MPEL up/Wynn down. With detailed data in hand, the shifts look more sustainable.

Macau gaming revenues grew almost 40% YoY in August. Considering the stronger pace in the first half of the month, 40% growth is a little disappointing. In looking at the breakdown between Mass revenue, VIP revenue, and VIP hold, it doesn’t look like luck played a major factor in the month.

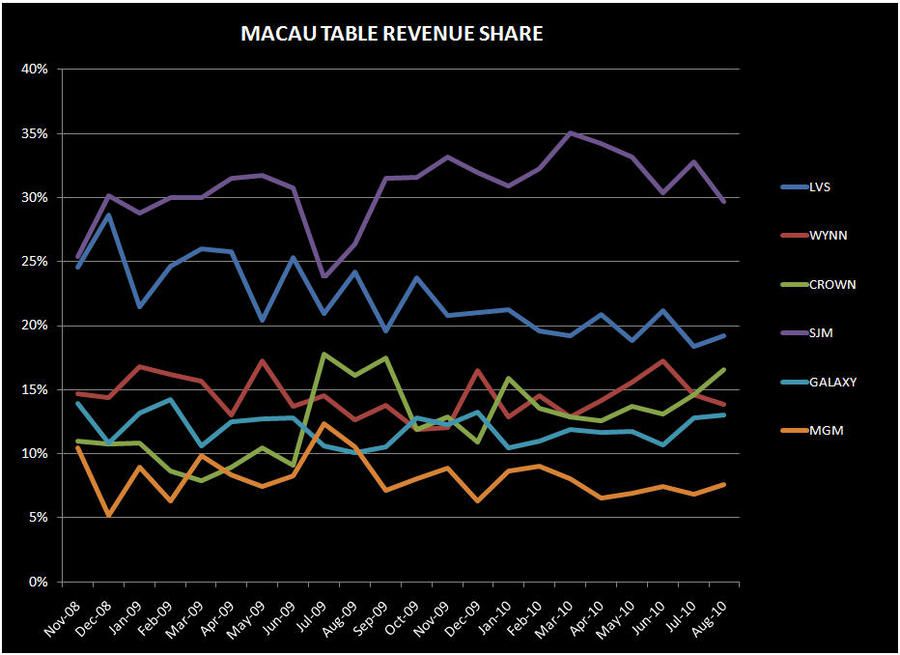

In terms of market share, MPEL and Wynn moving in opposite directions is the most interesting trend. We saw it in July and here again in August. As can be seen in the following market share charts, Wynn’s market share fell again, to 14.2% from 15.0% and 17.4% in July and June, respectively. On the other hand, MPEL had another strong month with its highest market share in almost a year, and it was mostly VIP volume related, not just high hold.

Wynn VIP hold % was consistent with last year but surprisingly, Wynn lost a lot of Mass share, down 180bps sequentially to 9.2%. August was the 2nd lowest ever for the company. Owing to an easy comparison, Wynn did grow total revenue 50% YoY, although high margin Mass only climbed 9%.

LVS seemed to hold very well on VIP which pushed up their market share to 19.9%, still below its TTM average. SJM played unlucky on the VIP tables which pressured their market share significantly sequentially. Finally, as we expected, MGM is starting to build market share due to the addition of a new junket, “David Star”, which had been active at Wynn (thanks Mr. Kwong).