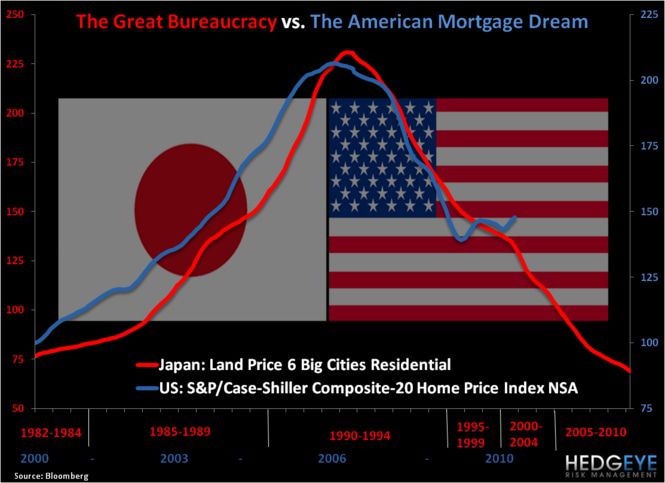

While the United States of America in 2010 may not “precisely” be Japan of 1997, there are plenty of similarities developing in terms of Big Bureaucratic Government resolve. If you have any recovering friends from Groupthink Inc who make it past the remedial exercise above, please send them our Chart of The Day that overlays the Japanese real estate bubble with ours. *Note the duration.

This chart was extracted from our EARLY LOOK note, available to RISK MANAGER and INVESTOR subscribers in real-time, at 8am ET every morning. The Early Look is unlocked at 4pm ET for non-subscribers. To gain access the note in its entirety, please subscribe or sign-up for a free-trial.