This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst. This piece does not necessarily reflect the opinion of Hedgeye.

As the very difficult year of 2020 grinds to a conclusion, the world is not much closer to dealing with COVID than it was six months ago.

Leaving aside the supposed success of the Chinese police state, the rest of the world is struggling to protect vulnerable populations, but all the while destroying the economic and social lives of the entire population. Vulnerable populations do not wish to be isolated, so instead we lock down the entire community and destroy the entire economy.

Go figure.

New York Governor Andrew Cuomo, who is tipped to be Attorney General in a Joe Biden Administration, has again shut down the restaurants in New York City. There is no evidence that indoor dining is contributing to the significant spike in COVID cases in New York City, where roughly half the patients are coming from the city’s nursing homes. Governor Cuomo apparently cannot resist the temptation to destroy what remains of the city’s economy before heading to Washington. In this regard, we note sadly that 21 Club has closed its doors.

Pondering the outlook for 2021, we first must note the buoyant state of the US equity markets, which are giving investors less and less cash flow at ever higher prices. The double-digit asset price inflation seemingly satisfies the requirement of the Federal Open Market Committee to see prices higher. But no, the US central bank continues to buy hundreds of billions in Treasury debt and mortgage-backed securities each month, creating an asset bubble that must eventually collapse into a massive correction.

Students of recent history will recognize the parallel between the actions of the FOMC today and the Fed under former Chairman Alan Greenspan, who stepped on the monetary gas in the early 2000s and thereby fueled the mortgage market boom and bust that ended in 2008.

This time, the Fed has increased its market manipulations by an order of magnitude, suggesting several more years of residential mortgage boom for lenders (if not MBS investors), followed by a 2008 squared correction in 2024 or 2025.

If the world of residential mortgage lending is headed for another good year, the situation in the commercial real estate sector is dismal and growing worse by the day. As we noted in the latest edition of The IRA Bank Book for Q4 2020 (“Is there a Bull Case for US Bank Stocks?”):

|

“We anticipate that just as the early period immediately following the Great Crash of 1929 was relatively stable, but was then followed by years of wrenching credit deflation, in 2021-2023 we are likely to see substantial restructuring of business assets and commercial real estate. These once blue-chip assets have been rendered moribund by the social distancing requirements of the response to COVID. Just imagine how empty office and retail buildings in downtown Manhattan or Chicago or Los Angeles will be revalued in the next 24 months and you begin to appreciate the future impact on commercial real estate credit and related public sector obligors." |

The risk presented by the changes in behavior compelled by COVID have only begun to emerge into view in asset classes such as commercial real estate. Unlike residential mortgages, which are relatively homogeneous and thus may be described in aggregate, commercial real estate is a chopped salad of assets and locations that can only be understood in particular. Yes, much of the commercial real estate in New York City is impaired vs valuations of 12 months ago, but how impaired is a far more complex question.

If all of this were not enough, there is another variable that has yet to be resolved as we approach year end, namely whether Congress will enact further spending to address the economic dislocation from COVID.

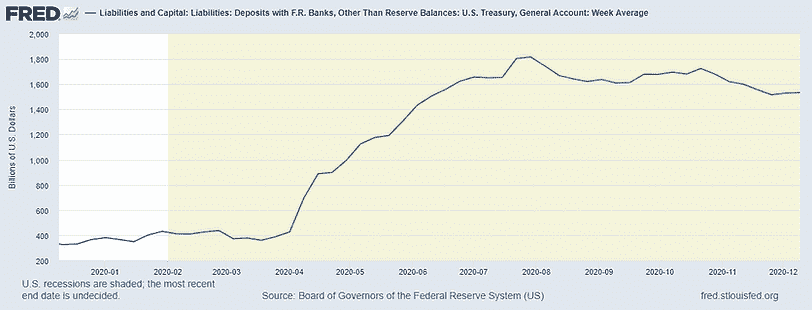

The answer to this question will directly impact the size of the Treasury General Account or TGA, which is the buffer the Treasury uses to manage cash payments and receipts.

Huther, Pettit and Wilkinson (2019) note in their fascinating paper (“Fiscal Flow Volatility and Reserves”):

|

“A dollar paid to the Treasury in taxes directly reduces the amount of reserves in the banking system by one dollar, while a dollar paid by the Treasury directly increases the amount of reserves in the banking system by one dollar. This has not always been the case; prior to the financial crisis, tax receipts were held in (and expenditures paid from) the Treasury's accounts at commercial banks, a practice that left the stock of bank reserves unaffected by fiscal flows.” |

As the chart below illustrates, the Treasury stopped depositing funds with commercial banks since 2009, greatly magnifying the market volatility cause by changes in payments and receipts.

