|

Editor's Note: Below is a brief excerpt from a complimentary Health Policy Unplugged note written by our Health Policy analyst Emily Evans. |

The very last place you want to look for disruption in health care is an insurance company.

However, the natural temptation after watching CLOV go from $17 to $8 is to wonder if at least part of the story is true.

After a review of the state filings, the 4Q earnings call and the Clover Assistant presentation last week, it seems hard to accept much of the story they tell. While one should never assign to malfeasance that which is easily explained by incompetence or indifference, it seems to us that being a public company requires at least some consistency and clarity between the official reporting and the story telling.

We have already highlighted the enrollment data that suggests a long road to profitability for a little insurance company in New Jersey. Making the path to profitability and, with it, true disruption much more difficult, if not impossible, are the ongoing underwriting losses, capital demands and the opaque approach to the Direct Contracting Program.

No nifty website is going to overcome these things, especially in the face of pent-up demand for medical care post-COVID.

Underwriting Losses & Capital Contributions

Based on disclosures made in state insurance filings, for 18 of the last 20 quarters, CLOV’s primary insurance unit, Clover Insurance Company (NJ) has experienced underwriting losses ranging from $323,000 in 2Q 2016 to $52,000,000 in 4Q 2019. While Wall Street generally expresses ennui in the face of consistent losses while pointing to some generally unreasonable TAM, insurance regulators are not nearly as accommodating.

|

Underwriting losses can and do trigger state requirements for additional capital contributions. According to NAIC filings, the company accepted capital contributions totaling $235 million between ~2015 and 2020. Additionally, sometime before 1Q 2016, the insurance subsidiary received $40 million in return for a “surplus note.” These capital contributions were made by CLOV, the parent company, to the insurance subsidy. While the original source of the funding is not disclosed, the S-4 indicates that on “December 27, 2018, CLOV entered into a Convertible Agreement with qualified institutional buyers, including entities affiliated with the Corporation for an aggregate principal amount of up to $500 million to support the Corporation’s growth in the MA market.” |

Without additional details to clarify what “growth in the MA market” means or meant, it is uncertain what the intended uses of up the $500 million are. One possibility, of course, is to wrap all previous capital contributions into a single security class with some optionality for those that contributed the capital for regulatory purposes.

The S-1 filed by CLOV in January, indicates $373 million in convertible preferred notes due in 2023, the year CLOV had estimated in October $1.7B in revenue, which given enrollment trends seems optimistic.

Direct Contracting

The Direct Contracting opportunity celebrated by CLOV remains difficult to understand given what we know about the program. If we are understanding what they have said it will work like this:

Step 1. CLOV will be admitted to the new Direct Contracting Model as a “New Entrant,” that is an entity with less experience working with the Medicare FFS population.

Step 2. CLOV will construct a network of sorts based on use of the Clover Assistant. A primary care physician that uses the CA will be considered part of CLOV’s Direct Contracting Entity, Clover Health Associates, a New Jersey Internal Medicine practice. (Note: In the earning’s release, CLOV called the DCE entity Clover Health Partners but we can find no practice by that name in the NPPES database.) What other contractual obligations there would be is not clear.

Step 3. Fee-for-Service beneficiaries served by the practices that use the Clover Assistant would enroll in the direct contracting program or be assigned by CMS. The Direct Contracting description provided by CMS suggests beneficiaries enrolled with a New Entrant DCE would primarily do so voluntarily. CLOV indicated in the presentations covering the program, that participants would be identified through claims which may be possible but clearly not the primary mode as far as CMS is concerned.

Step 4. Somehow, CLOV would manage the risk associated with caring for Medicare enrollees on a capitated basis. How they do so would depend on exactly what primary care physicians expect or agree to as part of being in CLOV’s “network.” Given the rather loose arrangement with Primary Care Providers described by CLOV, it is difficult to understand who will get paid what and when. More concerning, of course, is CLOV’s already demonstrated inability to manage the risk they have now. MLR for 4Q 2020 was an eye-popping 109%.

If you have any greater insight into how the CLOV Direct Contracting program will work, by all means share.

There are other strange turns in the story of CLOV. Descriptions of the Seek Insurance Services relationship are contradictory and inconsistent with official filings. The related party disclosures are incomplete and require follow-up.

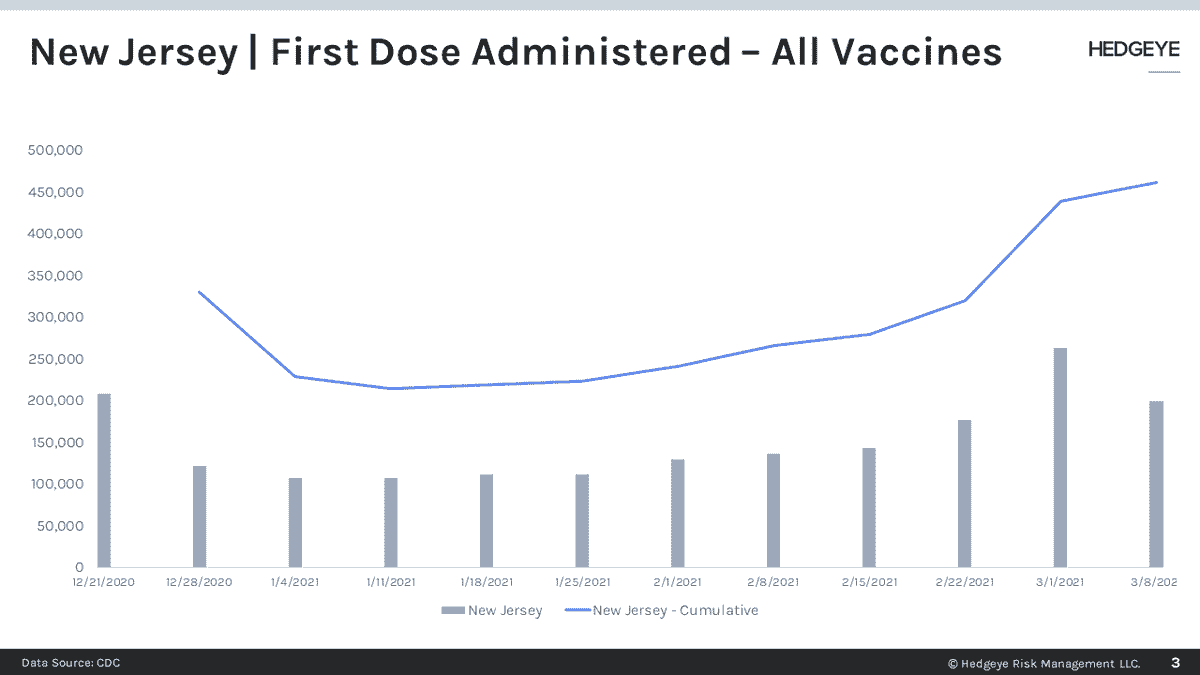

What really matters is that as vaccine administration proliferates, particularly in the northeast and people begin their return to in-person care, the lack of pricing power derived from having a network and the market influence to negotiate prices suggests that CLOV will be in no better position to manage their MLR than they were in 2020.

In fact, things could get worse. New enrollees are often the most expensive in a plan. The explosion in medical costs in 4Q 2020 was prior to the vaccine rollout in New Jersey. As the vaccine proliferates and the disease recedes more care and at higher intensity will be necessary.

Given CLOV’s weak management of their benefit costs, what cash resources the company has could be burned in a few quarters.

Let me know if you have any questions and please share any additional insight. CLOV is one of the stranger stories I have heard over the last few decades, and that is saying something.