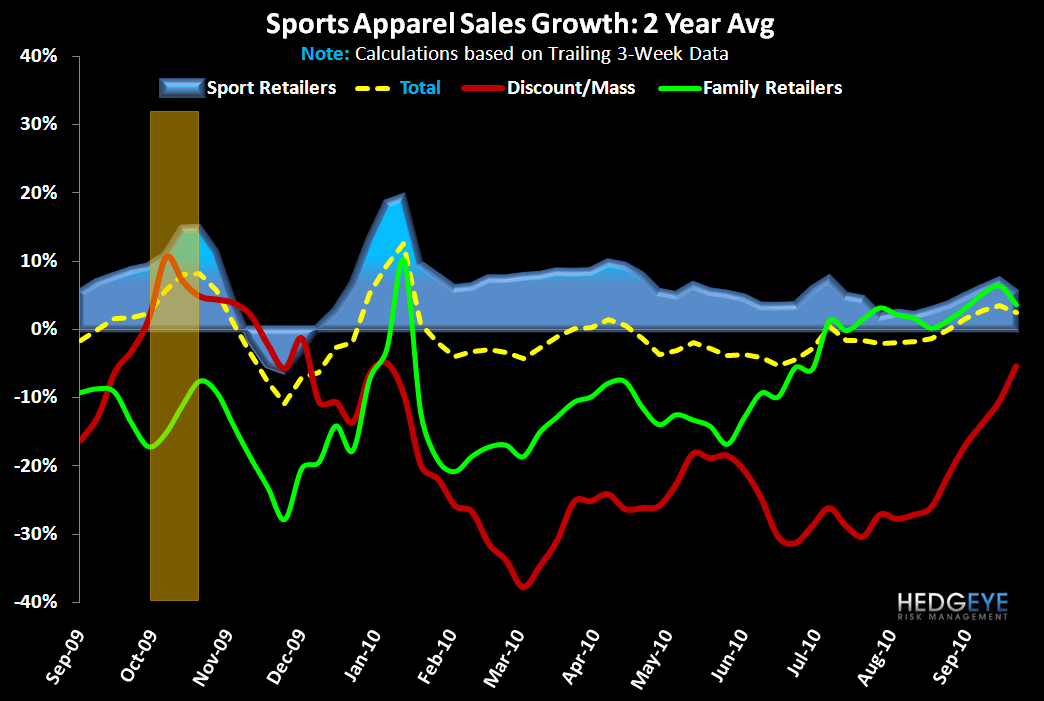

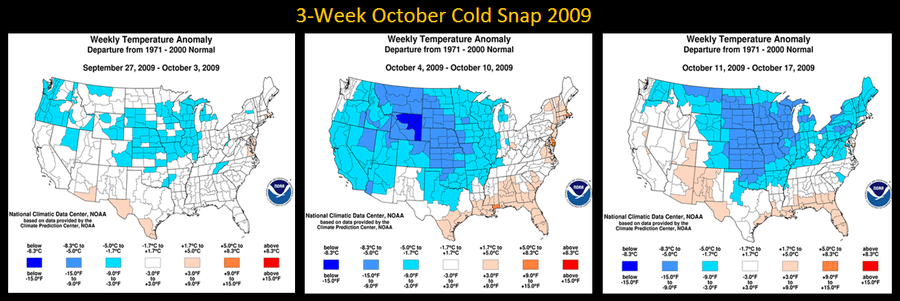

Despite what seems to be a meaningful erosion at face value, the underlying trend in sports apparel sales remains positive (+3%) on a trailing 3-week basis. While the week ending Sunday the 26th marked the greatest sequential deceleration since May 23rd, it’s important to note that at this time last year we saw the start of 3-week growth spurt brought on primarily by a nationwide cold snap through the first 3-weeks of October as well as UA’s shift into expanded fits beyond compression to fitted (non-compression) product. During that time last year, total sales accelerated from +2% this past week to +3%, +7%, and +15% while Sport Retailer sales ramped from +9% to +8%, +9%, and +19% as highlighted in the charts below.

The biggest anomaly for the week is that the Athletic Specialty retailers underperformed the mass, discount and channels on the margin. Given that it’s only a week, this is not enough for us to challenge any of our models – but we’ll keep an eye on the trends to monitor any sustained channel divergence.

On a branded basis, sales slowed across the board sequentially. Additionally, a divergence in performance over the last two weeks has emerged with Under Armour outpacing Nike – something that we’ll be watching closely in the next few weeks but expect to moderate. Why? Recall UA introduced its expanded offering of fitted (non-compression) product in mid-October. This in turn drove sales up +56% the week ending October 18 and trailing 3-week trends materially higher. The product intro also added nearly 5% to an already strong base. At the same time Nike increased 18% driven by accelerated growth in the family channel most likely reflecting the clearance of underperforming product. Now we’ve got Nike sporting a 20%+ growth rate in its North American futures.

As much as we try to avoid the weather card, we can’t ignore temps hitting record highs in certain parts of the country as we start to anniversary unseasonable cooler weather. That said, October will be an important month for UA as it comps its toughest month of the entire year.

Casey Flavin

Director