This guest commentary was written on 12/16/20 by Chief Market Strategist Mike O'Rourke of JonesTrading.

We all have a front row seat to what will likely prove to be the most calamitous monetary policy in US history. There is not much any of us can do except buckle up and prepare to watch it unfold.

This won’t materialize overnight. This process has been a decade in the making but now the Fed has codified inane policy and is ignorant as to its ramifications.

The reason the unwind has not occurred sooner is the Fed intervened with asset purchases to prevent its financial bubbles from bursting - by blowing them even larger. Now that the 2% inflation target is the paramount objective of monetary policy, the asset purchases are no longer a crisis response tool but instead a conventional monetary policy resulting in perpetual easing.

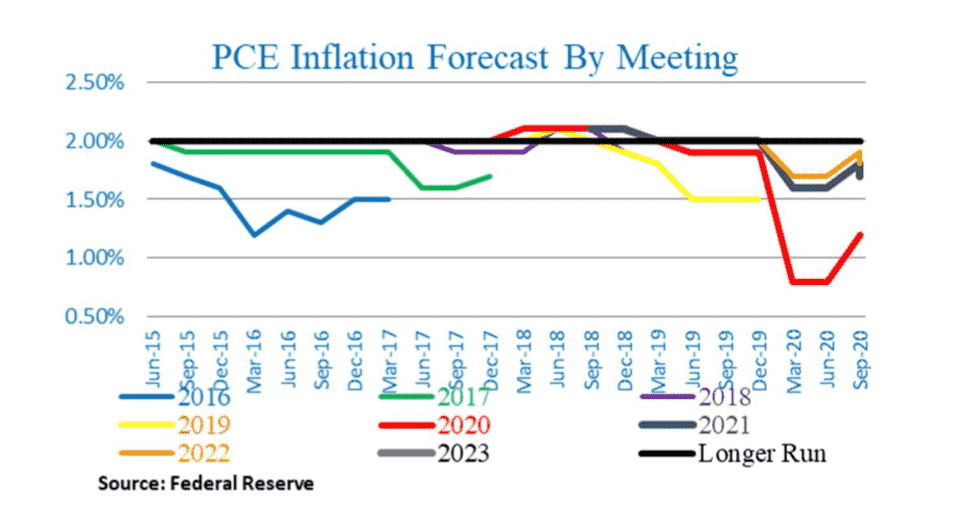

Bear with us as we highlight the important facts and how they tie into Chairman Powell’s press conference today. As we all know, the Fed’s inflation target is 2% PCE Inflation. If you ask anyone at the Fed why it is 2%, they cannot cite any current research or studies for why the 2% inflation rate is optimal for the US economy. The Fed will say that other central banks use it and as its website vaguely asserts, “evidence” supports 2%.

A number of countries adopted the practice in the 1990s. Thus, the overwhelming majority of the Federal Reserve commentary on the subject is from 17 to 20 years ago. That commentary, from the likes of former Chairs Bernanke and Yellen, advocated a target range.

Over the past two decades, PCE Inflation has averaged 1.8% and Core PCE has averaged 1.7%. It is important to note in the numerous instances when the Federal Reserve has announced asset purchases over the past 12 years, the size of the program was scaled to correspond with declines in asset prices, not inflation.

The Fed is incapable of quantifying the effect its $3 Trillion of asset purchases will have on PCE inflation. Since 2007, the size of the Fed’s Balance sheet has compounded at 19% per annum. Over the same time period, PCE inflation has averaged 1.5%. Of course, none of the Fed’s non-existent analysis takes into effect the structural shifts of globalization and technology on the economy. They can’t even be sure they are measuring inflation correctly.

Early in today’s press conference, Chairman Powell asserted:

|

“Our ability to achieve maximum employment in the years ahead depends importantly on having longer-term inflation expectations well anchored at 2 percent. As we reiterated in today’s statement, with inflation running persistently below 2 percent, we will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer-term inflation expectations remain well anchored at 2 percent. We expect to maintain an accommodative stance of monetary policy until these employment and inflation outcomes are achieved.” |

How did 2% inflation somehow become the magic number for full employment? Has the Chairman already forgotten we had record low 3.5% Unemployment in February of this year? PCE Inflation averaged 1.4% over the 5 years prior to that reading.

The Chairman continued, “With regard to interest rates, we continue to expect it will be appropriate to maintain the current 0 to 1/4 percent target range for the federal funds rate until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.”

