CRI: One of the Worst Stories in Retail

I tried to think of a clever title. But with CRI there’s really no more appropriate way to tee up the story. This company is over-earning by 400bps in margin.

Let’s be clear about something. The Carter’s brand is dominant, and the core business is extremely defendable. Everyone reading this who has a child under the age of 2 probably has Carter’s layettes, onesies and booties all over the place. Our point in this note is not that the business is a fade, but simply that the sustainability of the current revenue trajectory at a 13% margin is an absolute pipe-dream. Our model is at $1.87 in FY11 – the consensus is $2.51. Our confidence in this number is high. Timing and sizing of the position will depend on Mr. Market. Keith shorted CRI in the Hedgeye Virtual Portfolio yesterday. Game on…

Macro Chimes-In: Before we lay out the research behind why margins need to come down, here’s Keith McCullough’s view on CRI from a Trading/PM perspective.

“CRI is bullish immediate term TRADE and bearish intermediate term TREND /long term TAIL. Immediate term bullish is what I call a short selling opportunity. The long term TAIL line of resistance for this stock is where it collapsed from this summer = $27.91; use that as your stop. From an intermediate term TREND perspective, there is a wall of resistance at the $26.68 line and I’d short it all the way up to that level, averaging in. Immediate term TRADE support is $23.69, and a breakdown/close below that line will put lower all-time lows in play.”

THE CASE AGAINST CRI’s MARGINS

As we usually do, let’s start off here with some historical context. It’s vital to the call.

Nov ’03: Carter’s goes public. The ‘pitch’ crafted by the bankers at Morgan Stanley was that the company was reaccelerating growth around its core baby business to playwear, mass channels, and company retail. This was being facilitated and funded by a deeper sourcing relationship with Li&Fung.

May ’05: Carters buys Osh Kosh for a staggering 312mm. As a frame of reference, that’s 10.8x TODAY’s EBIT. It’s old hat that this deal was a complete failure. But the context matters.

You gotta hand it to the MS Bankers. Their pitch at the time was spot on. That’s probably why the stock ended up being a 3-bagger in 2-years.

But there was one very big problem brewing beneath the surface. Simply put, the company was morphing its business model from that of a stable and predictable packaged goods company, to one that is more fashion related.

C’mon McGough…Isn’t it a stretch to call Carter’s fashion??? The answer is No. The core wholesale baby (onesies, blankets, etc…) used to account for 75% of cash flow. Now it is closer to a third. The stone cold reality is that the Playwear business competes with Old Navy, Children’s Place and Gymboree. The retail segment is a completely different ball game, has extraordinarily low visibility, and added significant volatility to internal forecast accuracy. The mass business can be a great asset, as the Target partnership has proven to be. But Wal*Mart woke up one day in 2009 and decided to shrink Carter’s. Not good for a company that’s never had to deal with key customer risk.

This all adds up to a business that has changed so much at the front-end as it relates to product and customer mix. That’d be great, but unfortunately the back-end of this company still looks and functions like a packaged goods business.

