Overview

On December 22nd, 2020, we hosted a discussion and Q&A featuring Ryan Schmid (RS) & Jeffrey Hogan (JH), moderated by Hedgeye Health Care sector head Tom Tobin. Ryan is the Co-founder, President & CEO of Vera Whole Health; and Jeff is the Northeast Regional Manager for Rogers Benefit Group and Founder of Upside Health Advisors. Two things are clear: 1) the traditional primary care practice/provider (PCP) model is facing disruption and increasing pressure from multiple angles, and 2) employers are keenly aware of new options and are looking to shift toward value-based and/or at-risk contracts ASAP.

Billions-of-dollars have been spent over the years on fee-for-service (FFS) models/workflows, so change isn't going to be easy; however, Ryan put it plainly when asked about when we'll reach an inflection point: "The train has left the station... we'll probably see some big announcements" in the New Year.

A few takeaways:

- Newer entrants like Firefly Health and Dispatch Health are disrupting the market - not only existing provider groups regarding FFS arrangements, but by inspiring payers to say, “We must have this as part of a value-based solution on a go-forward basis.”

- We think hybrid models can offer employers and employees/members savings and a better experience, respectively, which is bullish for $ONEM.

- While change is clearly coming at the request of [large] employers, it's going to be slow due to entrenched workflows; Teladoc and Livongo ($TDOC), among others, should be able to maintain growth in the New Year, especially if BetterHelp continues its growth trajectory and Livongo is willing to enter into value-based arrangements and can execute.

|

Health Care Speaker Call | The Evolution of Primary Care & Employer Sponsored Benefits Healthcare Subscribers: CLICK HERE for event details (includes video and materials access) |

Summary Call Notes

Background Info

JH: Looking at the healthcare marketplace since March, I’ve never seen so much change in such a short period. At the end of March, much of it shut down but not for COVID-related payments. People were hiding out so as not to be exposed to the virus. We saw provider groups shut down as well, and many receive reimbursement from FFS. That volume fell off dramatically and exposed the immediate fragility of the system.

- With members/patients hiding out or lacking access to care, providers tried to stand up telehealth solutions quickly (some good, some bad, some indifferent). Speaking to doctors, the issues were many including payers trying to figure out reimbursement and no access to patient history, EMR/EHR records, etc. Many are still trying to figure it out.

- What happened/inspired the things we’ll talk about (hybridized or Advanced Primary Care (APC))? The need for interoperable and longitudinal care and coverage. People were/are afraid and don’t trust the existing commercial or public healthcare infrastructure (or politicians).

- The system failed them, creating a huge opportunity for innovators/disruptors.

