We've extracted this chart from a post available to RISK MANAGER SUBSCRIBERS in its entirety and in real-time. To access this post and other research in its entirety, sign-up for a 14-DAY FREE-TRIAL or SUBSCRIBE.

_______________________________________________________

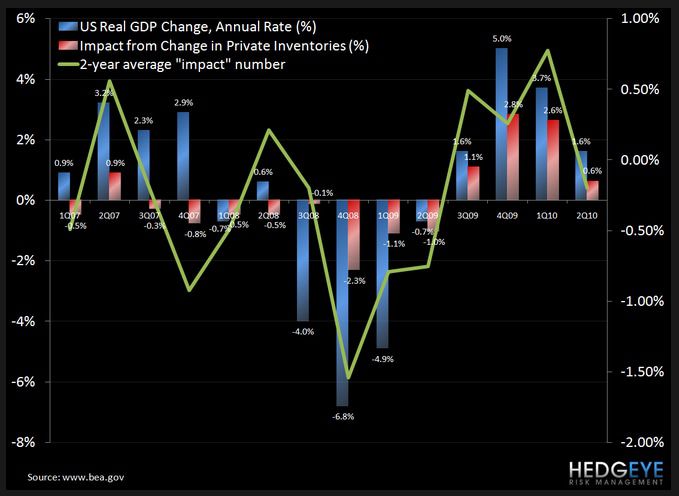

We have not published our official estimate for 3Q10 GDP growth yet, but suffice to say it will be substantially below the current 1.7% number and substantially below the 2.5% consensus for 3Q10.

Today’s made-up numbers from the commerce department suggest that the economy is in fairly bad shape.