After passage of the Cares Act, the size of the TGA was expanded by Treasury from $130 billion to several trillion, but this authority is temporary and reflects the assumption of future spending -- spending that may never materialize. Should Congress fail to authorize new emergency spending outlays, Treasury will theoretically be forced to return the cash to the markets by ceasing the issuance of new debt for several months.

Lorie Logan, EVP at the Federal Reserve Bank of New York, told the Money Marketeers of New York University on December 1st:

|

"[T]he TGA has risen dramatically since March, as the Treasury Department built cash balances to prepare for potentially unprecedented outflows related to the pandemic response. Treasury’s cash management policy is motivated by precautionary risk management and calibrated to allow Treasury to cover outflows in case of a temporary interruption to market access. The TGA currently stands at roughly $1.5 trillion, nearly four times its largest size prior to this year. This balance is generally expected to fall in the coming months and, while the extent of the decline is uncertain, most expect the balance to remain well above historical norms." |

Just imagine what happens to interest rates and the credit markets more generally if there is no further pandemic response and Treasury must slow or even cease issuance of at least T-bills, and perhaps notes and bonds.

Fed monetary policy would be rendered irrelevant as the supply of Treasury obligations available for purchase would dry up. Could the FOMC force banks and private investors to sell their Treasury holdings to fuel the fires of inflation?

Bond market strategist George Goncalves tells The IRA:

|

"The Fed is really going to be walking a tightrope between how much liquidity gets unleashed and when. Luckily we have seen this movie before, but never to the levels we are potentially faced with ahead. Each time the Treasury has faced the debt ceiling dance it has resulted in a wind down in the TGA account to the bare minimum and with it an eventual reduction in T-bill auction sizes in order to operate under the ceiling. The issue now is the size and timing of it all. In the past the Treasury had $350-400bn on average to start with in the TGA, now its well over 4x times those levels so that alone can amplify through funding markets more severely. The movement of over $1 trillion from TGA back to reserves through the reduction in T-bill supply also will reduce collateral for the most highly sought after paper in the system." |

If Treasury is forced to return cash now in the TGA, the ability of banks and other financial intermediaries to hedge finance risk would be entirely disrupted.

Even a short hiatus in Treasury debt issuance could throw the mortgage and secured finance markets into chaos as the return of cash by the Treasury swelled bank reserves, but risk-free collateral would disappear. Goncalves continues:

|

"The TGA issue, coupled with persistently large money market fund balances remaining into the start of the next year is a recipe to collapse short rates into negative territory in the 1st half of 2021 and throw another wrench into the system at a time that the Fed continues to claim it won’t go down the NIRP path. There is talk of using reverse repos to try to mop up some of this up TGA/reserve switch, but they know it won’t be enough. Overall, the Fed and Treasury both over-reacted to Covid induced market vol earlier in the year and now will need to deal with the hangover into 2021." |

We understand from several bond market analysts that the most likely scenario would see Treasury Secretary-designate Janet "QE" Yellen forced to slow sales of Treasury bills for months, forcing short-term interest rates sharply negative as Treasury collateral disappeared. The too-be-announced (TBA) market for residential mortgages would be thrown into chaos and the repo market would be thrown into total disarray. The supposed market for SOFR would also evaporate overnight. Good thing we still have LIBOR!

As we’ve noted several times since the start of quantitative easing, allowing the FOMC to conduct massive open market purchases of Treasury securities and MBS has a considerable downside – especially when the Fed is also holding the Treasury’s cash in the TGA.

The Fed and Treasury are alter egos, like two faces of a Hindu deity, thus the market risk is magnified when the Treasury and the Fed are pursuing divergent policy goals.

The other more profound point raised by the size of the TGA is that the Treasury now accounts for about 25% of the Fed's balance sheet. Or put another way, the Treasury is funding about $1.6 trillion worth of QE. The cash deposits made by Treasury into the TGA must be collateralized with Treasury securities, meaning that $1.6 trillion worth of QE has no impact on bank reserves and is not supporting FOMC policy. As a practical as well as political matter, Treasury must reduce the size of the TGA or risk detracting from the FOMC's monetary policy actions.

So, for example, if Senate Republicans led by Mitch McConnell (R-KY) say no to trillions more spending and bailouts demanded by the socialist tendency that controls the House of Representatives, does this mean the Treasury will suspend issuance of T-bills? Indeed, Treasury Secretary Steven Mnuchin is already letting the TGA run off so as to leave an empty cupboard for Chair Yellen.

This bizarre situation illustrates the fact that once the FOMC turned to the dark side by embracing QE, it essentially lost control of monetary policy. More than ever before, the Treasury is the fiscal policy dog and the Federal Reserve System is the increasingly superfluous tail.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.