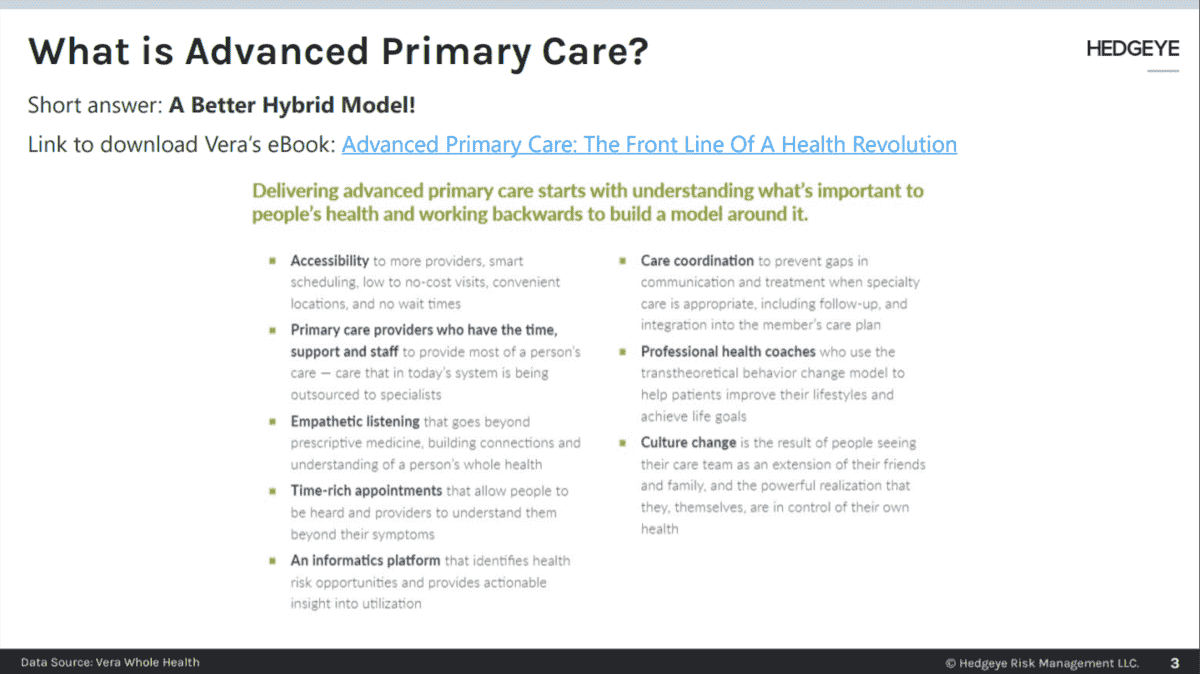

RS: Vera is an APC provider – mostly commercial but w/ some Medicare Advantage and individual business as well. How does one define health? If we’re honest, we have a “sick care” system designed around caring and paying for physical disease. But the World Health Organization definition [of health] is a “... state of complete physical, mental and social well-being, and not merely the absence of disease…” There’s never been a point in time where this is clearer than now – the stress, anxiety, depression, etc. of COVID has influenced the physical.

- One of the positive byproducts - employers are paying for it. We are seeing the integration of all the physical, mental, social… employers are looking for models that can address the “whole person” or “whole community.” We can’t bifurcate health based on body parts anymore.

- Often, physician adoption of anything is based on reimbursement for “it” – and doing nothing is expensive/non-economic – i.e., doing nothing runs contrary to primary care as a loss leader. That’s getting disrupted.

Q&A

A lot of doctors adopted telemedicine in a state of crisis, trying Zoom, Doximity, etc. to keep practices open. A lot of that is receding, but COVID is worse now… thinking through what doctors will do, does the “boil” reduce to a “simmer” (do we revert to 8-9-minute visits)?

JH & RS: There will likely be some regression. New advanced models haven’t been pushed forward. I met Ryan in Washington talking about his vision for APC. I chased him to come to CT and speak to [our] group. We want a virtual care model that’s more robust.

- All the health tech companies realize what’s going on w/ practice transformation, payment reform, and better access to patients. Some have one or two of the elements, others have all. Fortune 500 companies are saying, “This is what we want - give employees and dependents superior access and has behaviorist embedded.” These are closed-loop systems.

- A couple of weeks back the Primary Care Collaborative and National Alliance of Healthcare Purchaser Coalitions (covering about 50MM Americans) said, “This is the model we want and it must have all for this to be acceptable to us and our membership.” What does that mean? It means we’re seeing employers/groups ask for attributed, at-risk primary care -> in-person + virtual, coordinated care with specialists. That’s better than “transactional” telemedicine.

- Primary Care as a provider class has been underappreciated for a long time (used mainly for steerage). The new model creates leverage for PCPs. Agnostic steering to the biggest spend areas (musculoskeletal, cardiac, etc.). Not only are payers saying it, but big purchasers think it’s really important.

What are your expectations for change? Next quarter? Or is it the next 12-24 months? Is there a good way to measure it - % next year or is it a longer duration?

JH: This is why I brought Vera to CT. We’ve got 169 towns and cities doing things differently – it’s the “land of frozen molasses.” However, we’re seeing new entrants like Firefly Health and Dispatch Health shake things up, not only with existing provider groups regarding FFS arrangements but by inspiring payers to say, “We must have this as part of a value-based solution on a go-forward basis.”

- Partnerships w/ on the ground providers, embedding tech, creating interoperability, and bringing health tech to legacy operations -> it’s all happening [now].

- People like "disruptors" a lot. Dispatch is emergency/urgent care, which is normally expensive. They send PAs and RNs to members’/patients’ homes. This is highly competitive and eats into a significant revenue source for hospitals/IDNs. The Net Promoter Score (NPS) is 96.

