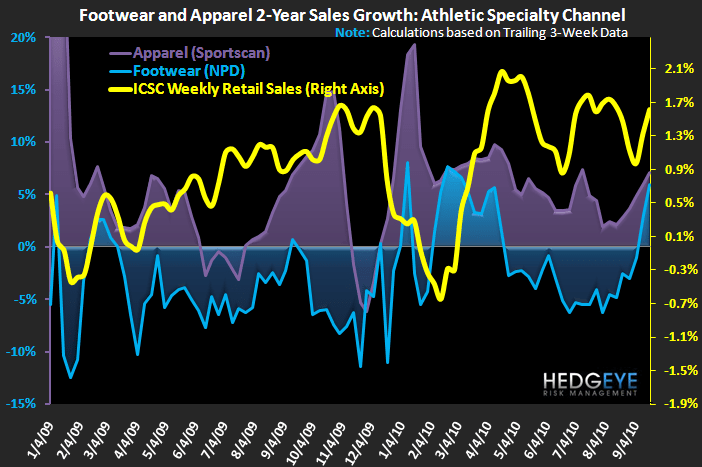

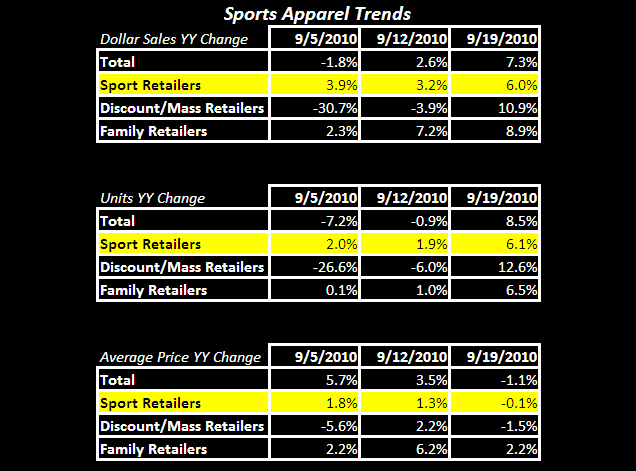

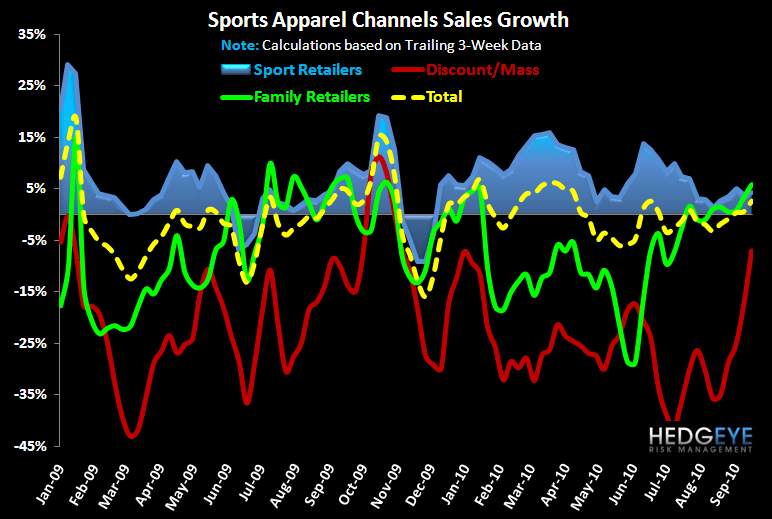

As a follow up to last week’s athletic trend update, sales accelerated again this week a trailing 3-week basis in athletic footwear and apparel as well as at retail according to ICSC weekly retail sales. Perhaps most noteworthy is the growth in athletic footwear up +8.3% on a trailing 3-week basis despite facing materially more difficult compares (+3.7%). Importantly, this growth came on higher ASPs suggesting new product flow is starting to gain traction. Recall that next week marks the last tough comp (+4.8%) before footwear has the wind at its back with considerably more favorable compares over the next 2-months until holiday sales in December. In addition, all three channels were strong with discount/mass going positive for the first time in nearly a year. As a result, we expect the athletic space and athletic footwear in particular to outpace overall retail and continue to be a preferred subsector within retail.

Casey Flavin

Director