McDonald’s is scheduled to report its August sales numbers before the market open tomorrow. August 2010 had one less Saturday, and one additional Tuesday, than August 2009.

Below, I go through my take on what numbers will be received as GOOD, BAD, and NEUTRAL, for MCD comps by region. For comparison purposes, I have adjusted for calendar and trading day impacts. To recall, July same-store sales exceeded street expectations and I fully expect that August will also surprise to the upside.

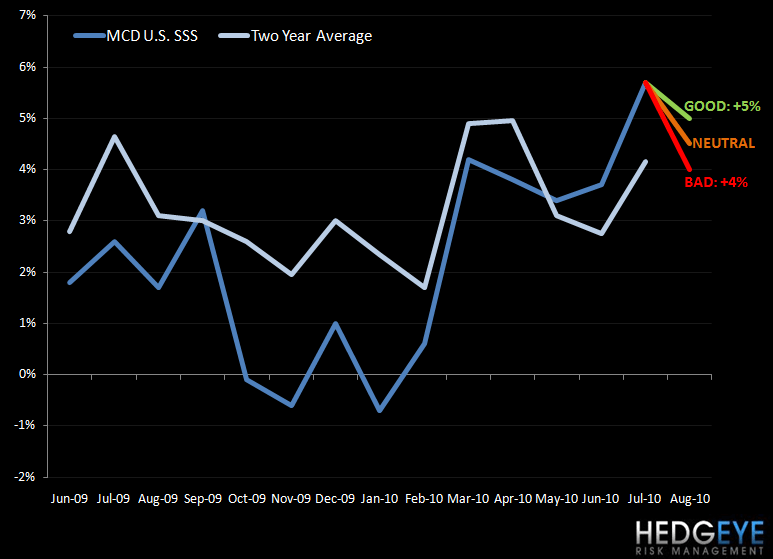

U.S. (facing a relatively easy 1.7% compare, including a calendar shift which impacted results by -0.7% to -0.8%, varying by area of the world):

GOOD: 5% or greater would be perceived as a good results because it would imply that the company was able to improve U.S two-year average same-store sales (by ~30+ bps) on a sequential basis. This would be a strong number in light of the average same-store sales figures for 2010, but it is clear that McDonald’s top-line has stepped up meaningfully and I actually expect a print of 7% or more for August. This would be far in excess of the current consensus same-store sales number of 4.4% for the U.S. August results. Smoothie sales continue to be strong; while a result of 5% or greater would be received positively by the Street, a number of 7% or more is in play.

NEUTRAL: Roughly 4% to 5% implies two-year average trends that are approximately in line with those seen in July. I would view this range with a positive bias and expect any neutral result to fall in the upper quintile. Lower than that would be slightly disappointing.

BAD: Below 4% would indicate that two-year trends have deteriorated on a sequential basis. Following two consecutive strong months of top-line performance in the United States, it would be disappointing if two-year trends were to slow from here. Sales of smoothies, said on the 2Q earnings call to be “blowing away high-end projections”, remained “top contributors” to sales growth in July. I expect that sales of smoothies and core products improved on a sequential basis in August.

Europe (facing a relatively easy 3.5% compare, including a calendar shift which impacted results by -0.7% to -0.8%, varying by area of the world):

GOOD: 6.5% or better would be a good result for MCD’s Europe operations as it would imply a level two-year trend following a strong month in June. While a print of 6.5% would actually be a sequential slowdown in trends of approximately 10 bps, it would represent the highest same-store sales results since September 2009.

NEUTRAL: 5.5% to 6.5% would imply two-year average trends that had declined slightly below those seen in July. This would be received as NEUTRAL because July trends were particularly strong on a two-year basis, therefore a deceleration, provided it is only marginal, would not be viewed with much disappointment.

BAD: Below 5.5% would imply two-year average trends that have declined sharply from July’s results. The Street is expecting a number of 5.2%, but it seems that the global business has been performing strongly and exceeded expectations in July – I believe it will once again do so in August.

APMEA (facing a relatively easy -0.5% compare, including a calendar shift which impacted results by -0.7 to -0.8%, varying by area of the world):

GOOD: A print of 10% would imply trends roughly in line with those seen in July. Any improvement would, of course, be well-received, but a print that sustains the strong improvement in July from June’s poor number would be viewed positively.

NEUTRAL: Comparable-store sales of 8% to 10% would result in two-year average trends slightly below those seen in July but still above the lower level implied by June’s result. On a one-year basis, this range also implies a number far in excess of the disappointing APMEA sales results of March, April, and May.

BAD: Same-store sales of 8% or less would imply a significant sequential slow down from July’s trends. Additionally, if the result is in the region of 7.5% or lower, it would imply results even worse than June on a two-year average basis. The Street is expecting a number of 7.4%. I believe this is conservative given that a print of 7% would yield a two-year average number of 3.6% - a mere 20 bps over the trough December two-year number.

Howard Penney

Managing Director