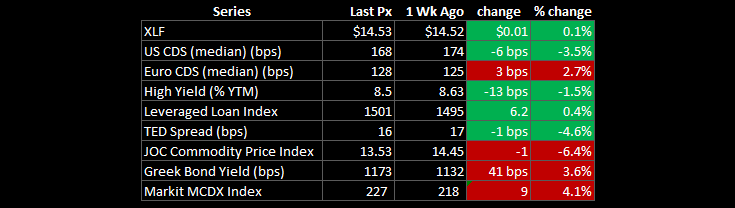

This week's Financials Risk Monitor is evenly split, with four metrics worsening week over week and four improving. European risk metrics (Greek bond spreads and European financials CDS) continue to flash warnings signs, while U.S. metrics are mostly flat to better. The Markit measure of municipal bond risk also showed increasing risk, as a potential default by Harrisburg, PA, looms this week.

Our risk monitor looks at the following metrics weekly:

1. CDS for all available US Financials (29 companies)

2. CDS for large European Financials (39 companies)

3. High Yield

4. Leveraged Loans

5. TED Spread

6. Journal of Commerce Commodity Price Index

7. Greek Bond Spreads

8. Markit MCDX

1. US Financials CDS Monitor – Swaps were positive across the board last week. Swaps tightened for all of the 29 reference entities. Conclusion: Positive.

Tightened the least vs last week: C, PGR, MBI

Tightened the most vs last week: JPM, LNC, HIG

Widened the most vs last month: SLM, AGO, MMC

Tightened the most vs last month: JPM, GS, UNM

2. European Financials CDS Monitor – In Europe, CDS was mixed. Swaps tightened for 11 of the 39 reference entities and widened for 28. Conclusion: Negative.

Widened the most vs last week: Banco Bilbao, DnB NOR, Credit Suisse

Tightened the most vs last week: Sberbank, Bakinter S.A., Banco Pastor

Widened the most vs last month: Bank of Ireland, DnB NOR, KBC Group N.V.

