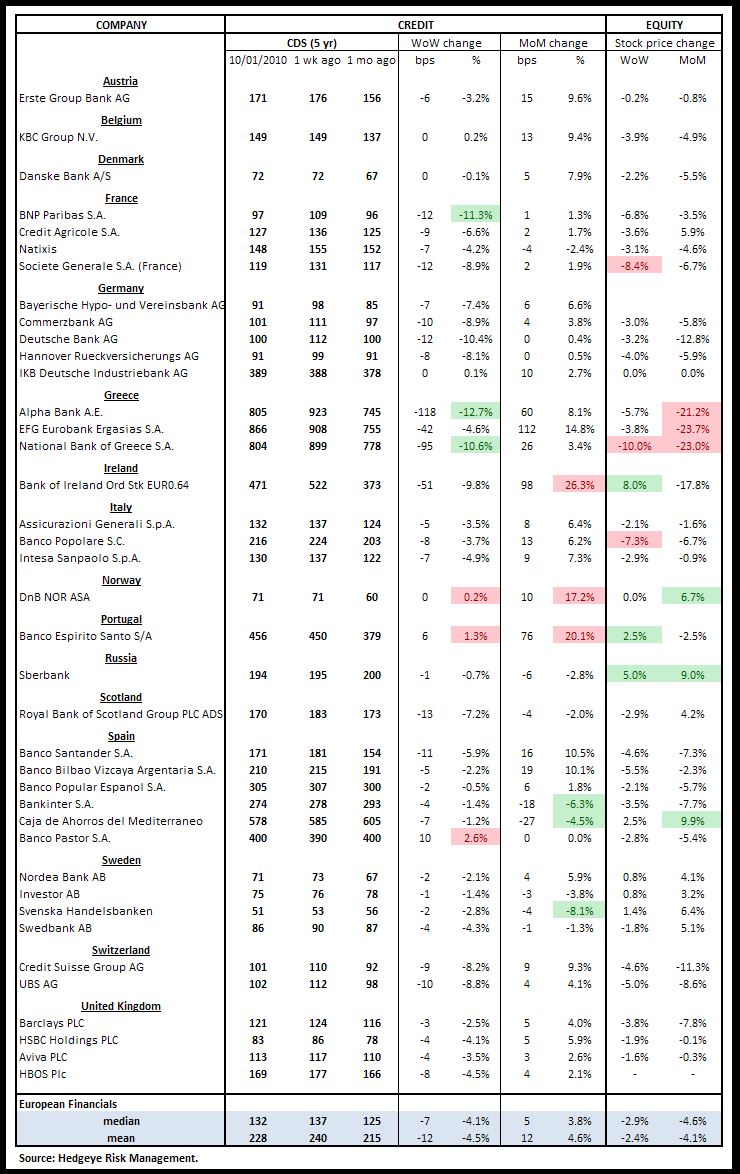

2. European Financials CDS Monitor – In Europe, the pattern was similar. Swaps tightened for 34 of the 39 reference entities tightened and widened for the only 5. After the Greek banks led the pack in CDS widening last week, two of the three were among the best performers this week. Conclusion: Positive.

Tightened the most vs last week: BNP Paribas, Alpha Bank A.E., National Bank of Greece

Widened the most vs last week: DnB NOR, Banco Espirito Santo, Banco Pastor

Widened the most vs last month: Bakinter S.A., Caja de Ahorros del Mediterraneo, Svenska Handelsbanken

Tightened the most vs last month: Bank of Ireland, DnB NOR, Banco Espirito Santo

3. Sovereign CDS Monitor – Sovereign CDS fell 10 bps on average last week, led by Ireland, Portugal, and Greece. Conclusion: Positive.