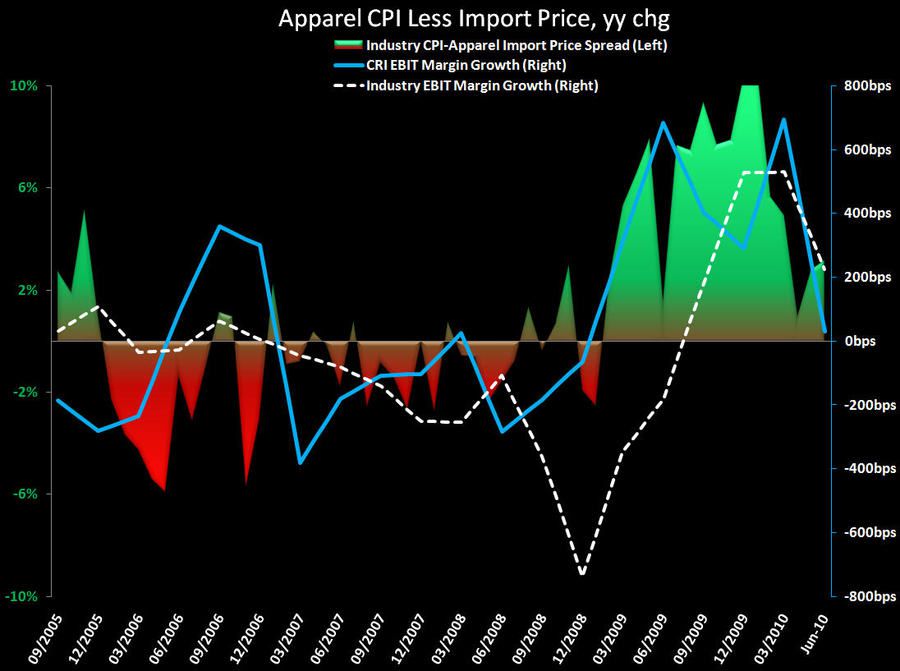

That’s why it was so amazing to see the business deteriorate from ’06-’08, and yet margins still never moved more than 100bp off of 10%. The reason is that CRI cut infrastructure – almost entirely on the creative side of the business – to keep margins and EPS high. An example is that when CRI bought Osh Kosh it had over 400 employees, and by the time of the management shake-up the Osh Kosh employee count was well below 200. Philosophically, I don’t see how any consumer business can reaccelerate growth by cutting heads by 50%.

The punchline is that this is what led to the shake-up in top brass in the summer of 2008. I was a big fan for all the above reasons, and specifically noted at the time that a guy like Mike Casey (then CFO) would ‘get it’ that margins needed to come down due to infrastructure investment before they could go back up to a level that would sustain profitable top-line growth. But I could not have been more wrong. Over the past 2-years margins have come up by a full 500bp. This is the same time over which the spread between consumer prices for apparel and input costs widened to 3-standard deviations above the mean – implying about $10bn of profit was freed up in the supply chain of an industry that’s only $280bn in size.

That brings us to today… What do we know? We know that we’re in a margin bubble, and in YouTubing management, synching with changes on the margin in the Macro and Retail landscape, and applying some analytical muscle – it paints a story where margins appear to have meaningful downside.

1) There has been a disproportionate shift in talent in Carter’s from product/merchandising towards finance and accounting. Is it bad to have better accounting? NO!!! But it needs to be additive to headcount, not replacement for creative talent. This is one reason why margins popped like they did over 2-years. A nice bonus, but not sustainable.

2) During this period, Carter’s had its little run-in with Kohl’s over accounting for markdowns – something that did not make KSS happy in the least. It also ran out of steam with Wal*Mart and subsequently had a 25% decline in WMT revenue. We’re seeing a pick-up at WMT this year per CRI. But with WMT completely uprooting apparel merchandising organization, this business is hardly a lock. The bottom line is that a question mark behind WMT and KSS is not something I want to see when I’m incrementally concerned about product.

3) Here’s management’s comment on cost inputs as of the conference call in July vs. our take (in bold).

-

-

CRI: “The cotton cycle has typically run some portion of a year. Nothing cures high prices like better-than-high prices, so as prices are up, people plant more cotton and the prices will come down. So cotton and freight will settle down in the next year or so.”

Hedgeye Retail: Since this statement – by far and away the largest component of COGS at CRI – is up 19% sequentially. That’s 56% year on year, 56% year on year, 56% year on year. Get the point? The company is planning for 10%. -

CRI: Higher labor rates will continue with us. Li & Fung says to expect higher labor rates to continue as there will be an inflationary cycle in the foreseeable future.

Hedgeye Retail: This is the second-highest input cost.

-

4) Pricing/Promotional Considerations

a. CRI On prices: “So going into spring ‘11 where products costs have gone up, 10%, we’ve raised prices in both wholesale and retail, I would say selectively. We’ve raised in where we thought unit velocity wouldn’t be significantly impacted and that’s a balance. We could take prices up on everything tomorrow, but if you take that spread beyond what makes sense relative to private label, you’ll start to lose unit velocity. So we’re trying to find the right balance between what price would the consumer be willing to pay, what continues to drive very strong top line growth because growth – sales growth solves a lot of issues.”

Hedgeye Retail: We know that this company needs pricing power to keep margins high. The price/cost gap has turned meaningfully against CRI over the past 3 weeks.

b. Promotional Flexibility: CRI: 50% of business is in retail, so [we have] plenty of flexibility. Typically the day new product hits the floor in owned stores its 40% off, only when the product is selling really well will they moderate the level of promotion to 25%-30% off. If traffic is better, product performance is better, if traffic is weak, it’s easy to get promotional.

Hedgeye Retail: 40% off on day 1! Does this sound like a business with pricing power? And this represents 50% of CRI’s business.

c. Long-term Cost Cycle: CRI: “Li & Fung has said publicly, listen, we’re probably going to be in an inflationary cycle whereas over the past 10 years it’s been a deflationary cycle, on product costs, probably going to be in an inflationary cycle. People got to have to figure out how to get paid more because we’re all public companies, we are not interested in lower margin, business isn’t making less money. So it’s going to – the consumer ultimately is going to have to pay a bit more for the product that they’re buying. Yeah, so I think it has more of an inflationary issue than it’s what Target and Wal-Mart are doing.”

