This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

Over the past several weeks, the US treasury market has shown increasing discomfort with the direction of the Biden Administration and the Congress on fiscal matters.

Somehow absurd fiscal policy in Washington was not a problem for global capital markets during four years of President Donald Trump, but that benevolent situation appears to have reversed in the first three months of President Joe Biden’s tenure.

The Treasury’s fiscal posture is verging on the ridiculous thanks to both parties in Congress. Even as the economy rebounds and banks show little credit impact from COVID -- so far -- the Democrats in Congress want their trillions in spend to match the profligacy of President Trump.

The judgement of the markets on Biden and Treasury Secretary Janet Yellen, however, was illustrated in the nearly failed auction of 7-year Treasury notes at the end of February.

“A big move came in the early afternoon when an auction for $62 billion of 7-year notes by the U.S. Treasury showed poor demand, with a bid-to-cover ratio of 2.04, the lowest on record according to a note from DRW Trading market strategist Lou Brien who called the result "terrible," reports Reuters.

Even before the auction, Reuters reports, yields on five-year and seven-year notes, the "belly" or middle of the curve, had risen significantly, following weak demand for a 5-year auction.

As investors shunned the recent Treasury auctions, primary dealers were left holding more than half of the paper. And it was at this juncture that the idea of Operation Twist magically reappeared on the scene, but so far only as rumor.

We hear that Operation Twist 3.0 was discussed by the FOMC, but our colleague Ralph Delguidice says nothing has been decided as yet.

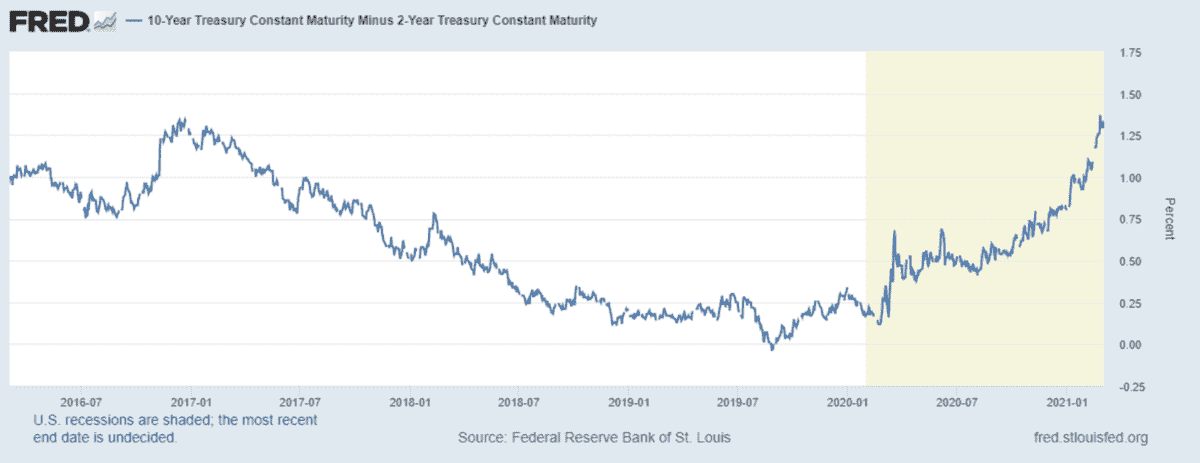

With the yield spread between 2-year Treasury notes and the 10 year as wide as seen in seven years, the markets have unceremoniously puked all over the idea of further deficit spending to address the quickly receding COVID crisis. Thus, the FOMC it seems must now ride to the rescue of the Treasury.

Most news reporters and economists will tell you that the FOMC’s purchases of Treasury debt and mortgage-backed securities (MBS), which is labeled "quantitative easing," are some sort of economic policy action.

In fact, the Fed’s purchases of Treasury debt represent a subsidy to the US government at the expense of private investors. And as the Treasury’s fiscal situation grows ever more precarious, the FOMC is forced to essentially maintain a market in Treasury debt when the primary dealers are overwhelmed. Like right now.

In one sense, we should all treat the selloff in bonds over the past couple of weeks as a gift, a rare buying opportunity borne of volatility the occurs amidst the general drought of duration engineered by the Federal Reserve Board.

Think of the Federal Reserve Bank of New York as a giant financial sump pump, sucking the available duration from the Treasury debt and agency MBS market in vampiric fashion. The Fed then remits the income from these assets to the Treasury, depriving private investors of a return. A remarkable form of stimulus indeed.

But more important than the transfer of interest income to Treasury is the emerging fact of the FOMC standing ready to unconditionally support new US debt issuance in the bond markets. This is a disturbing development for all investors in dollar denominated assets.

Like a great black hole in space-time, the FOMC is sucking the resources out of the private economy in order to feed public sector deficits in Washington. President Biden and Italian Premier Mario Draghi have more in common than they know.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.