|

Editor's Note: Below is a complimentary excerpt from a recent institutional research note written on by our Gaming, Lodging, and Leisure (GLL) analyst Todd Jordan. If you are an institutional investor interested in accessing our research email sales@hedgeye.com |

Tripadvisor (TRIP) is not a name we often comment on, as we have often been more focused on the bigger cap names on the OTA side of online travel. But with the stock performing nicely so far this year, and actually outperforming its OTA and other travel peers, we wondered if there was something more in its story that we’re missing.

The stock has been ‘cheap’ for a while, but cheap with limited growth prospects doesn’t usually beget a higher multiple.

We have heard that the newer pitch on TRIP is that its formerly non-core business lines like restaurants and experiences will become a lot more core and inevitably drive the company’s future growth.

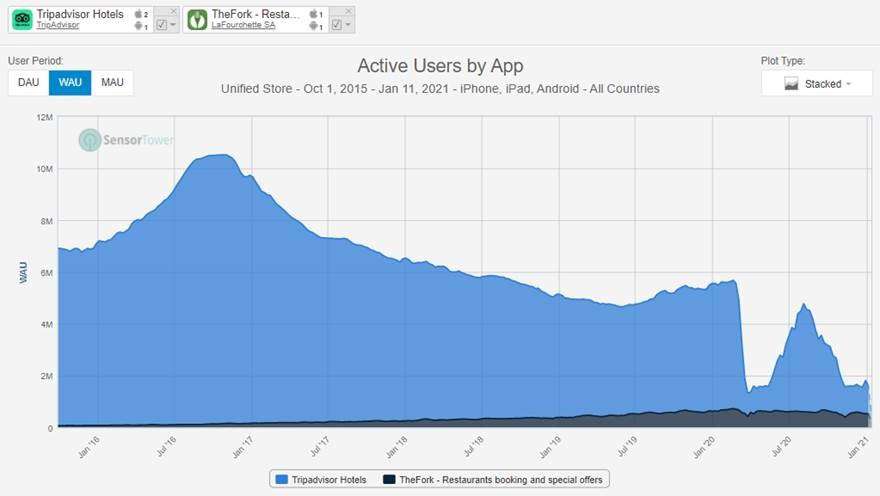

All the while, TRIP’s core hotel product and search should benefit from the reopening of the leisure travel industry – we see that opportunity more than the former.

But how about all the company issues pre-Covid?

A secular decline in users on mobile (see below), desktop, and a lot more risk from Google (due to poor SEO management) than for the OTAs, are a few of the issues. We’re not overly focused on TRIP right now, but we’re curious if there’s enough of a case to be made that the story is changing – we’re skeptical, but open minded on the topic.