NV will release July revenues in 2 weeks and we expect another mid-single digit drop.

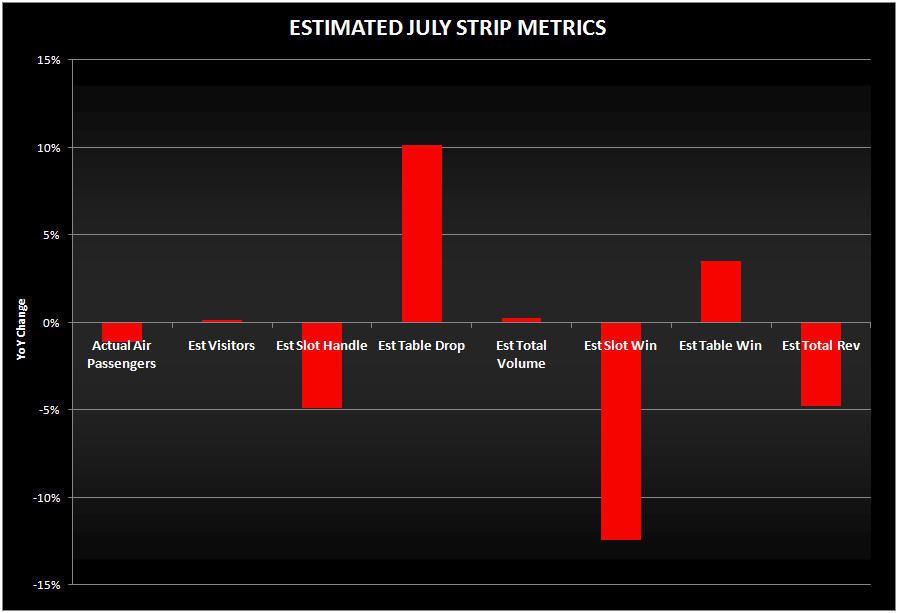

With McCarran Airport traffic declining 1.1% YoY in July - the same as June - we project Strip gaming revenue will again decline in the mid-single digits. Helping July is an extra Saturday in July of this year and a fairly easy comparison. Total gaming revenue declined 11% last year despite above average slot and table hold percentage. Hurting the performance will be the month end falling on the weekend.

Slots should be the laggard this month. Since the month ended on a Saturday, the weekend's winnings won't be factored in until August. Thus, we are projecting Strip slot revenue to fall 12% and total gaming revenue to decline 5%. If we assume the same high 7.4% slot hold percentage experienced last year, total revenue would be flat. However, due to the timing of month end, we are projecting only 6.6% hold. Normal slot hold is around 7%.

Here are the details of our projections: