<revised with correct chart below>

Hedgeye Portfolio: Long Germany (EWG); Long British Pound (FXB); bullish on EUR-USD

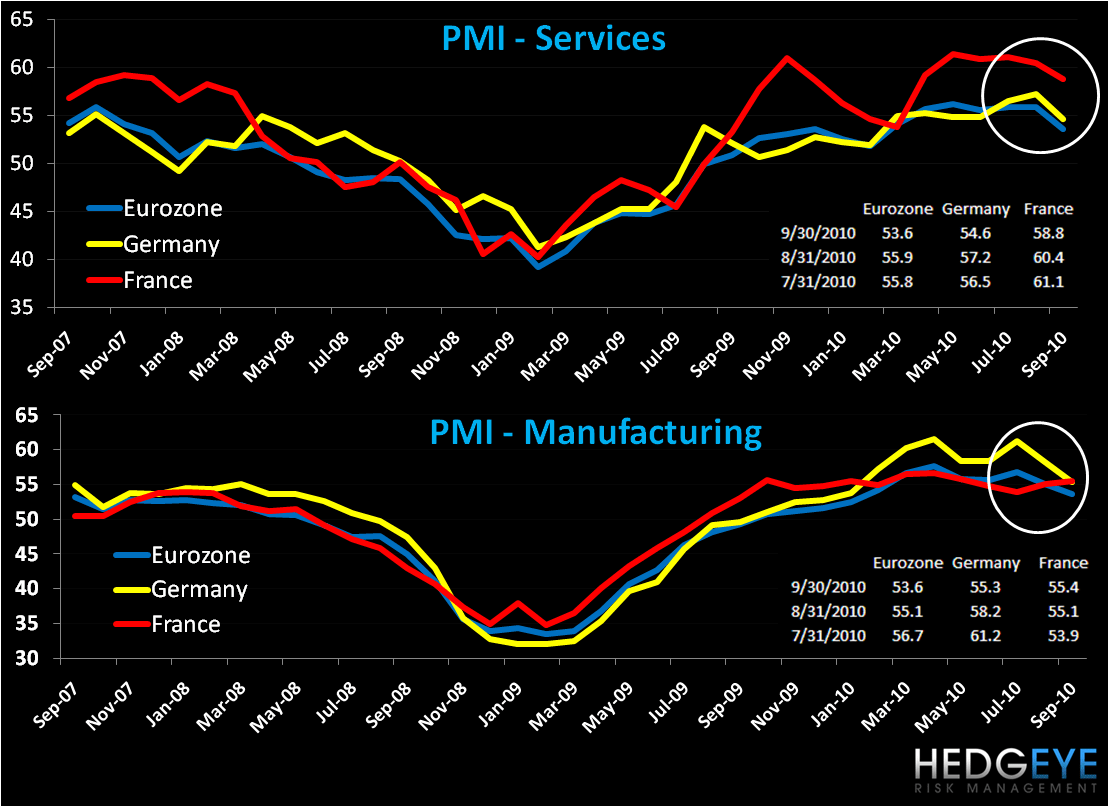

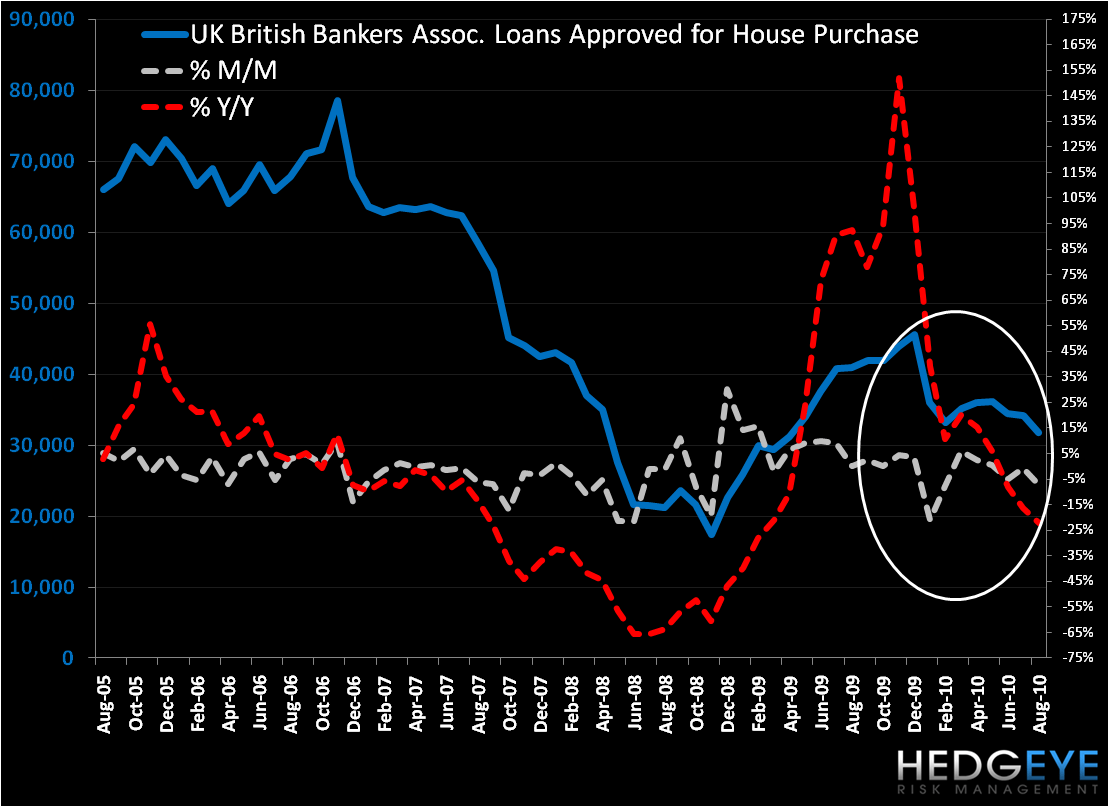

Position: Eurozone, Germany and France Services and Manufacturing PMI numbers decline in September; UK housing loan data continues to wane; and risk heightens across the region, in particular vis-à-vis rising CDS spreads in Portugal and Ireland above the critical 400bp line (see charts below). Today’s data is in line with our call for a material downward inflection in fundamental European data across most of Europe beginning in August and continuing over the intermediate term TREND.

We’re however not bearish on Europe outright. As we noted in a recent post titled “The EU’s Guiding Hand”, we’re currently bullish on Germany, with the DAX outperforming many of the equity markets of its Western European peers, and bullish on the GBP and EUR versus the USD on a relative basis, as we see substantial downside in the USD and YEN, in particular. Our bullish intermediate term TREND line for the DAX is 6089; our TREND lines for the Euro and Pound are $1.26 and $1.52, respectively.

Below is a short discussion of today’s charts:

1. We expect Eurozone Services and Manufacturing PMI to continue to wane over the intermediate term TREND as austerity measures across the region squeeze the consumer and dampen the economic outlook out on the curve.

2. The UK housing market remains a critical fundamental headwind (like in the US) that we think will continue to drag down growth prospects in the UK. According to the British Bankers Association, loan approval for house purchase declined -7.2% M/M and fell -22.3% Y/Y. Noteworthy is that year-over-year comps will get increasingly difficult up to a loan approval peak in Dec. ’09.

3. As an important leading indicator, the risk trade in Portugal and Ireland is breaking out vis-à-vis CDS spreads, in particular. As we noted in late ’09 and 1H10 in relation to Greece, and as history has shown in relations to the CDS spreads of Lehman Brothers and Bear Stearns, the 400bp line is a critical inflection line (Shark Line) to watch as the probably of upside risk heightens materially as you move through the line.

Matthew Hedrick

Analyst