"The lesson that I have learned is that it isn't reasonable to be agnostic about the big picture."

-David Einhorn

There was an article in the Wall Street Journal on Friday that was forwarded to me hundreds of times over. The article was titled “Macro Forces In Market Confound Stock Pickers.” There was nothing particularly new in the article. Everyone who has protected their client’s hard earned capital in the last 3 years gets that macro matters. But what about those who don’t get it? What’s their answer to David Einhorn’s mental flexibility? Do their answers matter?

Macro Forces certainly matter. As Risk Managers, it’s our job to both identify their market impact and proactively prepare for their most “improbable” outcomes. I have a great deal of respect for someone like Einhorn because he can skate circles around Captain Stock Picker out there but, at the same time, acknowledge that he needs to continually evolve his investment process to incorporate the macro frontier.

If you are a bloodhound who trades merger arbitrage or your job is to be long of the next stock to hit this market’s broadening “rumor mill” of takeout targets, that’s fine. Maybe you don’t do macro until, as Mike Tyson would say, it “punches you in the face.” For the rest of us, “it isn’t reasonable to be agnostic” about global macro market risk anymore. October 1987 mattered.

Being Duration Agnostic is also something we evangelize a lot here in New Haven. My sense is that the Buy-And-Hope model of yesteryear isn’t going to be emailed to me 100 times over via a WSJ article anytime soon. Legacy print media has a funny way of being a lagging indicator. All that said, we need to focus intensely on compartmentalizing calendar catalysts that are macro in nature. It’s unreasonable to actively manage risk otherwise.

During Friday’s US stock market short squeeze I was also getting a lot of emails asking me when I was going to short the SP500 (SPY). After 3 consecutive down days (Tuesday, Wednesday, and Thursday), the illiquidity rally was broad based and I think the questions were well timed.

Unfortunately, I’m not enough of a cowboy anymore to stand on the other side of this market’s intermediate term TREND line and call it anything other than what it became on Friday – what was 1144 resistance in the SP500 is now support.

It’s not my job to be bearish or bullish. It’s really not my job to be anything other than a student of whatever it is that Mr. Macro Market throws at me each and every day. There certainly were more bearish than bullish fundamental research data points in my notebook last week but at the end of the week they were all trumped by Mr. Macro’s market price. The US Dollar has been demolished (down 14 of the last 17 weeks) and the reflation trade is back on.

To be crystal clear, there are no rules in this game suggesting that the 1144 line cannot become resistance again. The Macro calendar of catalysts for the early part of this week that could easily be construed as bearish are:

- Monday: A breakdown close through 1144 on the SP500 combined with a failure of the VIX to breakdown through its critical 20.77 line of support.

- Tuesday: A reminder that Housing Headwinds remain in the US economy with the Case Shiller report for July.

- Wednesday: An acknowledgement by both Japan (Tankan Survey) and the US (Obama speaks on joblessness) that Fiat Republics are not stable.

Then, of course, you have month and quarter-end on Thursday for the hedge fund business on top of a Chinese PMI report for September that could go either way. No one said that doing macro is easy. The way we all get paid in this business, it shouldn’t be…

The Macro Forces that are bullish out there are fairly straight forward at this point:

- Prices: The SP500 is up +9.43% for September-to-date!

- M&A: Unilever buys Alberto Culver this morning for $3.7B making at least 1 of the 67 rumors of takeouts we are tracking true…

- Mid Terms: If you didn’t know the Republicans are going to take the House, now you know.

“Republican House” being on the cover of Barron’s this weekend certainly doesn’t make this a new Macro Force to consider. That’s why we did our risk management call with Karl Rove last month to get ahead of this. As always, the better questions in our risk management lives surround what people aren’t talking about. These factors, too, need to be considered on a Duration Agnostic basis.

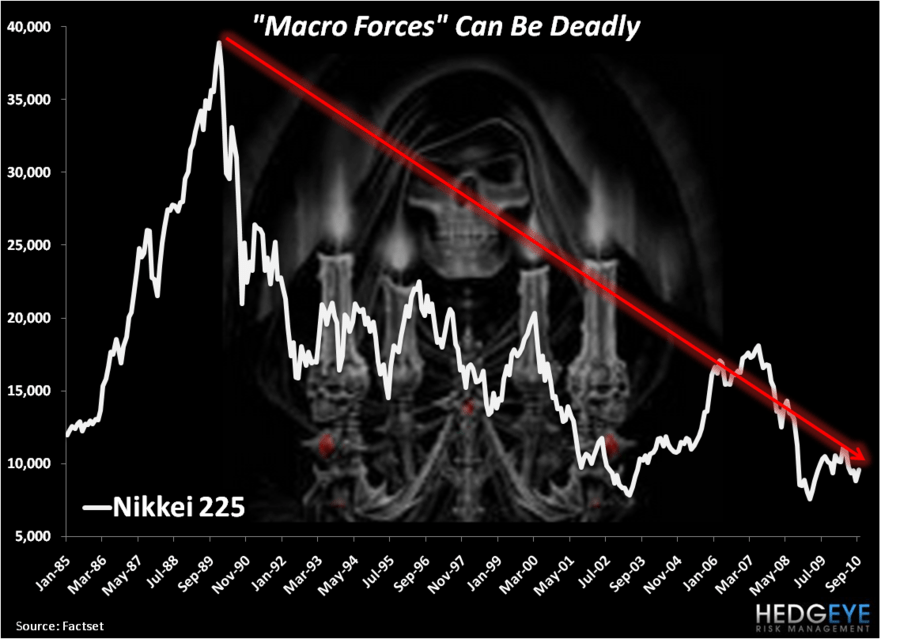

Whether or not the intermediate term TREND line in the SP500 of 1144 holds or not definitely matters to me in the immediate term. At the same time, out on the long term TAIL, the biggest question is why won’t the US stock market continue to make a series of lower-long-term-highs like the Nikkei in Japan has?

There are only 7 countries in the world who have underperformed Japanese equities for the YTD at this point (in order of worst to Japan: Greece, China, Slovakia, Italy, Portugal, Spain, and Ireland). Sadly, in response to another lower-long-term-high in the Nikkei, this morning the Japanese have introduced another 4.6 TRILLION Yen in stimulus. Shame on those who don’t learn history’s lessons. They deserve to lose.

My immediate term support and resistance lines for the SP500 are now 1131 and 1150, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer

This note was originally published at 8am this morning, September 27, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.