This note was originally published at 8am this morning, September 1, 2010. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

________________________________________________________________________

“Do not go where the path may lead, go instead where there is not a path and leave a trail.”

-Ralph Waldo Emerson

A college hockey coach sent me a nice recruiting letter about fifteen years ago with the quote above handwritten on it. Although I ended up not going to the college he coached at, he did catch my attention with the quote. At the time, as a rangy defenseman from a small town in Alberta, I’m pretty sure I didn’t know who Emerson was and I had certainly never seen the quote before. As a result, I was quite moved by the concept and idea embedded within the quote.

Emerson was known as a passionate individualist and a “prescient critic of the countervailing pressures of society”. He spread his gospel via dozens of essays and many hundreds of public lectures across the United States. According to Wikipedia, Ralph Waldo Emerson was an American philosopher, lecturer, essayist, and poet. Were he alive today, I think he may have been a Hedgeye.

In the short history of our firm, we’ve been accused of many things. On the political front, we’ve been accused of being both Republican and Democrat. On the market front, we’ve been accused of being bullish and bearish, and sometimes both at the same time. We’ve also been accused of being grumpy (well, mostly Keith before his coffee) and overly negative. The bottom line is that we have opinions, which are sometimes offensive to people, but those opinions aren’t to make ourselves feel better. They are based on data and analysis with the objective of producing high quality and accurate research. We express that research with our opinions, and when the facts change, so too do our opinions.

Currently as we survey the global macro landscape, we see a number of markets making trails that both concern us and really inform our broader perspective. This morning I want to highlight three of those: the yield curve, the Swiss Franc, and copper.

1. The Yield Curve - Yesterday in our morning call, our Financials Sector Head Josh Steiner noted that the yield curve was narrowing to a point where banks were going to potentially see an impact on their earnings. Remember, banks borrow short and lend long, so as the yield curve narrows, so inherently do their margins. So it’s no surprise given this move in the yield curve that the financial sector ETF has been the worst performer of all the sector ETFs in the last three months (down 7.9%) and broken from both a Trend and Trade perspective.

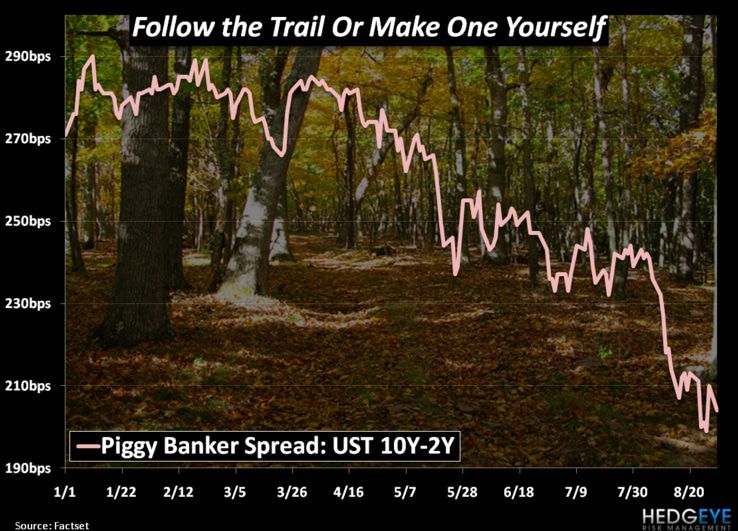

From a global macro perspective though, the yield curve narrowing is typically a leading indicator for slowing economic growth. When we analyze the yield curve, we focus on two durations specifically - 10s and 2s. In the parlance of the nonfinancial world, that is 10-year treasuries and 2-year treasuries, or as we like to call it, The Piggy Banker Spread. We've highlighted this point in the chart below, but the Piggy Banker Spread has narrowed dramatically through the course of the year from ~290 basis points at its peak to ~210 basis points now. This narrowing provides further support for our view that global growth is going to slow as it is a real time indicator for which direction long term rates are going, and the answer seems to be lower.

As a side note, we read with interest quotes from Thirdpoint’s Dan Loeb's recent letter to his investors (Dan, if you get a minute, please email us a copy). Dan's letter, from what we could tell, went off on the system being rigged and on government intervention generally. Admittedly, this is a point we have been very vocal on and it does worry us as we analyze and try to infer research information from markets that are managed by the U.S. government because, to be frank, we don't trust the Fiat Fools in Washington.

Nonetheless, the yield curve is a trail that is leading us to slow growth. For now, we'll accept that for what it is.

2. Swiss Franc - We highlighted this point in a note to our subscribers yesterday and want to re-emphasize it today. The Swiss Franc has had a massive move against the Euro in the last three weeks. In fact, the Swiss Franc is up over 7% in the time period (that's a big move in currency land) and is now back at levels not seen since the May time frame when everyone and their mother was worried about sovereign debt issues. Well, sovereign debt issues don't go away over night, or because of ECB interventions.

The rapid move in the Swiss Franc, in conjunction with widening of credit default swaps in Europe over the past few weeks, is signaling that we may be hearing and seeing more sovereign debt issues in Europe in the coming months. The explicit buying of the Swiss Franc and selling of the Euro is a direct vote against the Euro, and an attempt by those institutions with large currency exposure in Europe to hedge or protect the relative value of those European assets.

3. Copper - Dr. Copper over the past three months is up 9.9%, while its global commodity brother, Oil, is only up 1% on the same duration. This isn't surprising since copper inventories globally, most specifically measured by the London Metals Exchange, are at nine month lows. Moreover, based on normalized demand patterns and underinvestment over the past couple of years, we expect a global copper deficit next year for the first time in four years. Most importantly, this price divergence is a trail that is leading us to China. For the first time this year we are long China in the Hedgeye Virtual Portfolio via the etf, CAF.

Copper is verifying its trail this morning as it is up another 2.1%. That is not necessarily a surprise given the Purchasing Managers Index report from China, which is an indicator of industrial activity. This report saw a small increase sequentially going from 51.5 to 51.7. While this is by no means massive, it does indicate stabilization. In a country with 1.3 billion people growing at north of 10%, stabilization is perhaps all we need to be comfortable from a growth perspective.

Taken together these paths are leaving trails that we need to contemplate before our own portfolio trails.

I'm not sure if Ralph Waldo Emerson ever traded a P&L, but I'm guessing if he did he’d have an investment notebook, and his quote inscribed on the inside:

"A hero is no braver than an ordinary man, but he is brave five minutes longer."

Sometime that's all we need in this interconnected global market place, five minutes.

Yours in risk management,

Daryl G. Jones