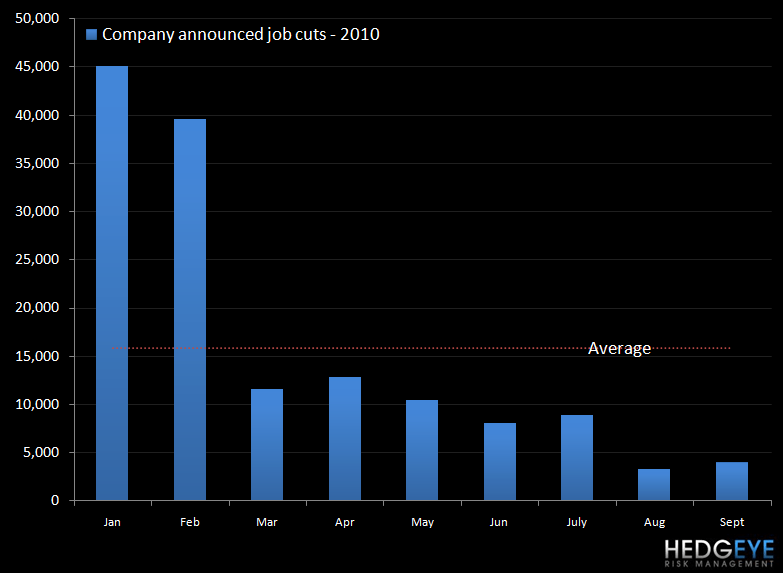

Conclusion: The number of job cuts in North America is accelerating after seven months of declines.

We are headed into a critical time for corporate America. As of the close last night, the S&P 500 was up 8.88% month-to-date, the best September performance since the 1930’s, as the MACRO data points are not getting any worse - for now.

Despite the market rallying on improved expectations, we are seeing the number of companies announcing layoffs begin to accelerate. So far, the number of layoff announcements in September 2010 is above the total number for all of August.

While the absolute numbers are modest compared to what we saw in 2008 and 2009, the MACRO backdrop suggests that the number of layoffs will accelerate from here.

So far in September, Philip Morris, Fed Ex, Genzyme, Merck and Boeing have announces layoffs. The interesting stand out is FedEx which announced it is laying off 1,700 people versus 1,000 in April 2009.

In the 2Q earnings season, 32% of the companies in the S&P 500 missed on the revenue line, while only 17% missed on the bottom line. With GDP declining sequentially and bonuses on the line for making “the numbers”, I fully expect to see more corporate restructuring and layoffs in the coming months.

To a certain extent, the pattern of layoffs is seasonal, as management teams plan for the next fiscal year and we are headed into the budget season. In a slowing economy and a difficult consumer environment, trying to anticipate revenue growth is very difficult. A real-time example of this is CAG. The company said today, “Promotional programs did not drive increased consumer purchases to the extent expected, reflecting the prolonged economic challenges consumers have faced and the difficult retail environment.”

We know from the labor department that, despite 3.7% and 1.6% GDP growth in the first two quarters of 2010, the economy did not add any jobs. With GDP growth likely to slow in 2H10, corporate cost cutting will take center stage in the coming months. The easiest way to cut costs is to cut employees, as we have seen over the past two years. Complicating the process in 2011 will be inflation. Despite what Ben Bernanke says, there is real inflation in the U.S. today. Again, just look to CAG’s results today, the price of gold, the price of foodstuffs or a number of other asset prices.

Given current trends, we calculate that between 160 and 200 companies in the S&P 500 are faced with a challenged revenue environment. The bulk of the companies that are feeling the pain are in the Financials and Consumer Discretionary sectors.

Howard Penney

Managing Director