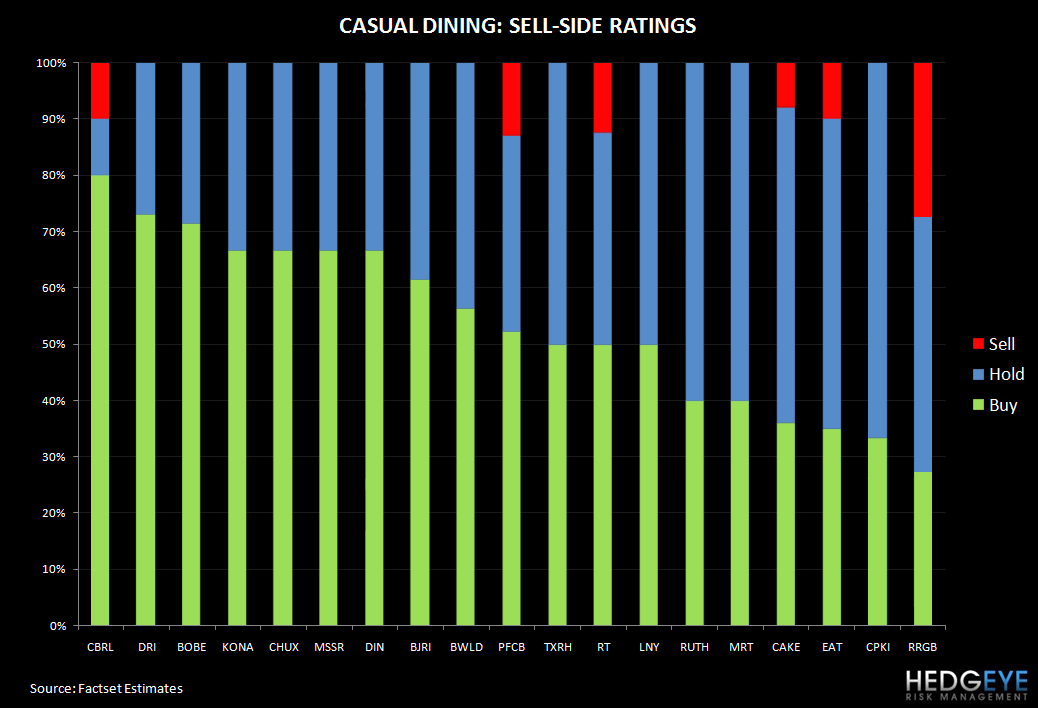

I know I am not alone on my bearish stance on RRGB. Nearly 30% of sell-side analysts rate the stock as a sell, which is the highest percentage of sell ratings among all of the casual dining names. Short interest also remains high relative to its peers at 12%. That being said, I would not view the nearly 20% pullback in RRGB’s stock price since reporting sequentially better 1Q10 same-store sales trends on May 20 or the company’s relatively low NTM EV/EBITDA multiple of 5.5x versus the casual dining group average of 6.1x as a reason to become incrementally more positive on the name.

Same-store sales trends continue to be choppy and unpredictable. After showing a sharp improvement in comp trends during the first quarter, same-store sales during the second quarter slowed 115 bps on a two-year average. The company attributed its improvement during the first quarter to the success of its spring LTO, which was supported with four weeks of TV advertising. It is important to remember that RRGB spent about $6.7 million on its TV campaign during 1Q10 and expects to spend about $15.6 million for the full-year versus $2.5 million during 2009. The increased advertising has driven improved comp results in the weeks the company is on air with its promotion but has not led to sustained improvements in the weeks following the campaign.

During the second quarter, same-store sales growth improved to +1.6% during the last four weeks of the quarter when supported by three weeks of TV advertising relative to the 2.6% decline during the first eight weeks of the quarter with no TV support. This implies a 225 bp improvement in two-year average trends from the first eight weeks of the quarter to the last four weeks, but for the entire second quarter, two-year average trends still decelerated 115 bps. During the first four weeks of 3Q10, same-store sales increased 1.4%, which management seemed bulled up about as it shows a marked improvement from the -1.2% number in 2Q10. However, given that the company is lapping a 15.3% decline from the first four weeks of 3Q09, the +1.4% actually implies continued deceleration in two-year average trends to -7% from -6.4% during 2Q10. And, the first four weeks of 3Q10 included one week of TV support for RRGB’s summer LTO.

