This note was orinigally published at 3:02pm ET for Risk Manager Subscribers. To receive Macro Select Content, and our Virtual Portfolio positions in real-time, please sign-up for a 14-day free trial or as a RISK MANAGER subscriber.

__________________________________________

Position Changes Today: Covered SPY, Bought EWG

I attempted to explain this today in my EL titled “Feeling Strange”, but I think it’s worth repeating. Duration Mismatch crushes performance and the best way to avoid it is having a Duration Agnostic risk management process.

As a reminder, we have 3 core durations that we manage risk around: TRADE, TREND, and TAIL.

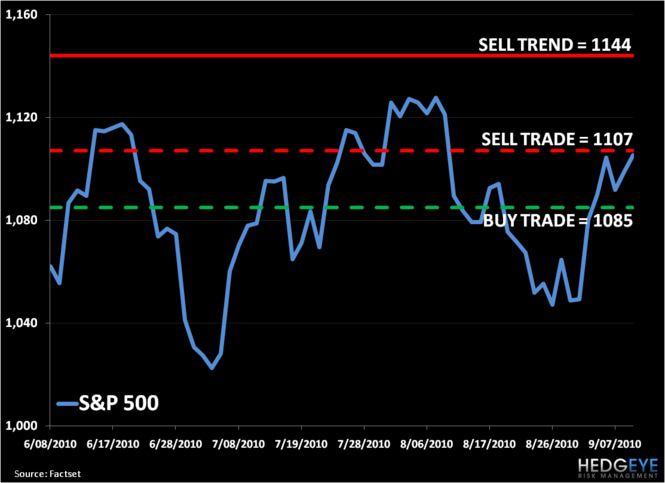

Currently, the SP500 is bullish from an immediate term TRADE perspective (support = 1085) and bearish from an intermediate term TREND perspective (resistance = 1144). That means that we can be mentally malleable enough to admit that the immediate term upside in the SP500 is more probable than the immediate term downside. Be sure not to confuse this with pretending you are going to be the next Buffett – keep a bullish TRADE a trade.

Both the DATA (ABC confidence, MBA mortgage apps and jobless claims) and the SP500’s PRICE support this immediate term bullish view. You might say, heh last week you shorted the SPY and how can you change your mind that quickly? Well, for starters, I didn’t have this week’s DATA or PRICES in my back pocket when I made that move earlier last week. The key to risk management isn’t being wed to a view that was based on prior DATA and PRICES.

If next week’s DATA turns back to bearish and the SP500 breaks 1085 again, I’ll short SPY again. As is customary, all my moves are on the tape – I have done nothing but cover and buy positions in the Hedgeye Portfolio since 11:02AM on September 3rd.

If the SP500 closes above our immediate term resistance line of 1107, I see heightened probability of this pain trade taking us all the way back up to another lower-high of 1123. And from a bearish intermediate term TREND perspective, nothing will have changed other than immediate term DATA and PRICES.

Stay transparent my friends,

KM

Keith R. McCullough

Chief Executive Officer