Conclusion: Recent data points suggest that industry sales trends continue to improve, especially for the more upscale, well positioned concepts. The most recent consumer conference data points are a clear indicator as to why.

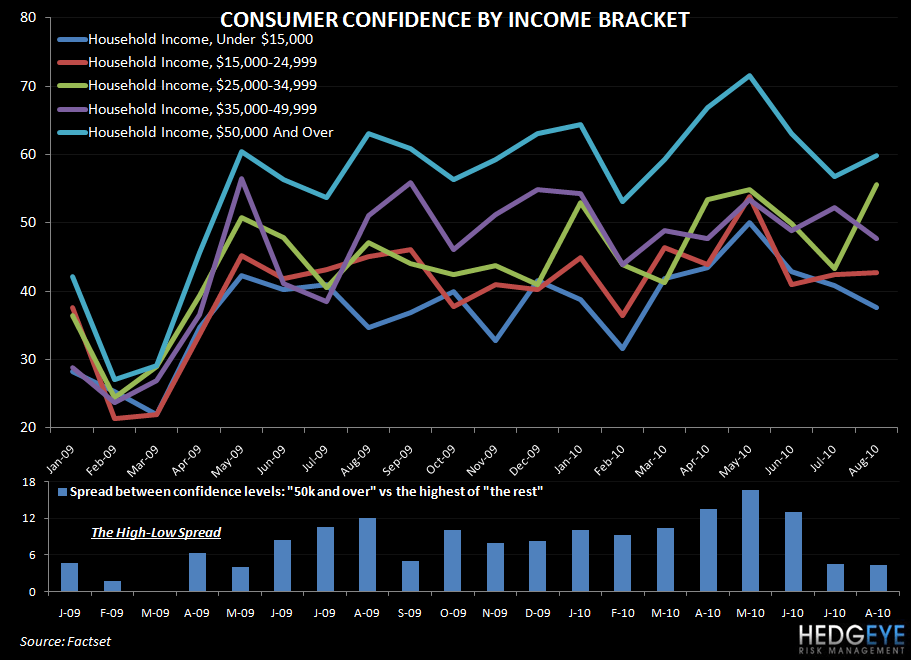

Consumer confidence continues to be one of the key metrics that management teams look at to predict future sales trends. As is evident from the chart below, the spread between the confidence levels in the top income bracket versus those in other income brackets has generally expanded during the last couple of years.

The message has been clear throughout this “recovery”: the higher socio-economic strata have been leading the upturn while lower classes continue to struggle. There are a number of datasets to point to in this regard; participation in the Supplemental Nutrition Assistance Program is probably the most telling. As of June 2010 there were over 41 million Americans participating in the program. The bifurcation in restaurants sales trends has reflected this reality but, going forward, it is possible that the space may start to see a convergence in performance across average check levels. If the spread between confidence levels in the $50,000 and over income bracket and confidence levels in the other income brackets continues to converge, it could have a marginally negative impact on sales trends in higher-end restaurants. A return to the scenario shown in early 2009, below, where all brackets are tracking closely in terms of confidence, would imply a slowing in sales trends at higher end concepts which have been outperforming, accordingly, as high income confidence levels have outstripped the other income brackets’ confidence trends.