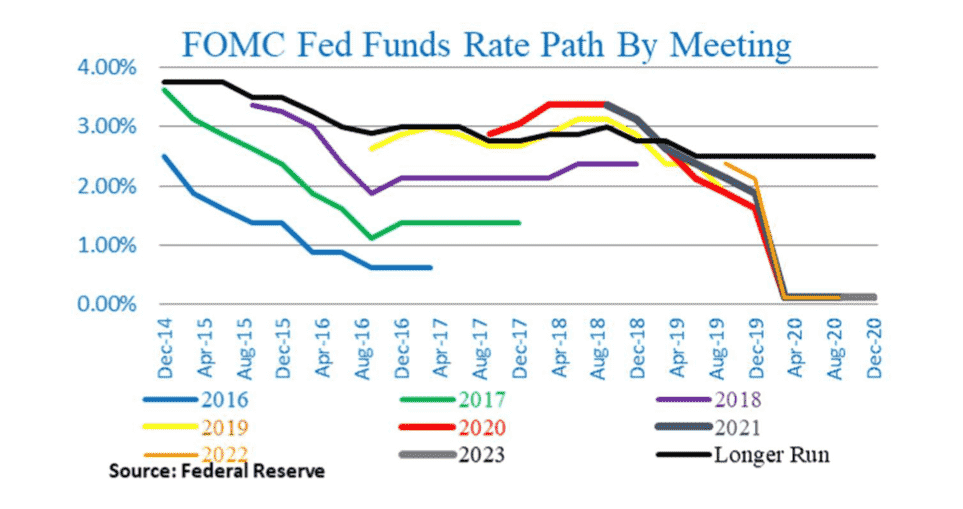

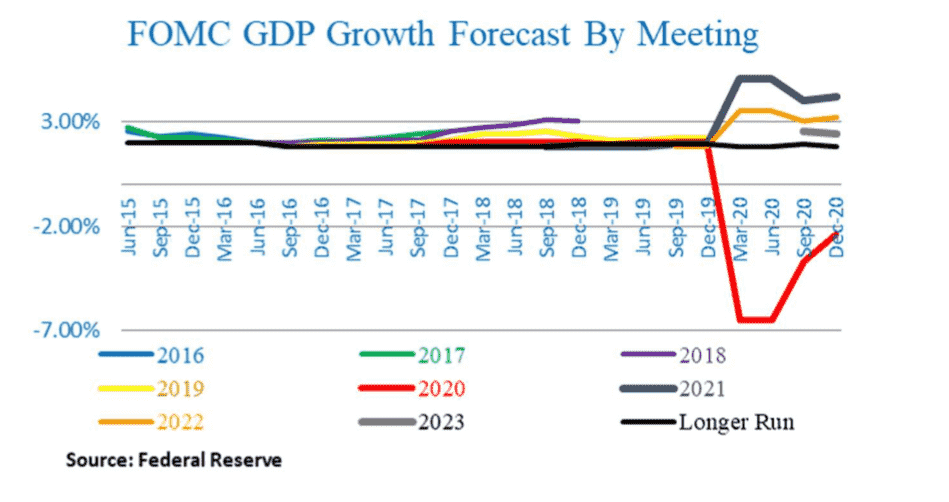

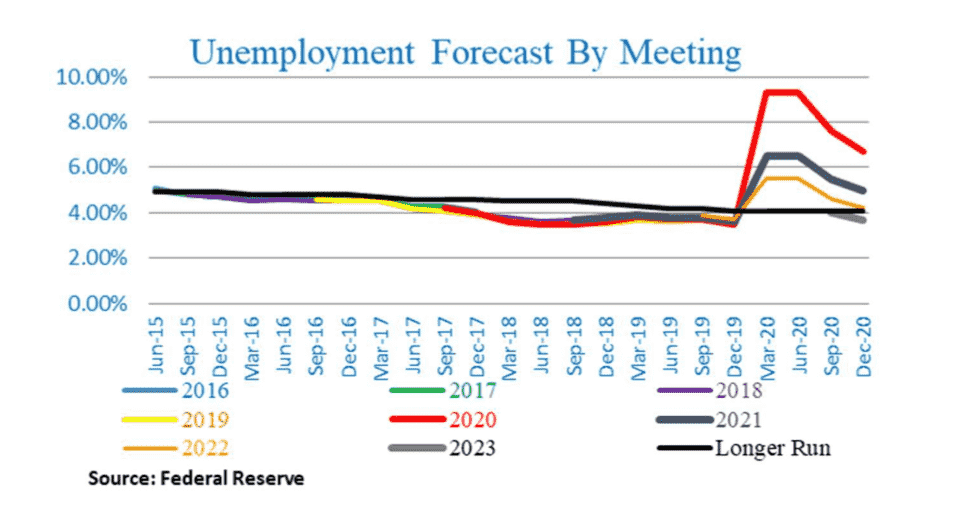

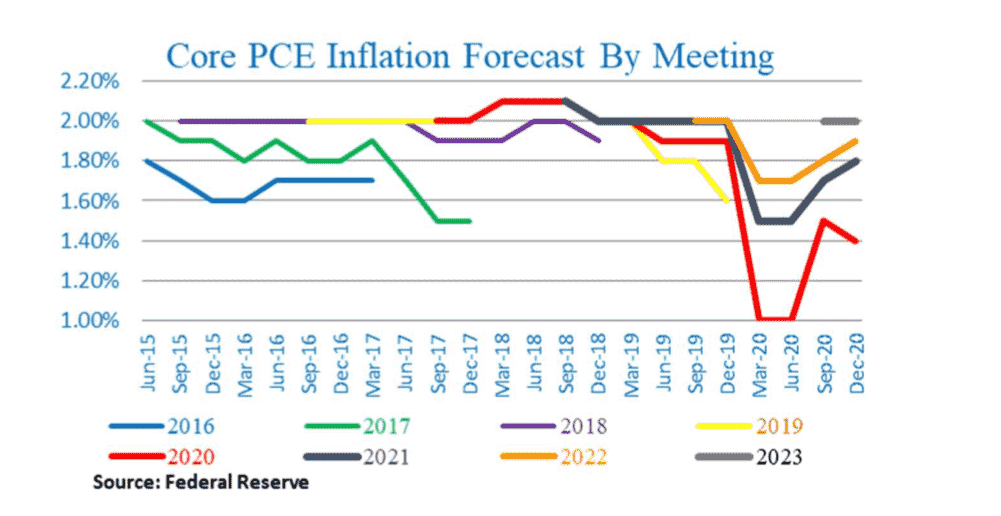

Thus, policy remains as it is indefinitely. The Fed forecast in the Summary of Economic Projections today continued to indicate that there will be no interest rate hikes for three years through the end of 2023 (chart below). That is despite the fact that this is the same report in which the Fed significantly raised its forecasts for GDP, and dramatically improved its forecasts for Unemployment for this year and the upcoming three.

The Fed’s year end 2023 Unemployment forecast is 3.7%, 20 basis points higher than the record lows from earlier this year. Yet they still won’t be tightening because PCE inflation is forecast to be only 2%, not the Fed’s conjured up “considerable period of time above 2%.”

We have reached such extremes in asset valuations that we no longer get pushback on our bubble assertions. S&P 500 earnings will be down approximately 19-24% this year, yet the S&P 500 is up 15%, and the Nasdaq 100 is up 45%. Yes, earnings will recover in 2021, but they will not exceed the 2019 level.

The S&P 500’s Market Cap to US GDP has eclipsed the extremes of 2000, whether it is the speculative IPO’s, overnight Billionaires who don’t have a commercial product or the massive retail options speculation.

It is harder to argue that is not a bubble, but Chairman Powell tried today. His comments should strike fear in all of us. When asked if he was concerned about asset valuations, Chairman Powell responded “With equities it depends whether you are looking at P/Es or whether you’re looking at the premium over the risk free return. If you look at P/Es they are historically high.

But in a world where the risk free rate is going to be low for a sustained period, the equity premium, which is the reward that you get for taking equity risk, would be what you would look at, and that’s not at incredible low levels. They are not overpriced in that sense.