4. High Yield (YTM) Monitor – High Yield rates fell last week, closing at 8.19 on Friday. Conclusion: Positive.

5. Leveraged Loan Index Monitor – The leveraged loan index rose 7.1 points last week. Conclusion: Neutral.

6. TED Spread Monitor – Last week the TED spread fell slightly, closing at 14 bps. Conclusion: Neutral.

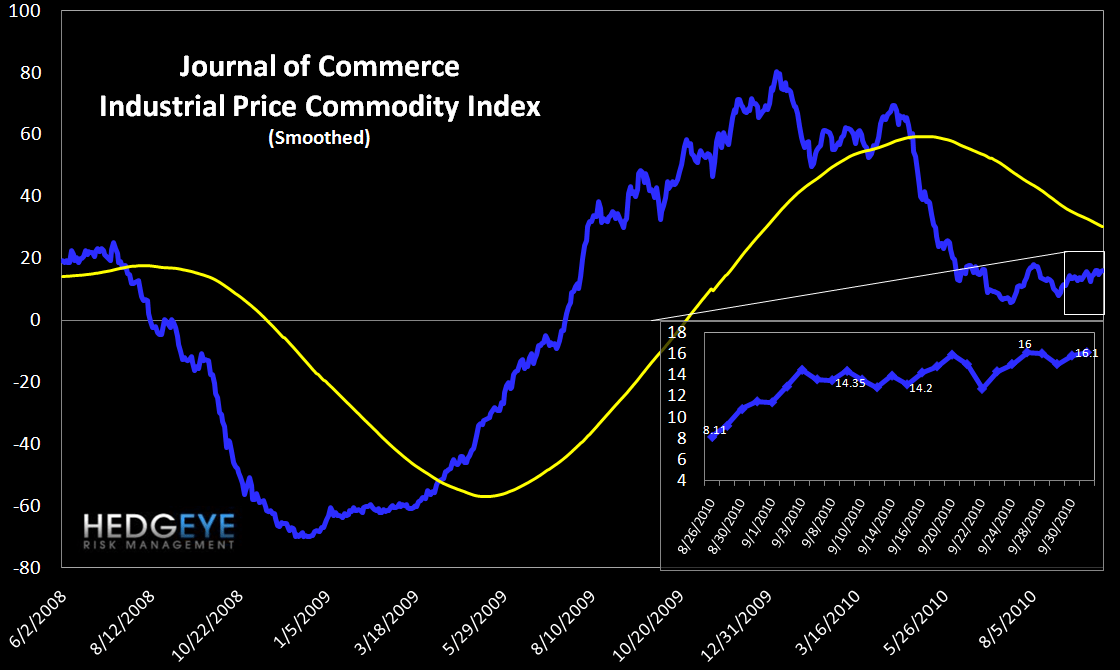

7. Journal of Commerce Commodity Price Index – Last week, the index rose 1.1 points, closing at 16.1 on Friday. Conclusion: Positive.

8. Greek Bond Yields Monitor – We chart the 10-year yield on Greek bonds. Last week yields fell 90 bps, ending the week at 1015 bps versus 1105 bps the prior week. Conclusion: Positive.

9. Markit MCDX Index Monitor – The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on four 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. Our index is the average of their four indices. Spreads were up slightly last week, closing at 217 versus 215 the prior week. Conclusion: Neutral.

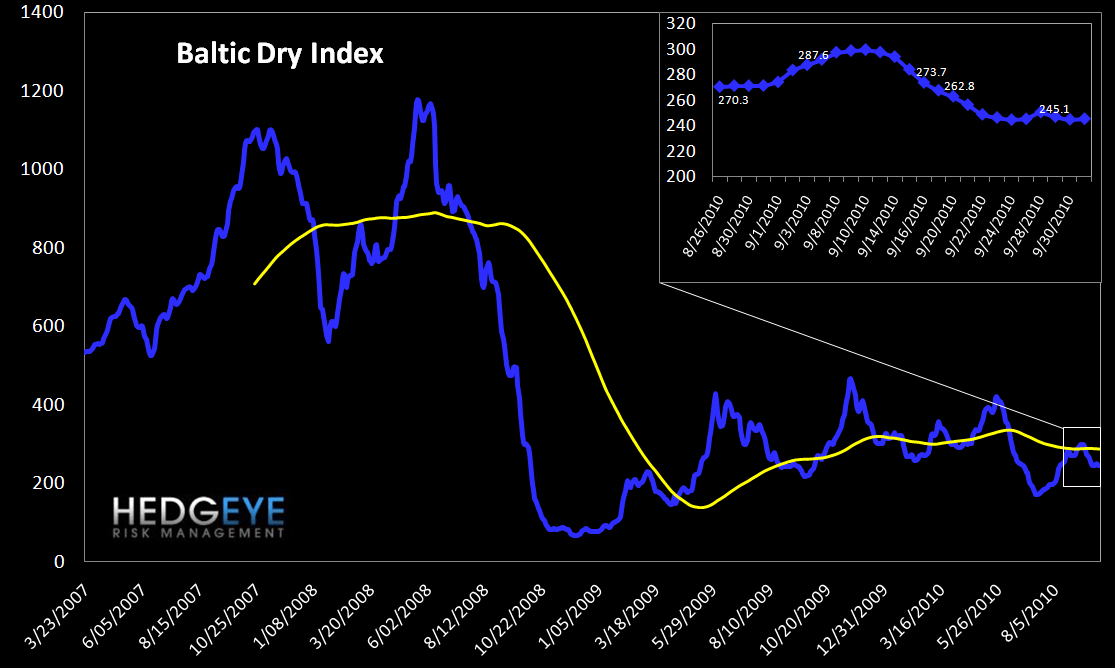

10. Baltic Dry Index – The Baltic Dry Index measures international shipping rates of dry bulk cargo, mostly commodities used for industrial production. Higher demand for such goods, as manifested in higher shipping rates, indicates economic expansion. Last week the index rose a hair, closing at 245. Conclusion: Neutral.

Joshua Steiner, CFA

Allison Kaptur