Value-based reimbursement is single digits (%), when will it inflect?

RS: Look at telemedicine – it’s just a distribution channel at end of the day. You can distribute transactional sick care through an app, which leads to fragmentation, perhaps overutilization, etc. As a part of a bigger strategy, there’s tremendous value: better access to a care team, continuity of care, convenience in that context, etc.

- Provider adoption of telemedicine grew dramatically through COVID - providers were the bigger barrier to virtual care being adopted than consumers. We saw 85% of total visits virtual, up from ~5%. Today, we’re at about 30%. Even with the spike in cases, we’ve seen some regression in virtual – a lot depends on how care centers are set up and populations are served.

- The real question is appropriateness - you can get economies of scale, see more people, and manage more complex populations while gaining scale and greater confidence taking at-risk contracts. It’s a virtuous process – manage that population w/ a smaller footprint and more connectivity between the care team and members of population = greater control over the total chain. This takes the PCP from a loss leader to gatekeeper, with tech being an enabler/distribution channel, NOT the solution itself.

Is managed care on the back end of this? Do they lose out because you have better data/control over the flow and can take an at-risk contract?

RS & JH: Managed care as a standalone, perhaps. It’s more of a component of a vertically integrated solution. Managed care makes it work, but as a standalone, not so much. From a payer’s perspective - markets want to move to at-risk. They are afraid of everything from Optum to Amazon to blockchain and single-payer. There’s risk/disruption everywhere, and they always tried to hammer PCPs. We’ve seen more provider groups bring their own plans to market - so looking at vertical integration to get control over the supply chain. It’s not about big, bad, broad networks – it’s more about performance.

- The gatekeeper comment -> primary care becomes that managed care function for the whole system to function more efficiently.

Like HMOs in the 90s, but this version works?

RS: I think so, yes. Using PCPs well reduces waste. The advantage of APC is having high-quality providers across the system (working for different networks) stitched together for a better-functioning network that leverages primary care to steer traffic.

- JH: Managed care is different now. In the state of CT, the largest purchaser is the state w/ 200k active and retired plan members. The state is part of a group that’s moving from FFS to value-based arrangements through an alliance w/ ~2k PCPs steering agnostically into a network of excellence based on the condition - there are targeted prices, etc. for cancer, cardiac, labor & delivery, and even autism is under consideration. Coming out of the pandemic, purchasers are craving accountability and predictability more so than transparency. In fragmented FFS, you could pay 3x the cost of a hip replacement for an infection/complications. If you have attributed, you can steer agnostically to the best and offer a warranty for costly items. Chief Financial Officers love this concept, especially those w/ self-funded plans.

- The CFO or the benefits person, do they have enough product from Vera or whoever to fill the order? JH: No, but capacity is being built, yes. In a lot of states, APRNs become de facto PCPs. There’s huge demand for a closed-loop system – we see players like Centivo coming into the market.

- Is there adequate supply on the shelf for Fortune 500s? And does the benefits person you’re talking to keep doing PMPM (with Teladoc) until there’s enough players like Vera to meet demand? Teladoc could be a short, but it could keep going because healthcare is slow [to change]… RS: I think there’s a long tail for telehealth/telemedicine incumbents for a number of reasons. A) There’s demand, even if not understood, incumbents do a good job of selling, but there’s a lot of noise, and b) there are not many value-aligned consultants. So, a lot of purchasers will stick with what’s familiar. And there is independent primacy care out there (independents want to stay independent – they can treat a larger population w/ a smaller care team if using virtual care to improve efficiency). Probably will have a long shelf life, but the demand for integrated far outweighs independent.

- JH: In addition, eConsult platforms like RubiconMD are growing. These allow a PCP to speak/check w/ a specialist after seeing a patient vs. sending the patient to cardiology for a $600 consult, for example. These models are episodic care payment arrangements -> nuanced care paths, simple, interoperable, and they save employers money.

- Think about cancer, usually the largest programmatic spend and 73% of people diagnosed never get a second opinion.

- Ryan alluded to a “craving” – prior to March, everything in the economy was “fine.” The C-Suite wasn’t involved in buying or design discussions; however, now they are because employees were let go, there are financial stresses, etc.

