Sports Apparel Data: Pre Sales Day Scoop

While we don’t read too deep into a single week’s sales as reported by POS data vendors, there’s a couple of items worth calling out for you to bake into your process for handling the sales-day onslaught tomorrow.

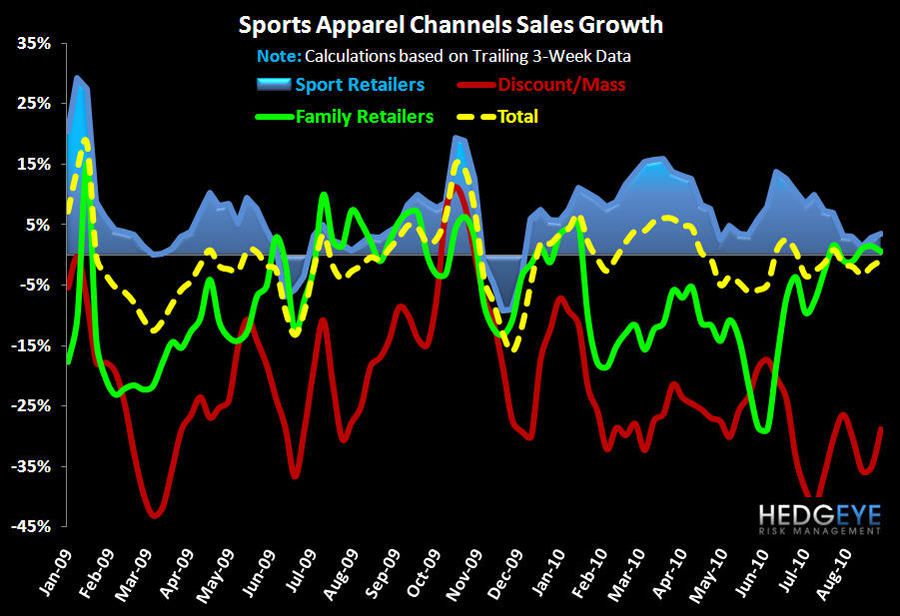

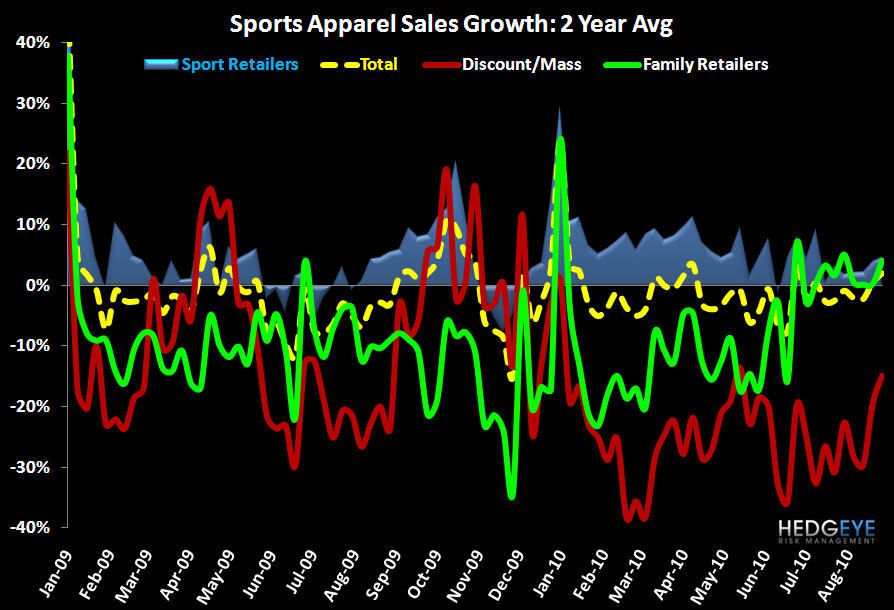

- The punchline is that the back half of the month stabilized after a steep drop at the start of August.

- On the whole, the month does not appear to be meaningfully worse (or better) than July. But keep in mind that this sample is drawn from the sporting goods category – which consistently outpaced retail overall for the whole year.

- Channel trends are consistent with what we’ve seen in the past, with the sporting goods channel proper leading the numbers. But as it relates to a read-through for the rest of retail, it’s worth noting that the discount and mass channels are getting ‘less horrible’ on the margin. That’s probably a decent sign for inventory.

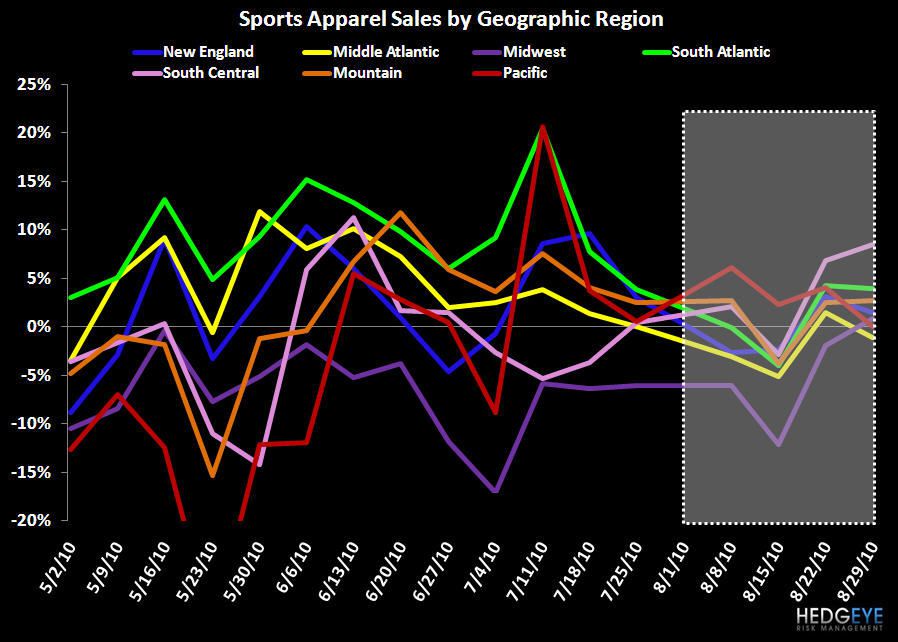

- There is fair consistency amongst regions, with the Middle Atlantic as the biggest negative callout. The Pacific region had a tough finish to the month, but that’s a wash as it also avoided the severe dropoff the rest of the country saw in week 2.