Hedgeye Portfolio Position: Long Germany (EWG); Long British Pound (FXB)

Where’s Europe at? Last week I was on vacation and had some time to think about how fear has run in and out of European markets over the last 18 months. Here’s a read-through regarding our top-down pulse on Europe.

Contagion Fears

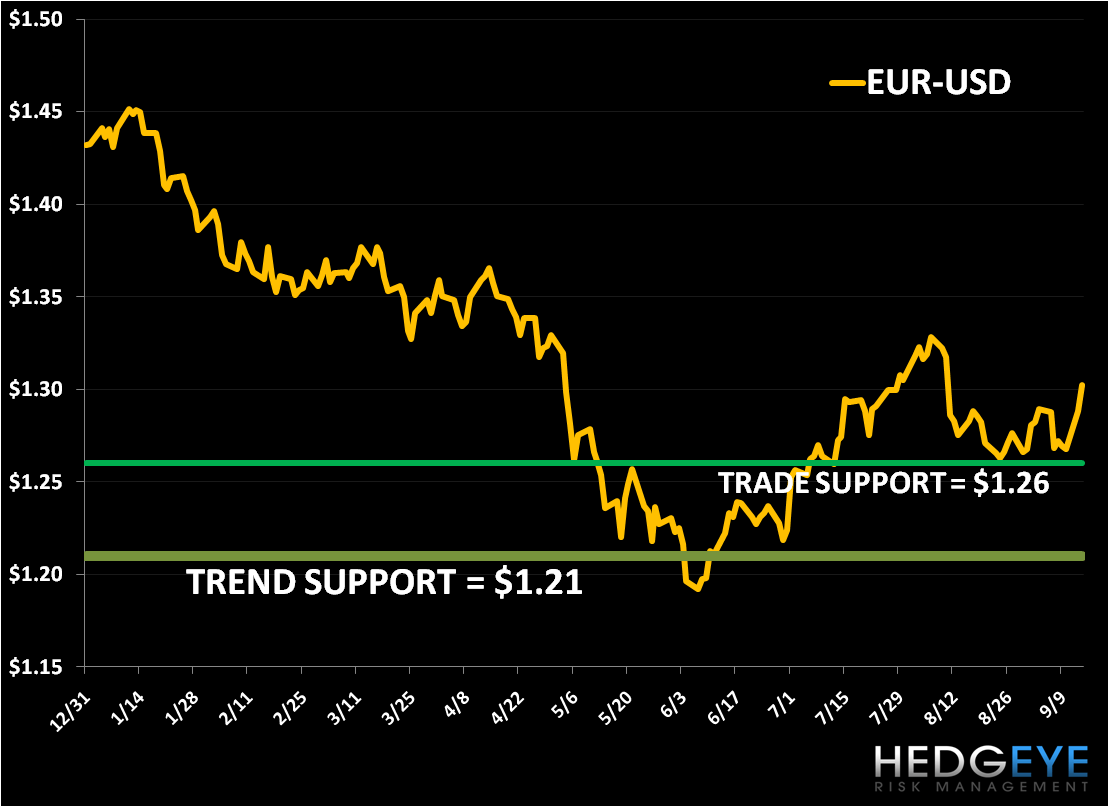

Despite the contagion fears and Europe “parity” callers that occupied front-page news in 1H10, the fear trade has settled down across most of the region to the benefit of the Euro. The EUR-USD has held its TREND line of support at $1.26 since 7/5.

Europe’s Baby

Our view is that Greece (and debt and deficit-laden countries like it) will remain the EU’s baby in the sense that European commissioners and heads of state will do everything in their power to prevent the immediate term failure (default) of member states for fear of the associated volatility (contagion).

Remember, leaders had a good taste of contagion fears in the first half of the year, which led to the decision on May 9th to issue a €750 Billion package of medicine to contain it. Politics are generally local, but recently the EU’s political scene has gone global.

Evidence refuting European Contagion over the immediate to intermediate term:

- Investor Protection: on Monday, Greece received its second tranche of funds, worth €6.5 Billion, and we expect future payments to go off without a hitch. Due to the highly interconnectedness of European debt across European banks, it’s in the interest of the EU to prevent default by any member state. In the case of Greece, our call is for the EU to continue to work in close cahoots with Greek PM Papandreou to show a good face to the investment community. Papandreou has promised to reduce the country’s budget deficit to 8.1% of GDP this year, versus 12.2% in 2009.

- Credible Buyers: Norway’s sovereign wealth fund (the 2nd largest in the world) decided to buy an undisclosed amount of Greek, Spanish, Italian and Portuguese debt late last week. This confirms that Norway is also betting that the EU will be feeding the PIIGS the bottle for quite some time. [Greece’s most recent sale of €1.17 Billion of 26-week bills commanded a hefty 4.82% yield with investors biding 4.5x the offering = confidence rising or yield chasing.]

- Idealism on the Line: the notion of a Eurozone member defaulting on its debt cuts to the core of the idea of the mutual benefit from a union of countries. Politicians in Brussels will take grave measures to insure the Eurozone remains whole. [Hedgeye note: we believe the utility of the Eurozone is still in question, and for good reasons. As we’ve noted in previous work, member countries are not created equal, and therefore we see a flaw in unilateral monetary policy for all; as ever, measures to manipulate currency and trade are very important in this global world.]

Austerity and Longer Term Structural Issues

While we’re bullish on countries cutting balance sheet and income statement ‘fat’ now in such forms as trimming spending, government jobs, and wages over the next 1-4 years, we expect more moderate growth in lock step with these fiscal cuts.

A couple of pressing issues over the longer term for the Eurozone are:

- What’s to be done if the Eurozone’s weaker nations continue to pile on debt, especially when they can’t compete for trade?

- Will the Eurozone’s fiscally weaker countries be able to bend on such cultural norms as the obligation to pay taxes, the duration of the work week, and creation of alternate job offerings as government positions are pared back?

To the second point, unemployment remains a huge structural issue on our long term TAIL duration. We see significant headwinds for countries like Spain, Ireland, and Greece where we don’t see their double-digit unemployment figures turning around materially in the next 1-2 years, which should hinder growth prospects out on the curve.

The chart below displays Greece’s equity market (left axis, down -28.9 YTD) versus Greek 5YR sovereign CDS (in bps) and the Greek 10YR bond spread over the German 10YR bund (in bps, right axis). What’s interesting to note here is that although we expect the EU to rescue Greece at all costs, which should boost equities and dampen yields and CDS, ‘fear’ since the EU’s bailout package in early May continues to heighten. Obviously this is a negative read-through, which we’ll continue to monitor for an inflection.

We’re currently long Germany via the etf EWG in our virtual portfolio, and bullish on the Pound versus the USD, a play we continue to like as UK inflation remains elevated (currently at 3.1% in August Y/Y) and US fiscal policy continues to be politically compromised.

Matthew Hedrick

Analyst