- Payers are flush for 1/1 effective date – most didn’t lose much and offered 0% increases. For employers used to seeing 15-18% volatility in health spending – COVID raised awareness of health care spend, and I haven’t seen this many Fortune 500 companies pushing. A quote from Elizabeth Mitchell: “Employers are willing to do things that they haven’t done before.”

Nobody went to a doctor for 3-4 months…how does a rebound and rising acuity feed into worry at the C-Suite level?

RS: We can’t speak to the long-term impact of COVID-19, yet. The jury is still out, but there’s no question that people are concerned about a rebound AND avoidance of necessary care. Otherwise manageable conditions are out of control now... or out of management. The market at large is expecting price corrections because a lot of data suggests care avoidance today. There are real concerns about care avoidance, stress, anxiety, and depression, and then the impact the mental is having on the physical, and what it will all do to claims.

- Care patterns have been totally disrupted like any other pattern in life.

With capitated arrangements, how does Oak Street deal w/ rising acuity plus incremental catch-up visit - sicker patient showing up?

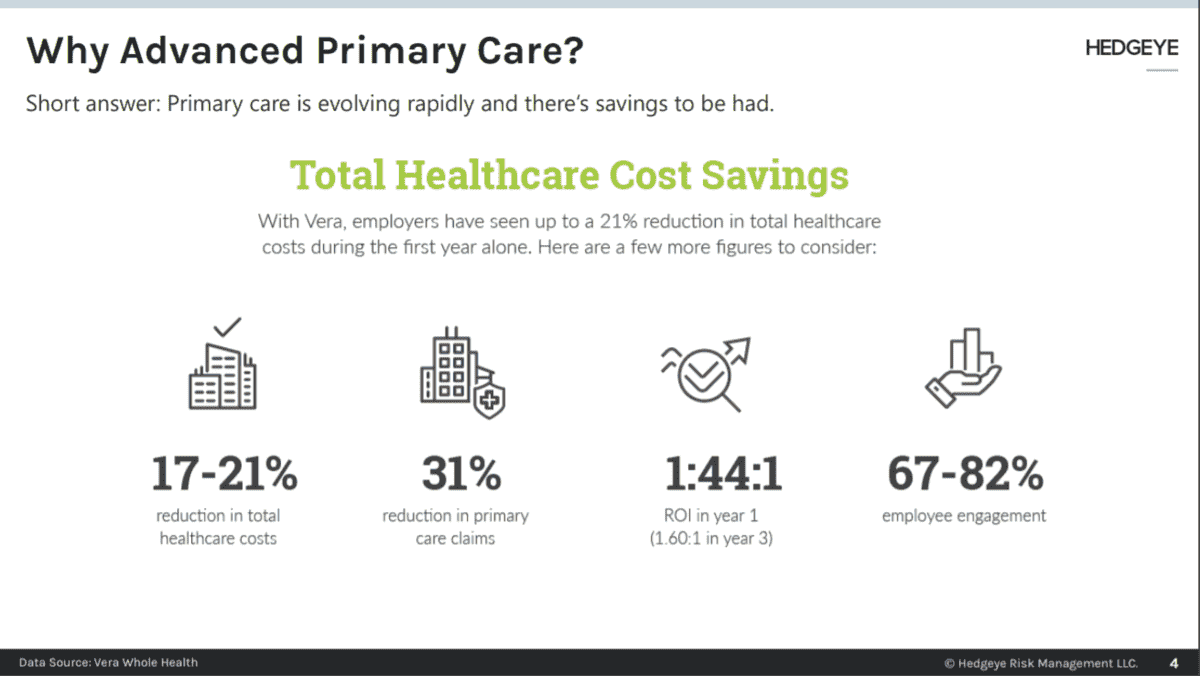

RS: That problem is less severe for employers that have had value-based arrangements. We’re a capitated model, at-risk on contracts. Total visit volume barely moved – it just shifted to virtual. Running respiratory clinics in the morning, sick visits in the afternoon, shuffling staff, some care teams working from home (for roughly 15k patients under management).

- That 15k group had roughly 1200 open care gaps when COVID-19 started. From March through October, the care team (6 people) closed all 1200 care gaps via phone calls, messaging, etc.

- Also, not all employees are home – many are front line/essential and at work.

