With Q2 under our belts, we’re taking a look at the important Direct VIP business in Macau. Why didn’t Wynn’s share go up with Encore?

Direct VIP is an important part of the Macau marketplace, representing 17% of total Rolling Chip volume. The profit contribution is even higher. Instead of paying an average of 1.25% of roll to the junkets, the operators rebate only 0.7% to 1.1% back to the players. This results in a 1,200bps higher EBITDA margin from the midpoint given the differential. The American operators are the most successful in this segment, particularly LVS, while Macau’s largest operator, SJM, does not participate in Direct VIP.

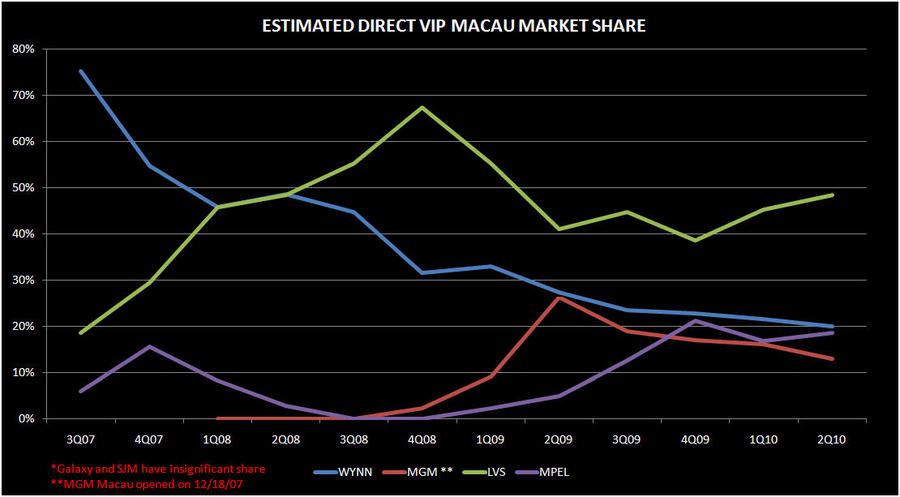

Following the end of earnings season, we are now able to back into the Q2 Direct VIP contribution. The following chart shows the market shares in Direct VIP.

LVS continued to grow its Direct VIP share – the only segment where its market share has grown. However, LVS recently announced it would be refocusing its efforts on the junket business so we would expect Direct VIP share to decline. The most puzzling market share move is Wynn. Despite the April opening of the predominately Direct VIP marketed property, Encore, Wynn’s share declined slightly in Q2. Combined with July/August overall market share sequential declines, Wynn’s Direct VIP share may further the narrative that Encore has not been additive. The next chart shows each company’s percentage of Rolling Chip volume attributable to Direct VIP. Again surprisingly, Wynn’s VIP % barely budged following the opening of Encore. MGM still generates a higher percentage of its RC from Direct VIP than Wynn, although this is partly due to MGM’s woeful junket performance.