“The mathematical expectation of the speculator is zero.”

-Louis Bachelier

Louis Bachelier was a French mathematician who was, well after the fact, credited with founding the Efficient Market Thesis. In 1900 Bachelier published his Ph.D thesis titled “The Theory of Speculation.” In his paper, Bachelier discussed the use of Brownian motion to evaluate stock prices. Unfortunately, his thesis was “not appropriately received”, which resulted in academic black-balling and the concept being buried for more than sixty years.

Almost sixty-five years later Professor Eugene Fama from the University of Chicago was officially credited with developing the Efficient Market Thesis after publishing his Ph.D thesis. His paper was titled “The Behavior of Stock Market Prices.” The core tenet of his paper and the Efficient Market Thesis is that an investor “cannot consistently achieve returns in excess of average of market returns on a risk-adjusted basis, given the information that is publicly available at the time the investment is made.”

Is it not somewhat ironic that the determination of who founded the Efficient Market Thesis was not efficient?

Despite not having a Ph.D on staff at Hedgeye Risk Management, we have been performing our own experiment to test the Efficient Market Thesis over the past two years. We call this experiment the Hedgeye Virtual Portfolio, and it is a culmination of our stock picks since inception.

In that time, we have closed 510 long positions and closed 490 short positions. 85.9% of the closed long positions have been winners and 83.5% of the closed short positions have been winners. Obviously, these results are far from a “random walk”. So, either we are good at our jobs, or the market is not quite as efficient as Efficient Market Theorists believe. I would submit that it is a combination of both.

Clearly, though, many stock market participants work hard, have processes, and are intelligent. So, why do many stock market operators underperform even the basic broad market returns? Simply put, because of this little critter called Behavioral Economics that leads many market participants to act against their best interests.

By way of example, let’s consider the St. Petersburg Paradox, which is as follows:

“Consider the following game of chance: you pay a fixed fee to enter and then a fair coin is tossed repeatedly until a tail appears, ending the game. The pot starts at 1 dollar and is doubled every time a head appears. You win whatever is in the pot after the game ends. Thus you win 1 dollar if a tail appears on the first toss, 2 dollars if a head appears on the first toss and a tail on the second, 4 dollars if a head appears on the first two tosses and a tail on the third, 8 dollars if a head appears on the first three tosses and a tail on the fourth, etc. In short, you win 2^k−1 dollars if the coin is tossed k times until the first tail appears.”

So, what would be a fair price to pay for entering the game?

I posed this question to our Research Team at Hedgeye yesterday and they came back with myriad of answers, which ranged from $1 to infinity. This simple mathematical answer is that you should be willing to pay infinity (or your entire net worth) to play this game as your expected value is infinity.

As one of our astute Analysts responded to me yesterday:

“Well, the series doesn’t converge …EV = (1/2)*($1) + (1/4)*($2) + (1/8)*($4) + …EV = ½ + ½ + ½ + …… the sum of which is infinite. So, is the fair entering price infinite? Strictly speaking, I think the answer is yes – but no one on earth would take that deal (even if we cap the number of rounds such that EV = all your money, since no one has infinite money).”

Therein is another paradox, the paradox of the Efficient Market Thesis. Specifically, most market operators do not make rational decision based on math. They make emotional decisions based on arbitrary evaluations of risk. This, of course, leaves opportunities for the sneaky mathematicians to make profit.

So then, how do we account for valuation when considering an investment? Surely, valuation is rational?

In my view, valuation is an indicator of sentiment around a security. For instance, when a stock trades with a single digit P/E, its business is either declining, or the collection of market operators believe it is. There are many studies that support the idea that value based strategies (i.e. buying cheap stocks) outperform over time, but I would submit that this is not because of the valuation, but rather because of the behavioral finance indicator embedded therein.

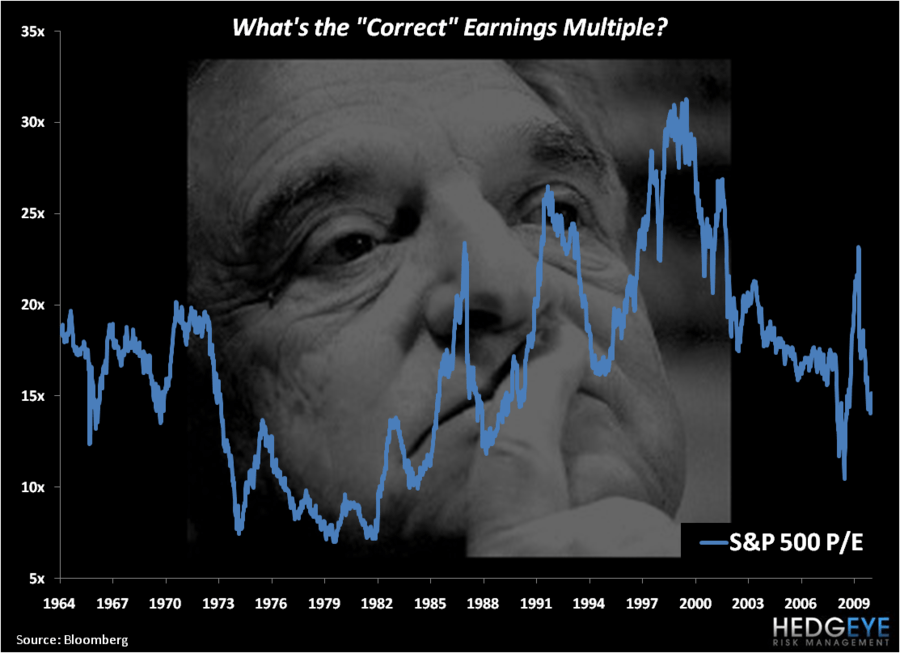

As we consider the stock market today, the first question many strategists try to answer is whether the stock market is “cheap”. The simple way to make this determination is to pull up a long term price / earnings chart and look at it going back fifty years. Today, at 15x current earnings and 13.7x forward earnings, the SP500 looks cheap versus history.

The more important task though is determining what expectations are embedded in that valuation. What is the correct earnings multiple for an economy that has crossed the Rubicon of Debt at 90% debt / GDP and has budget deficits projected for the next thirty plus years (I would say infinity, but that’s probably not fair)? Additionally, if growth rates are mired in the 1 - 2% range as a result of this fiscal situation, is the stock market “cheap”?

In the shorter term, setting those sneaky valuation metrics to the side for a second, what do you think is priced into the S&P500 up 8.8% in September? Given the cover of Barron’s this weekend and the rapid rise in the S&P in the last few weeks, the catalyst of the Republicans winning more seats than expected in the midterms is likely priced in. (We called this out on our conference call with Karl Rove in early September - Could the Midterm Election Be A Major Stock Market Catalyst?) So, what is priced in now?

Well, perhaps our friend George Soros said it best:

“The financial markets generally are unpredictable. So that one has to have different scenarios. The idea that you can actually predict what's going to happen contradicts my way of looking at the market.”

Or as we say at Hedgeye, the plan is that the plan will change.

Yours in risk management,

Daryl G. Jones

Managing Director