JH: There are a thousand provider groups that may not come out of the pandemic. And my kids (a police officer and teacher) won’t go back to brick-and-mortar for routine care. They like virtual.

- Provider groups must 1) move to risk, 2) create better accessibility, and 3) integrate behavioral.

Is there a platform of choice? Epic’s myChart, Amwell, Teladoc/BetterHelp?

JH: A local company, Diameter Health, recently did a deal w/ Centene and Optum to tie EHR/EMR data together… it’s a huge problem - employers have all data streams, providers too. It’s the same thing for APC. Systems must talk to each other.

RS: We’re battling that. In reality, it’s exceedingly difficult for independent practice to stay a few providers, nothing to do w/ quality of care provided - most has to do w/ the question: “Do we make the financial investment to keep pace with tech requirements to operate today, especially if we move to risk.” There’s been billions spent over the years on FFS workflow investment - interoperability is a huge issue. Some may try to bypass interoperability and move toward cloud-based platforms that suck data out. There’s no easy answer.

JH: Agilon Health will partner with and teach PCPs how to move to risk-based contracts starting w/ Medicare Advantage, move to commercial. Optum does that well. Blockchain is another potential way.

RS: I can’t overstate how difficult change is given the dollars invested in FFS workflows, mentality, incentive programs. I’d argue that we need supply side pressure from disruptors like Vera, ONEM, OSH – everyone must work together.

Livongo/Teladoc

JH: Livongo - employer directed, market to diabetics – they’ve done a good job w/ marketing. However, DTC offerings that don’t integrate w/ employers are difficult for employers to wrap their heads around, especially at-risk. Avoiding catastrophic hits seems smart, but wellness programs didn’t do well and there’s a lot of skepticism. They are in a lot of the biggest employers, and the state of CT took on Livongo w/ a value-based program/contract for ’21.

RS: Diabetes management is one clinical pathway w/ in advanced primary care – but we can’t separate diabetes from depression or other issues. So, we try to think about the whole body. Livongo will be fine for the time being – the approach has a play until APC matures.

Is ‘22 a good year to think we’ll see the next step function change (vs. ’21 when we’re cleaning out the pandemic)?

RS: I think the train has left the station - will see a bunch of announcements w/in the next 3-6 months. Whatever acceleration experienced this year is only growing. It’s happening exponentially faster than we’ve ever seen.

About the Speakers

Jeffrey Hogan is the Northeast Regional Manager for Rogers Benefit Group, a national benefits marketing and consulting firm. Jeff has been with Rogers Benefit Group for 28 years. Additionally, he operates a consulting firm, Upside Health Advisors, which provides expert witness services on healthcare-related litigation, as well as advises payers and large provider groups on product development and launch strategies. Jeff has been a resource to employers desirous of implementing strategies to manage health spend more efficiently and is focused on healthcare payment reform, health policy issues, care coordination, value-based initiatives, and healthcare quality measures. He regularly appears on national forums focused on moving to value-based healthcare and is actively working to promote healthcare-related transparency measures in the market. Jeff is a current board member for the Connecticut Business Group on Health and serves as the group’s liaison to the National Alliance of Healthcare Purchaser’s Coalition. He is also is one of the Coordinators of Connecticut’s Moving to Value Alliance. He also serves on the Advisor’s Panel for the Validation Institute and is the Regional Leader for the Leapfrog Group.

Ryan Schmid is the Co-founder, President & CEO of Vera Whole Health, a market-leading “Advanced Primary Care” provider that delivers comprehensive, intelligent primary care to employees via employer-funded worksite clinics and insurers. Vera contracts with companies to build and operate dedicated on- and near-site primary care clinics for their employees and was named one of Washington’s 100 Best Companies to Work For by Seattle Business Magazine, and serves such groups as Seattle Children’s Hospital, The Bill & Melinda Gates Foundation, Virginia Mason Medical Center, City of Kirkland, Anchorage School District, and the Northern Arizona Public Employee Benefit Trust. He is also the co-founder of Hope Central Pediatric and Behavior Health and Rainier Health and Fitness, non-profits dedicated to improving the health and well-being of people in low-income areas.

Please email with any questions or feedback.

Thomas Tobin

Managing Director

Twitter

LinkedIn