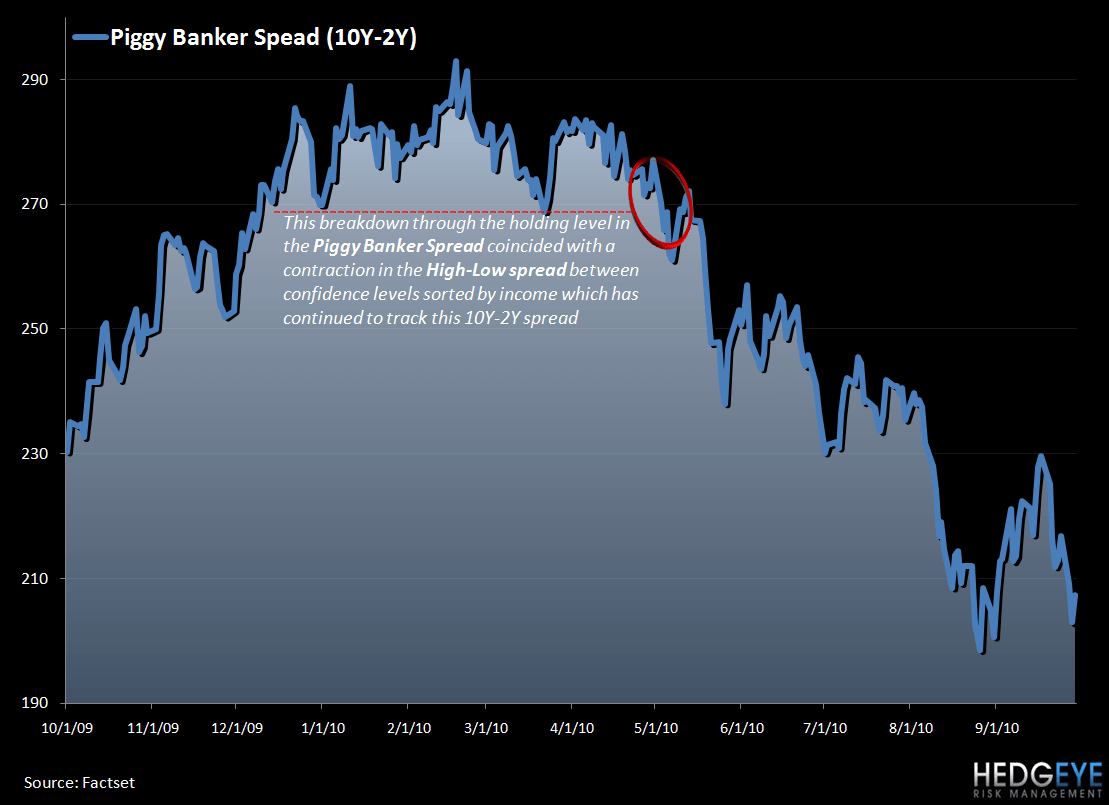

It is interesting to note that the surge in confidence among the “$50,000 and over” income bracket has tracked, and continues to track, what we call “the piggy banker spread”, or 2-10 yield spread, very closely. It is important to note that this spread has been compressing since the first quarter of 2010, moving meaningfully downwards since midway through the second quarter. The ensuing trend augurs poorly for the financial industry which is a negative for business traffic in casual dining – particularly for MRT. Josh Steiner, head of Financials at Hedgeye, believes that the headwind of sequential declines in the yield spread will grow in significance “as it affects most companies on a lag”. An article published today in The Wall Street Journal titled, “Wealthy Take a Bigger Helping of Fast Food”, underlines this point. A survey conducted by American Express revealed that 24% of “ultra-affluent” consumers boosted their fast-food spending by 24% in the second quarter, compared with the year-earlier period versus 8% growth among the rest of U.S. consumers. A senior executive of American Express Business Insights, Ed Jay, said that while a lot of affluent consumers are trying to spend less on food by frequenting quick-service restaurants and discount retailers, they continue to spend on air travel and luxury items. “Ultra-affluent” is defined as consumers who charge $7,000 or more per month to their cards and meet certain income criteria.

During the last few days we have heard some commentary from management teams on their macro outlook. Some insights worth repeating include:

- “The best evidence of that [Darden’s good position in consumer space] is how well the industry has performed during the economic downturn compared to some other important consumer-related industries” -- Clarence Otis, Darden CEO, 9/29

- “We expect meaningful same-restaurant improvement this year [at Capital Grille], as business and luxury spending continue to rebound” -- Clarence Otis, Darden CEO, 9/29

- [On business activity continuing to grow in 2011]: “People are going to get on the road. They’re going to get on planes, they’re going to get on trains, they’re going to be staying in hotels. And once again, if people are out on the road trying to grow their top line, some of them are going to fall into our restaurant” -- Bert Vivian, P.F. Chang’s China Bistro CEO, 9/29

- “Companies need to get out on the road. I have heard from many, many businesses…we are seeing it. We are seeing it in our private board room and our Monday through Thursday business. That’s our higher margin business. The Monday through Friday business is typically the business traveler” -- Ron Dinella, Morton’s Restaurant CFO,9/29

Despite the fact that most restaurant companies have guided to improved same-store sales growth in the back half of the year, it was surprising to hear overwhelmingly positive comments out of most of the companies presenting over the last few days in light of the reported decline in consumer confidence.

As I said yesterday, PFCB’s Co-CEO Bert Vivian sounded modestly optimistic about 2H10 and FY11 top-line trends for PFCB and the overall industry. Morton’s reaffirmed its +4-6% FY10 comp guidance, which implies a sharp improvement in two-year average trends in the back half of the year. After the company reported 2Q10 results, I said this guidance seemed aggressive, but management is now maintaining this guidance after nearly completing its third quarter.

This optimism only affirms the high-low society thesis, however, as both PFCB’s Bistro and Morton’s draw a large proportion of its guest counts from business travelers. At the Bistro, about 30% of tickets end up on expense accounts versus about 80% for Morton’s. Contrasting this more positive outlook, the best news that both JACK and WEN could provide was that trends appear to be stabilizing.

Both RT and CHUX, which are situated in the middle of MRT and QSR in terms of average check, talked about their outlook for improved trends but at the same time, they hedged those comments by highlighting the difficult economic environment. Specifically, RT management said the world is going to be sluggish for the next 3-5 years, or as long as deleverage takes, but that it is seeing a little upside relative to earlier in the summer. CHUX management stated that the environment is still challenging and as a result of high unemployment, falling home values and declining confidence, consumers are dining out less and are chasing more value. That being said, he said there was a positive shift in momentum in 2Q, which he expects to continue into the second half.

Reflecting the casual dining industry as a whole, DRI said on its fiscal 1Q11 earnings call that industry same-store sales trends are improving faster than it had expected and the bulk of that growth is being driven by better performance among the higher average check concepts.

Howard Penney

Managing Director