Tightened the most vs last month: Deutsche Bank, Alpha Bank, HSBC

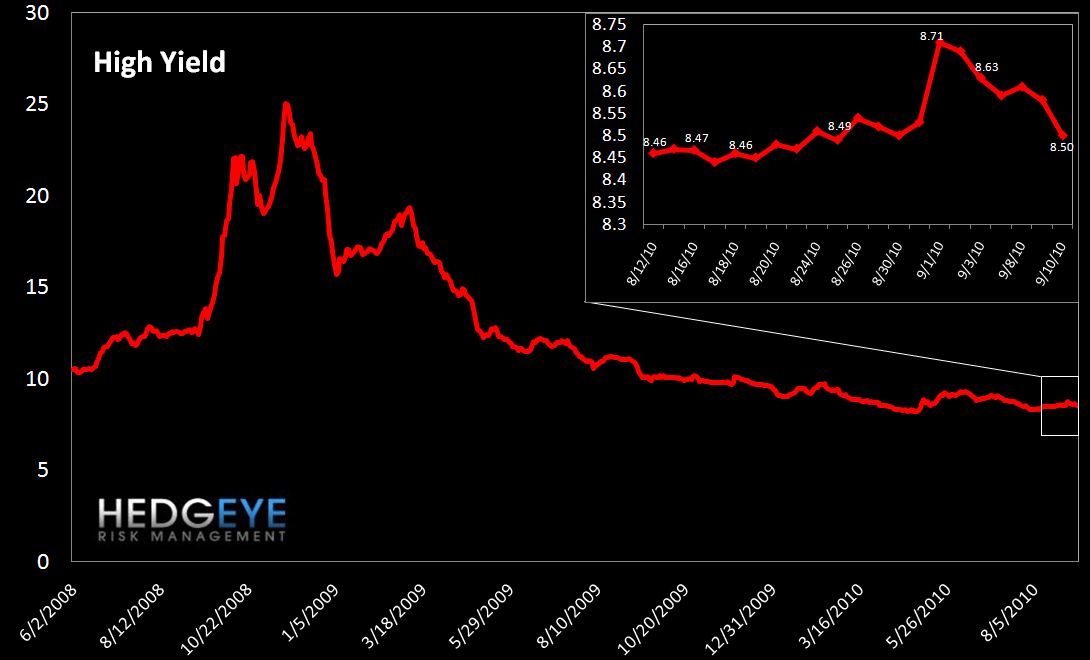

3. High Yield (YTM) Monitor – High Yield rates fell 13 bps last week. Conclusion: Positive.

4. Leveraged Loan Index Monitor – The leveraged loan index rose 6 points last week. Conclusion: Positive.

5. TED Spread Monitor – Last week the TED spread fell slightly, coming down by less than one basis point. Conclusion: Positive.

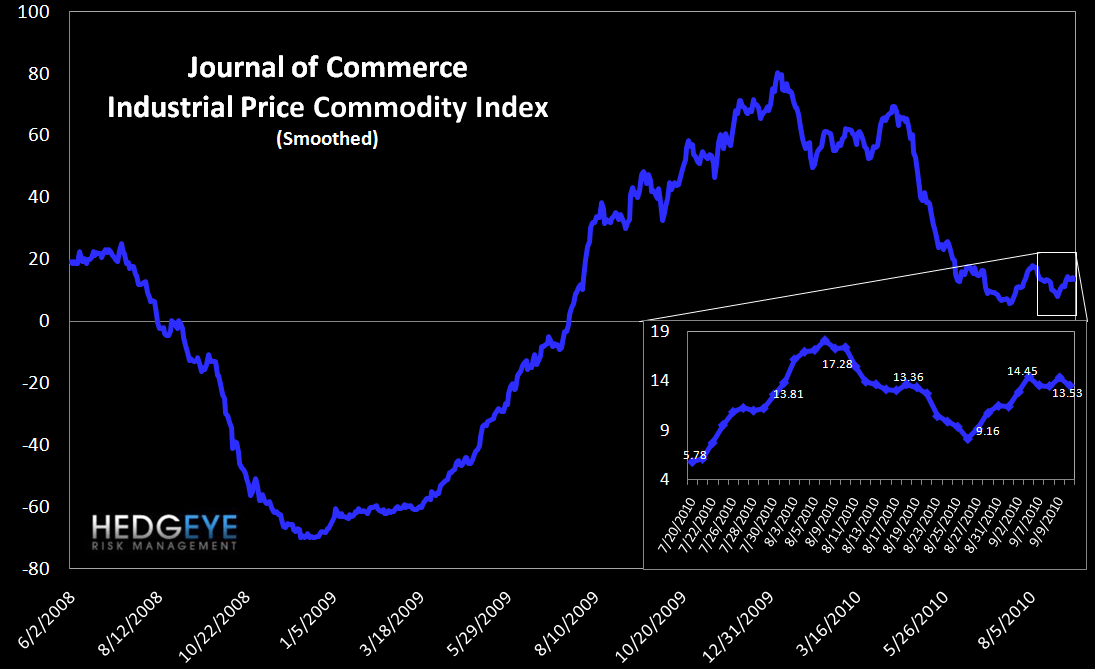

6. Journal of Commerce Commodity Price Index – Last week, the index fell just under 1 point, closing at 13.53. Conclusion: Negative.

7. Greek Bond Yields Monitor – We chart the 10-year yield on Greek bonds. Last week yields rose 41 bps, ending the week at 1173 bps versus 1132 bps the prior week. Conclusion: Negative.

8. Markit MCDX Index Monitor – The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on four 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. Our index is the average of their four indices. Spreads rose last week, closing at 227 versus 218 the prior week. Conclusion: Negative.

Joshua Steiner, CFA

Allison Kaptur