“Never stand begging for what you have the power to earn.”

-Miguel de Cervantes Saavedra

This is an important quote from one of Western literature’s most important authors. Cervantes wrote Don Quixote in two volumes (in 1605 and 1615) and to this day it is regarded as one of the greatest fictional works of all time.

Wikipedia summarizes the Cervantes central characters well: “Don Quixote is noble-minded, an enthusiastic admirer of everything good and great, yet having all these fine qualities accidentally blended with a relative kind of madness. He is paired with a character of opposite qualities, Sancho Panza, a man of low self-esteem, who is a compound of grossness and simplicity.”

As we prepare to hear the proclamations of Fiat Faith from our central planners in Jackson Hole, Wyoming this morning, we must realize that the developing story of Sancho America is far from fiction. Consumer and small business confidence in this country is abysmally low and the causes of the slowdown in US economic growth are being grossly misrepresented by both the US government and its dogmatic economic advisors.

The “grossness and simplicity” of it all is now being compounded by the world YouTubing us for who our professional politicians have become. When the most compromised and conflicted of all central planners in the world (Japan) launches into public attacks on Americans being “simple” and “single-celled organisms”, folks we have a problem.

Those are Ichiro Ozawa’s quotes. He is challenging the current Japanese Bureaucrat in Chief, Naoto Kan, to an election in Japan on September 14th. The battle lines have already been drawn. This economic disaster of a Japanese quantitative easing experiment provides for a proactively predictable political debate.

Never mind whether his challenger’s platform is calling America a modern day Sancho Panza, there is only one question that matters here. It’s the same question that the Fiat Republic of Japan has been asking of its countless PM’s since Paul Krugman talked the Bank of Japan into “PRINTING LOTS OF MONEY” in 1997. After only 2 months on the job will the current PM of Japan lose his job to an antagonistic charge that he isn’t doing more of what hasn’t worked?

What hasn’t worked in Japan is government “stimulus spending” that is financed with borrowed money (government debt). This week, the Japanese sold 1.1 TRILLION Yen in 20-year debt in order to ostensibly give Naoto Kan that last heroin shot he needs to give his citizenry another enema before the election.

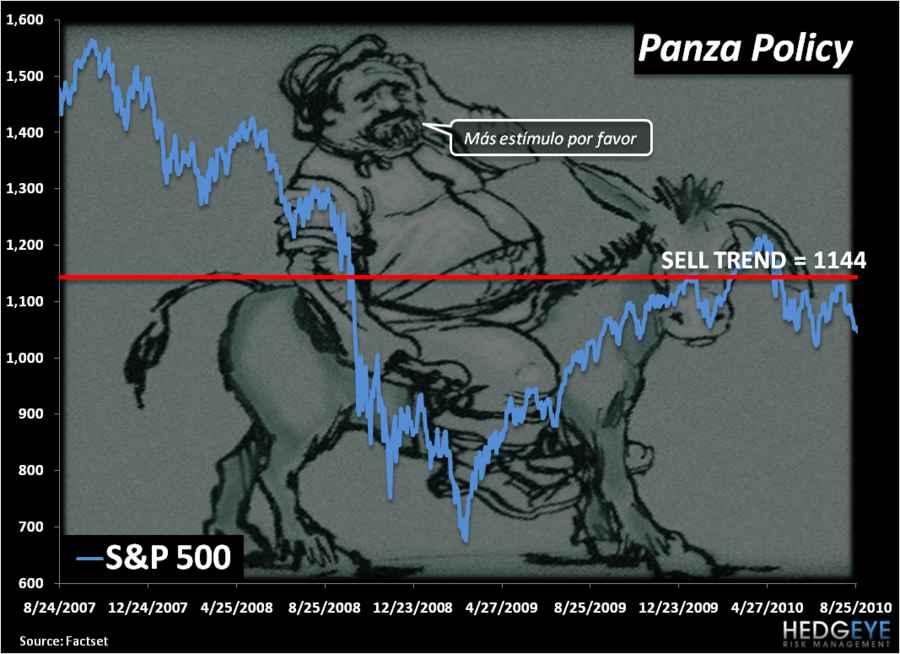

All the while back in America we have our own Panza Policy that will be pandered to, big time, in Jackson Hole as the czars of ‘government is good’ throw down the gauntlet of their long-standing, fear-mongering, marketing message to the American people.

This morning, Paul Krugman has already accused the US government of “sugar coating” the messaging about the recovery. This must me some sad and sadistic attempt to make sure that the fear-mongering messaging that leaves America effectively begging Bernanke for free moneys remains Washington consensus.

Never mind empowering American independence and confidence. Out with the grind and grit that makes the great leaders on this country’s fields of battle earn the world’s respect. Bring in the government - it’s the elixir you need – debt financed spending will give us all “the power to earn.”

I wish I was coloring Krugman unfairly – I really do. Sadly, the alternative to believing this man doesn’t have an impact on how Bernanke thinks is also fiction. In the flesh, here are the 2 comments that were most alarming to me in his New York Times editorial this morning:

- “This isn’t a recovery, in any sense that matters… and policy makers should be doing everything they can to change that fact.”

- “We’ve already seen the consequences of playing it safe, and waiting for recovery to happen all by itself… It has landed us in what looks increasingly like a permanent state of stagnation and high unemployment.”

Alarming, yes. And being blunt about the economy being a mess isn’t what alarms me. It’s A) the misrepresented cause of the mess and B) the dogmatic solution to this mess that makes us trust government so little.

If Americans think that the answer to this Failed Fiat Experiment is empowering government to compound their Japanese spending and quantitative easing mistakes, this is not the United States of America that we used to be.

Put on our cowboy hats in Jackson Hole and pretend you are patriots. Begging for Bernanke and stimulus will have no power in earning this simple man in New Haven, Connecticut’s respect.

My immediate term support and resistance levels for the SP500 are now 1038 and 1070, respectively. I continue to register lower-lows of support and lower-highs of resistance on both the US Dollar and the US stock market. Stocks are down -14% since April and down -33% since 2007. These markets don’t lie folks, politicians do.

Have a great weekend and best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer