Below is a chart and brief excerpt from today's Early Look written by Retail analyst Jeremy McLean.

|

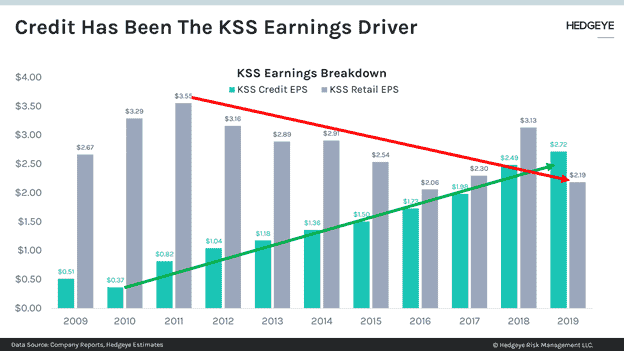

Recent retail results have seen credit declines, but retailers are citing lower card balances and lower fees as the driver from higher pay rates and less usage. Some seem to be signaling further declines, other recovery. Despite the uncertainty on how this will play out, this week KSS’s CFO gave what we would consider overly certain commentary on its credit business, implying it will track in line with sales and hinting that sales should make a big recovery towards 2019 levels in 2021. We’d suggest investors take that with a grain of salt and treat the credit outlook to be highly uncertain. We think the most probable outcome is the one supported by historical results and our deductive reasoning, which is that many jobs are permanently lost, and eventually that will lead to countless cardholders that can’t pay their bills, as has been the case in every prior recession. Yesterday’s jobless claims report showed we are not out of the woods and Hedgeye US Macro Analyst Christian Drake has highlighted the impending year-end income cliff. Still, a crash in retail credit income is far from certain. If we do see recessionary levels of credit card defaults in the coming quarters, we think several credit exposed retailers like KSS and GPS will make great shorts as the market is assigning a very low probability to that scenario. And if we’re wrong, there will still be plentiful ways for us to make money on both the long and short side of retail ideas, so we can get back on the birdie train. |