Admittedly, P/Es are high, but that’s maybe not as relevant in a world where we think the ten year Treasury is going to be lower than where it has been historically from a return perspective.” What the Chairman failed to mention is that he has ordered the purchase of $2.3 Trillion in Treasuries this year, and he is the one responsible for the artificially expensive Treasuries (to which equities appear slightly cheaper).

Everyone always checks to see if China is selling its Treasury holdings, fearful it would be a major market event. China holds $1 Trillion worth of Treasuries, less than half of what the Fed has purchased in 2020. The Fed holds $4.6 Trillion in Treasuries and as the Chairman’s guidance today indicates, he will continue to buy just under $1 Trillion per year for each of the next 3 years.

The rest of the world in its entirety only holds $7 Trillion in Treasuries, so we will see the Fed surpass them in the next couple of years. To hear the Fed Chairman state that equities are not expensive relative to the risk free rate, a rate which he is essentially controlling, is disingenuous at best or negligent at worst.

Either way, for the Chairman to say that equities are “not overpriced” based on their comparison to instruments he is spending Trillions of dollars to manipulate, is an alarming proposition. It is even more terrifying that he does not comprehend what he is saying, as he has pledged to spend additional Trillions.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Mike O'Rourke, Chief Market Strategist of JonesTrading, where he advises institutional investors on market developments. He publishes "The Closing Print" on a daily basis in which his primary focus is identifying short term catalysts that drive daily trading activity while addressing how they fit into the “big picture.” This piece does not necessarily reflect the opinion of Hedgeye.