This guest commentary was written by Benn Steil, Director of International Economics at the Council on Foreign Relations. This post originally appeared here on the Council of Foreign Relations' Geo-Graphics economics blog on February 16, 2021.

|

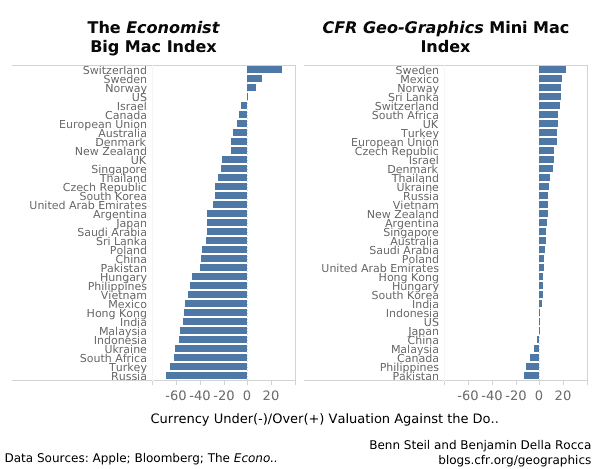

The “law of one price” holds that identical goods should trade for the same price in an efficient market. But how well does it actually hold internationally? The Economist magazine’s Big Mac Index uses the price of McDonald’s Big Macs around the world, expressed in a common currency (U.S. dollars), to measure the extent to which various currencies are over- or under-valued. The Big Mac is a global product, identical across borders, which makes it an interesting one for this purpose. |

But the law of one price assumes there are no restrictions on, or costs involved in, the movement of goods, and Big Macs travel badly. So in 2013 we created our own Mini Mac Index, which compares the price of iPad minis across countries. Minis are a global product that, unlike Big Macs, can move quickly and cheaply around the world. As explained in the video here, this helps equalize prices.

And as shown in the graphic above, the Mini Mac Index suggests that the law of one price holds far better than does the Big Mac Index.

|

Over the past year, the dollar has fallen by eleven percent against the world’s second-leading currency, the euro. Measured by Minis, the dollar’s valuation has also fallen steeply—from a 1.8 percent undervaluation, to a 6.7 percent one. The euro, which has attracted investors with newly issued EU common bonds, has, on the flip side, soared from roughly fair value to a 14.9 percent overvaluation. |

The biggest factor in the dollar’s fall has been the Fed’s unprecedented monetary easing.

Since last February, just before the coronavirus triggered an economic crisis, the Fed has slashed short-term rates nearly to zero and pumped over $3.2 trillion into U.S. bond markets.

In consequence, the ten-year Treasury rate, which ended 2019 at 1.9 percent, stayed below one percent for the last nine months of 2020.

These historically low rates discouraged investors from parking funds in the United States.

With U.S. rates plunging, many developed nations with more stable rates have seen their currencies soar on the Mini Mac Index.

|

Australia, whose ten-year rates have mostly held steady since 2019, saw its currency jump from a 7.7 percent undervaluation to a 5.9 percent overvaluation. The economic crisis also sent investors running to the Swiss franc, a typical safe-haven currency, which swung from an 8.6 percent undervaluation to a 17.1 percent overvaluation. The Japanese yen, another traditional safe-haven currency, rose from a 4.3 undervaluation to a 0.6 percent undervaluation. |

And what does the Big Mac Index say? Well, perversely, it shows the dollar now overvalued by 31.1 percent—a Whopper.

So who ya gonna trust?

EDITOR'S NOTE

Benn Steil is Senior Fellow and Director of International Economics, as well as the Official Historian in Residence, at the Council on Foreign Relations in New York. He is also the founding editor of International Finance, a scholarly economics journal; lead writer of the Council’s Geo-Graphics economics blog; and creator of six web-based interactives tracking Global Monetary Policy, Global Imbalances, Sovereign Risk, Central Bank Currency Swaps, China’s Belt and Road Initiative, and Global Growth. Prior to his joining the Council in 1999, he was director of the International Economics Programme at the Royal Institute of International Affairs in London. He came to the Institute in 1992 from a Lloyd’s of London Tercentenary Research Fellowship at Nuffield College, Oxford, where he received his MPhil and DPhil (PhD) in economics. He also holds a BSc in economics summa cum laude from the Wharton School of the University of Pennsylvania. This piece does not necessarily reflect the opinion of Hedgeye.