Below is a complimentary Demography Unplugged research note written on 12/8/20 by Hedgeye Demography analyst Neil Howe. Click here to learn more and subscribe.

|

Political pressure to cancel student debt is mounting—and so are the tensions surrounding the idea. Economists, activists, and policymakers are deeply divided over debt forgiveness and disagree on whether it would help or hurt the economy. (The Washington Post) |

NH: Roughly 43 million Americans now owe $1.6 trillion in student debt. It has tripled since 2007 and has grown to become the largest category of personal debt after mortgages. A majority of Americans back some level of debt forgiveness: Fully 60% of registered voters in a Hill-HarrisX poll last month said that they would support President-elect Joe Biden cancelling up to $50,000 of debt per person. This rises to 73% among 18- to 34-year-olds and 68% among 35- to 49-year-olds.

With Biden set to take office in January and the economy still in Covid-19’s grip, congressional Democrats and activist groups are urging Biden to make student loan forgiveness a priority for his first 100 days. At a recent press conference, Biden affirmed his support for legislation that would offer a $10,000 write-off to “economically distressed borrowers” with student loans.

But some Democrats (the Sanders/Warren contingent) are pushing for Biden to forgive most or all of it. They argue that doing so would help millions of cash-strapped Americans and put those payments back into the economy at a time when it desperately needs stimulus.

But critics--both Republicans and moderate Democrats--say that these proposals are misguided. First, student loan payments do not often force young adults into destitution.

Borrowers are allowed to reduce their payments according to their income, and millions defer their repayment schedule by many years. On average, borrowers only repay about one percent of their debt every year. (See “Student Loans Make Up a Record Share of Defaulted Loans.”)

Second, debt forgiveness is being discussed like it’s a one-and-done deal. But in practice it would surely commit the federal government to doing it again in the future. And this implicit promise would push future students (and their families) to maximize debt in the expectation that American taxpayers would eventually pay it back.

In so doing it would suppress even further any consumer price sensitivity to whatever price the Ivies and their ilk want to charge.

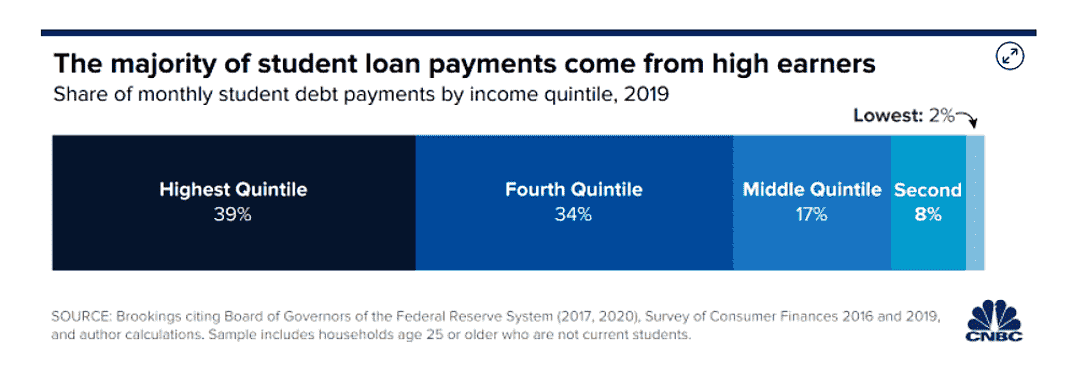

A third objection is that debt forgiveness transfers resources to those who aren't especially in need. Arguably, the biggest beneficiaries of debt cancellation would be high-income households. Borrowers with the highest student debt loads are mostly high earners (namely: lawyers, doctors, or MBA grads who went to pricey professional schools). Sixty-four percent of Americans age 25 and older do not have a four-year college degree. Should we be taxing the latter to relieve the former?

A recent analysis from professors at the University of Pennsylvania and the University of Chicago found that debt forgiveness plans--even if they’re capped at $10K or $50K--would have “highly regressive” effects.

What’s more, they would actually exacerbate the wealth gap between blacks and whites by delivering a much greater share of benefits to white borrowers.

Of course, debt forgiveness policies could be adjusted to target lower-income borrowers. The government could use tax records to forgive only the debt held by people below a certain income level. But this risks sparking resentment from less-affluent Americans who scrimped to go to college without borrowing or from those who have paid off their debt already. Why not consider other policies that could benefit people across the board and automatically favor younger or lower-income workers? This might mean offering a larger tax credit for first-time home buyers. Or a more generous EITC. Or, if we need fast cash, just sending out another round of stimulus checks.

I've commented on the student debt burden extensively over the years. (See “Six-Figure Tuitions Are Coming to Colleges,” “Shackled by Student Debt,” and “High Cost of Higher Education Can Put Families Into Impossible Binds.”) IMO, what we need more than debt forgiveness is to change the conditions that led college costs to soar in the first place. (See “How to Control the Exploding Price of Higher Ed.”)

The only way to make the cost of higher ed go down and stay down is to level the competitive playing field--and that means constricting demand, expanding supply, improving transparency, and encouraging innovation.

Colleges possess such extraordinary pricing power in part because they bar or discourage new competitors and in part because lazy employers rely on a limited number of them to act as credential gate keepers. What federal policy ought to do is actively promote new types of educational institutions better fitted to employer needs and to promote measures by which families can fairly compare the value-added of different schools. Colleges and collegiate associations actively discourage all of the above.

In sum, it's a mistake to enact a student debt jubilee without first rethinking and recasting the whole market for higher education. Otherwise, we’ll either end up right back where we started (with millions of new students crushed by huge debt loads) or somewhere we don’t want to go (with taxpayers committed to covering the cost of whatever colleges want to charge... a bit like they now do with healthcare providers).

There has to be a better way.

* * *

ABOUT NEIL HOWE

Neil Howe is a renowned authority on generations and social change in America. An acclaimed bestselling author and speaker, he is the nation's leading thinker on today's generations—who they are, what motivates them, and how they will shape America's future.

A historian, economist, and demographer, Howe is also a recognized authority on global aging, long-term fiscal policy, and migration. He is a senior associate to the Center for Strategic and International Studies (CSIS) in Washington, D.C., where he helps direct the CSIS Global Aging Initiative.

Howe has written over a dozen books on generations, demographic change, and fiscal policy, many of them with William Strauss. Howe and Strauss' first book, Generations is a history of America told as a sequence of generational biographies. Vice President Al Gore called it "the most stimulating book on American history that I have ever read" and sent a copy to every member of Congress. Newt Gingrich called it "an intellectual tour de force." Of their book, The Fourth Turning, The Boston Globe wrote, "If Howe and Strauss are right, they will take their place among the great American prophets."

Howe and Strauss originally coined the term "Millennial Generation" in 1991, and wrote the pioneering book on this generation, Millennials Rising. His work has been featured frequently in the media, including USA Today, CNN, the New York Times, and CBS' 60 Minutes.

Previously, with Peter G. Peterson, Howe co-authored On Borrowed Time, a pioneering call for budgetary reform and The Graying of the Great Powers with Richard Jackson.

Howe received his B.A. at U.C. Berkeley and later earned graduate degrees in economics and history from Yale University.