Advertising is Addictive…I have been highlighting this problem for some time as RRGB continually changes its strategy around whether or not to spend behind advertising. Although the company often experiences a lift in comp results as a result of its incremental spending, the company cannot increase its level of spending forever. And, the returns do not always justify the spending. In 2008, RRGB spent about $18 million on TV advertising, up from $11.5 million in 2007. After a difficult 2008, the company decided to not invest so heavily behind TV support and only spent about $2.5 million in 2009. Now, in 2010, they are upping the spending drastically to $15.6 million.

When the company first introduced its 2010 media plans, it said “Based on the results of the spring LTO promotion, television advertising may be used to support the remainder of Red Robin’s LTO promotions in 2010, but no decision on subsequent campaigns has been made.” The spring LTO did drive sequentially better trends during the first quarter, but the company has lowered its comp guidance two times since initially providing its FY10 guidance. Current same-store sales guidance is -0.5% to +0.5%, down significantly from the company’s initial +2.4% to +3.4% range. In addition to the need to lower full-year same-store sales guidance, management said that macroeconomic conditions during the second quarter diminished the impact of the company’s Q2 TV media support. And yet, the company is going ahead with its planned spending to support the final fall LTO in the back half of the year. Management will not walk away from this spending because it needs the LTO and TV support in order to even come close to achieving its new comp target.

What happened in 2Q10 relative 1Q10?

Management stated that macroeconomic challenges worsened during the second quarter and negatively impacted consumer spending consumer confidence. Specifically, management stated, “We believe these challenges diminished the impact of our Q2 TV media support, compared to the impact of the TV in Q1, specifically the widely-publicized downturn in consumer confidence in June and July, as well as the underemployment and unemployment levels, have continued to create headwinds to strengthening guest count and sales trends.” This is a valid point, but this will continue to be a headwind over the next couple of quarters.

The company’s spring LTO, which ran during the first quarter, featured a $5.99 price point whereas the 2Q10/early 3Q10 summer LTO promoted a $6.99 price point. Although this higher price point is more beneficial to average check and margin, it does not drive the same level of traffic. The company reported that the summer promotion represented about 7% of total mix versus 10% mix for the $5.99 LTO in 1Q10. The company is sticking with the $6.99 price point for its fall LTO, which will begin in September and will be supported by two weeks of TV advertising during 3Q10 and two weeks in 4Q10.

Highlighting the significant volatility in results in the post-media period early in the second quarter, management commented that it saw large spikes both up and down during the second quarter, as much as 15% swings either way from week to week. Such volatility hurt margins in 2Q10 as the company was unable to adjust it labor levels accordingly as such swings were unpredictable. This will likely continue to be a problem in the back half of the year as the company goes on and off air with its support around the fall LTO.

Given the slow start to the third quarter on a two-year average basis, which included one week of TV advertising, and the growing pressure on consumers, I am modeling +1.5% same-store sales growth during 3Q10, which implies a slight deceleration in two-year average trends from the second quarter. On a full-year basis, I am modeling a 0.9% decline in comps, which falls short of management’s -0.5% to +0.5% guidance. For reference, a 50 bp decrease in same-store sales growth equates to a $0.11 decrease in EPS. My full-year EPS estimate is currently $0.75, below the street’s $0.85 estimate.

Restaurant-level margin will come under increased pressure during the second half of the year as a result of continued pressure from lower check averages as a result of the summer and fall LTOs and due to higher ground beef and dairy prices. Year-over-year restaurant-level margin compares get easier, however, in the back half of the year and although I would expect another quarter of declines during the third quarter, YOY restaurant-level margin will likely turn positive during 4Q10 for the first time in eight quarters.

Increased visibility…

Although RRGB could potentially move out of Hedgeye’s Deep Hole during 3Q10 (after being there for seven consecutive quarters), I don’t think this name will really work until it pursues a strategy that drives more predictable top-line trends. I am expecting the casual dining names in general to have a tough back half of the year from a demand perspective, but RRGB’s volatility in results exacerbates investor anxiety. The company announced that Stephen E. Carley will be RRGB’s new CEO, effective September 13. In the near-term, this transition could amplify the company’s lack of consistency. New direction, with time, however, could lead to increased visibility and consistency, but we will have to wait to see.

Howard Penney

Managing Director