One year expensing of capital purchases could be a boon to slot suppliers.

Casinos are about to get a new incentive to upgrade their slot floors. HR 5297 would allow accelerated depreciation of new equipment for tax purposes, although not at the 100% proposed by President Obama last week. Still, for slot floors that are aging fast and nearly fully depreciated, this bill could be the tonic to expedite that inevitable acceleration of replacement demand.

According to the Internal Revenue Code of 1986, slots are depreciated under a 7-year recovery period, though there is a pending proposal (HR 5465) to change the recovery period to 5 years.

On Sept 8, 2010, President Obama proposed increasing the bonus depreciation policy to 100% for 2011. The policy will allow firms for the first time to apply an immediate, full write off of the cost of new equipment purchased between Sept 8, 2010 and Dec 31, 2011. Expensing legislation has been enacted in the recent past. In 2002, Congress passed a 30% bonus depreciation allowance through the Job Creation and Worker Assistance Act of 2002. A year later, it raised the limit to 50% through the Jobs and Growth Tax Relief Reconciliation Act of 2003 for investments made before January 1, 2005. The Economic Stimulus Act of 2008 and the American Recovery and Reinvestment Act of 2009 both renewed the 50% rule but that expired on 12/31/09.

The Small Business Jobs Act (HR 5297), which was passed in the Senate today, will allow firms to retroactively apply the 50% rule for equipment purchased before Sept 8, 2010. HR 5297 will also increase Section 179’s depreciation limit from $250k to $500k for 2010 and 2011—Section 179 is a provision allowing taxpayers to expense 100% of certain types of acquired assets. Now, HR 5297 returns to the House for approval before being passed to Obama for his signature.

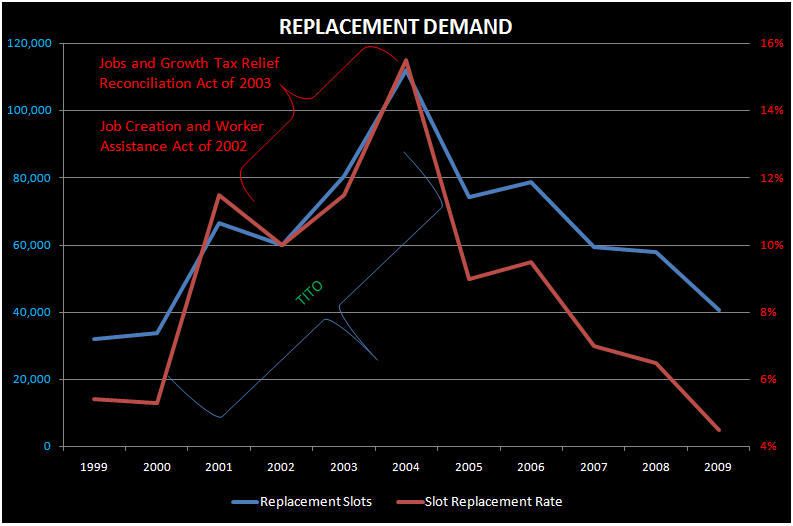

Let’s look at history. As the following chart shows, the enactment of accelerated depreciation during 2002-2004 coincided with a big jump in replacement demand. Of course, that was also in the middle of the Ticket In/Ticket Out (TITO) technology implementation so it is difficult to determine the direct impact. What we do know is that for tax purposes, the current slot floors are pretty close to being fully depreciated. Slots purchased pre-2004 will be fully depreciated by the end of the year. Very little remains of the 2004 slots due to the accelerated depreciation in that year. The 2005-2007 slots are still being depreciated over a 7 year life. Due to 50% expensing, the 2008-2010 classes of slots have low tax basis.

We are not ruling out 100% expensing either. The President wants it; it is politically feasible; and it could garner bipartisan support. Accelerated depreciation alone is probably not enough to create a big replacement cycle but it could spark one. The long-term dynamics are in place, however, which is why we are excited about the prospect of a spark. Here are the reasons why replacement acceleration could be fast and big:

1. Floors are not old yet but they will be soon – end of TITO was 6 years ago

2. Operator balance sheets are in much better shape

3. More certainty in the casino business – revenues are stagnant but at least the world isn’t ending

4. More competition from new markets