|

Below is an excerpt from a complimentary research note by our Healthcare Team of Tom Tobin, William McMahon, and Justin Venneri. We are pleased to announce our new Sector Pro Product Health Care Pro. Click HERE to learn more. |

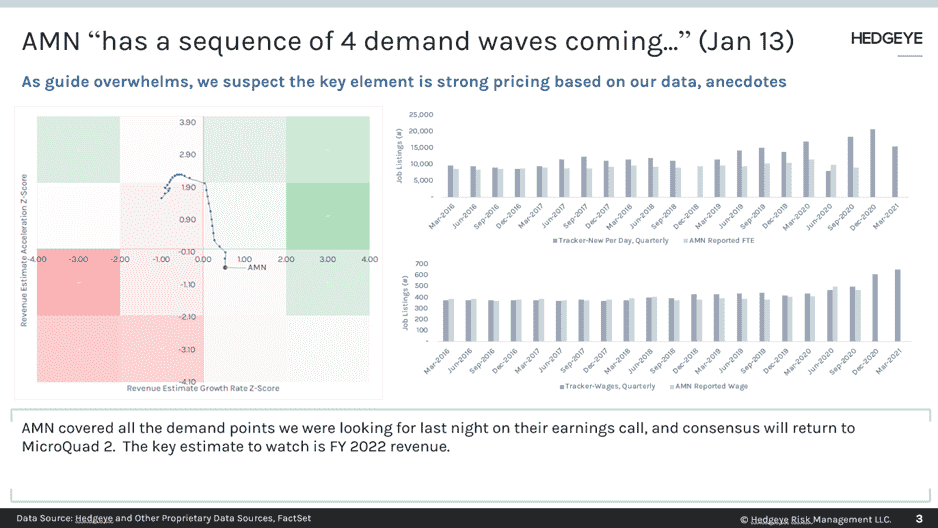

AMN remains a Best Idea Long. The beat was tremendous. AMN guided 1Q21 revenue well above consensus to $800MM-$820MM vs. consensus of $620MM.

COVID-19 has been a positive driver, but later in the call management indicated that they expect 2Q21 to trend well above the $605MM estimate.

“…when you take all into account, we would at this point, be thinking about second quarter revenue, something more in the low $700 million range. And all that would be down around 10% from the Q1 guide, that would still reflect year-over-year growth of around 15% to 20%.”

Management also pointed to other positive drivers like burnout, vaccinations, and the return to in-person care, corroborating our view that there were multiple waves of demand emerging for AMN as COVID-19 recedes.

As we’ve been hearing in our checks with physicians, staffing remains tight. Wages rates for AMN are rising 20% which we expect to persist through 2021 and into 2022.

The dynamics of deferred care will bring a wave of A) patients who have merely waited for a vaccine to return to a physician, and a rise of acuity that typically comes from waiting to see a doctor, and B) the long-term disability for COVID-19 patients, even for patients with milder cases.