Hedgeye Retail: JC Penney and Kohl’s are also out recently saying that inflation will be good for the apparel industry. It seems like everyone is banking on all of us paying higher prices. SO let me ask you this…with a 56% boost in the primary cost input, you’re looking at paying $11.50 on a layette that would otherwise cost $10. Not a chance…

d. CRI on what we’ll refer to as Anniversarying a Temporary Pricing Bubble: “Everybody was running very lean over the past 12 to 18 months. [Are people shifting] to be more aggressive with building inventories? I hope not, because when they were running lean, they were running out of goods, calling us to say hey, we’re too light on inventories. Can you ship the – that third delivery earlier? Can you get us some things? What do you have? Can you dip into the safety stock levels and get us product earlier. And for us, it was a beautiful thing. We had a strong consumer pull model and the sales were better, margins were better.”

Hedgeye Retail: Kind of ironic that this happened during the period when the new management team was put in place and margins went up 500bp.

e. On Private Label: CRI: “We’re most conscious on the spread between Carter’s and Osh Kosh brands vs. private label. Private label is primary competitor and as long as management keeps the price $1 to $2 above private label, consumers will pay the premium for the branded product.”

Hedgeye Retail: Again, pricing for this company will be based on the least common denominator in the competitive landscape. CRI is not planning for this. Nor are the retailers. Who in their right mind would step up now on a conference call and say ‘we’re preparing for a price war with our competitors’ or ‘we’re going to break rank with retailers and breach price integrity’?

The bottom line is that we’re just coming off a 2-year period where margins skyrocketed by 500bps despite no change in the trajectory of revenue. Input costs and supply chain dynamics worked in CRI’s favor, as did an accounting-led management team. Along the way product has suffered relative to strengthening competition, relationships with key retail partners became strained, and input costs have done nothing but go up. The level of price increase that we as consumers need to pay without department stores or Li&Fung picking up the tab in order for CRI to protect margin is something they’ve never seen – ever. The sell-side has adopted an extend-the-trend model here and has the company reaching margin levels in 2011 that are above Nike, Ralph Lauren, Under Armour, Columbia, and a host of others who have something called sustainable top line growth. We’ve got high conviction that this is a blow-up waiting to happen.

Where could we be wrong?

-

CRI is seeing a rebound in its Wal*Mart business next year. They’re budgeting $125mm – which is up roughly $15mm vs. this year, and over $25mm in 2009. Even though there is new leadership in Wal*Mart’s merchandise org for apparel who has little brand loyalty, this is a good direction. If the brand performs and the desired price and margin, there’s no reason why it can’t head higher.

-

CRI brought in a new product leadership team at Osh Kosh earlier this year. They plan to strut their stuff for the Street at an analyst event in October. Wholesale orders are currently up about 10% at Osh Kosh – that’s about $10mm, or less than 1% incremental growth to the company.

-

Dot.com is an opportunity for CRI. They’re investing in this business and are likely to see an acceleration therein. Dot.com makes sense here. Think about it – you’re a new mom and you need a bunch of booties. Do you want to haul all the way to a Carter’s store? Probably not. That said, it makes more sense to us to leverage the dot.com model of a Baby’s-R-Us or Buy Buy Baby – where you’re likely doing one-stopping for the wee one beyond apparel.

-

Pricing: If the industry as a whole pushes higher pricing and no one breaks rank, then our numbers next year may be too low. It would be one of the first times in the modern history of the apparel retail industry that this happened. But it’s a risk we can’t ignore.

-

The 3Q print is the most challenging one from a top line perspective. Then the 4Q compare is quite easy before the margin story really starts to unwind. Whether CRI lets the margin story out of the bag with guidance in the 3Q call is questionable. We’re probably going to have to wait til 1Q for the big blow-up.

Where could the stock go?

If you think that our work is completely off-base and you believe that the company can earn $2.51 next year and continue to grow sales in the mid-single digits, EBIT at 10, and EPS in the teens, then be my guest and buy it at $25. But if I’m ultimately right on the model, then we’re looking at Under $1.90 in EPS. We can slap a 10x p/e on that, but the reality is that I’m looking for a severe event that will blow earnings credibility out of the water. At that time, I’m not so sure how many people will be so rational or fixed on price target methodology. If the event makes $1.87 apparent, then there will be times where the market will wonder – why not $1.25? Why not $0.50? That’s not what I’m calling for, mind you. But simply to use 10x $1.87 as a floor would be irresponsible from a risk management perspective. Realistically, this has $5-10 downside. As noted, Keith is likely to trade around this for a quarter or two based on his own risk management parameters. Stay tuned.