|

Editor's Note: Below is a complimentary excerpt from a recent institutional research note written on by our Gaming, Lodging, and Leisure (GLL) analyst Todd Jordan. If you are an institutional investor interested in accessing our research email sales@hedgeye.com |

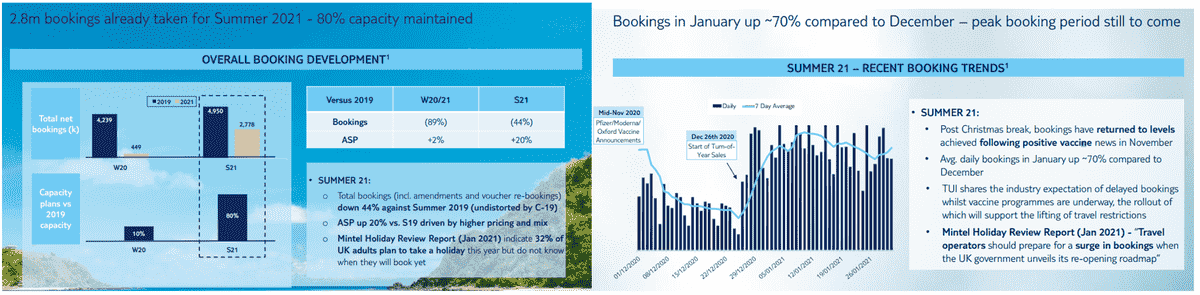

European travel agency / tour operator TUI Group released year end results yesterday and also highlighted current trading activity for the YTD.

TUI presented an entire deck, but we zoned in on the two slides below as it could provide some context for how European leisure demand is shaping up for Q2/Q3 - an important read through for the OTAs, Booking Holdings Inc. (BKNG) and Expedia (EXPE) in particular.

Just a few weeks after the Pfizer and Moderna news broke, TUI began to see bookings pick up for their summer season and that pace has maintained since the start of the year, despite a relatively worse Covid situation in Europe.

New bookings in January accelerated 70% MoM vs December for the summer program.

Still, bookings are down 44% vs ’19, but the ASPs are actually 20% higher due to mix and timing, but also due to strategy it seems. We think similar data is trending much more favorably in the US, but for the EU, that -44% number seems a bit better than our indications have been from other 3rd party data, which we discussed in yesterday’s OTA preview (HERE).

With an improving Covid situation, accelerated macro growth, and disposable “cash on the sidelines” for many consumers, we’d expect TUI’s and others bookings will look a lot stronger in a few months.

Specifically for BKNG, who dominates across the EU, we think the readthrough is a relatively positive one because they’re likely to materially outperform TUI’s growth rate given the breadth of unique inventory they offer, but also their ability to market efficiently and stimulate more bookings as they see demand creeping back into the system.

For context, we’re modeling BKNG Q2/Q3 Room Nights down 15% vs ’19 vs the Street which is modeling Room Nights -26% vs ’19.

We expect the Street to migrate higher towards our numbers in the coming months as travel data hooks higher. BKNG remains on our Best Ideas as a long.