Dear Hedgeye Nation,

What’s the big investing takeaway this week? Don’t let your politics into your portfolio.

The big “Blue Wave” on Election Day narrative never materialized. It caught Wall Street completely offsides. As our subscribers know, we’ve been on the right side of financial markets—not by guessing Election Day results, but rather by adhering to our data dependent Macro process.

On that front, Hedgeye CEO Keith McCullough just hosted a free edition of “The Macro Show.” Keith discussed the bigger picture macro trends driving financial markets and how to position your portfolio to take advantage of them.

Here’s a key insight from Keith on today’s show:

“Let’s take the VIX. It went out just north of 30. Anytime the VIX is north of 30 and rising Captain Stockpicker dies. Their stock picks don’t work so well anymore. Equally important is when volatility breaks down below 30. Captain Stockpicker gets a bid.”

Below we’ve transcribed for you critical excerpts from today’s Macro Show. Watch the rest of the 31-minute investing masterclass with Keith McCullough below!

Keith McCullough: Thank you all for joining us this morning. The top three things in my notebook are the Dollar, #Quad3 and an epic move in the bond market.

First, on the Dollar. The Dollar has been going down for a while now. Our model went bullish and then went bearish. We use math to determine whether we’re bullish or bearish on the Dollar.

The only time you should be bullish on the Dollar is when we’re in Quad 4. That’s an environment in which U.S. growth and inflation are slowing at the same time. I will get to why we’re not in Quad 4 and we’re in Quad 3, an environment of growth slowing and inflation accelerating.

But before we get to that, the only big bet that we had going into the election is that I wanted to short Dollars and be long inflation. That’s Quad 3. That’s long Commodities. Tech is a long in Quad 3. That’s what’s really happening this morning. The U.S. Dollar is down hard. Our Swiss Franc (FXF) long position is doing quite well alongside my Bitcoin.

It’s a good morning if you can put bets across the global Macro table as opposed to CNBC which is perma-long stocks. That’s not any fun.

That’s the second point on Quad 3. What happens in Quad 3? Bond yields go down. The Dollar goes down. Tech goes up. Commodities go up. Cannabis stocks go up. Anything growth goes up. Why? Because growth is slowing.

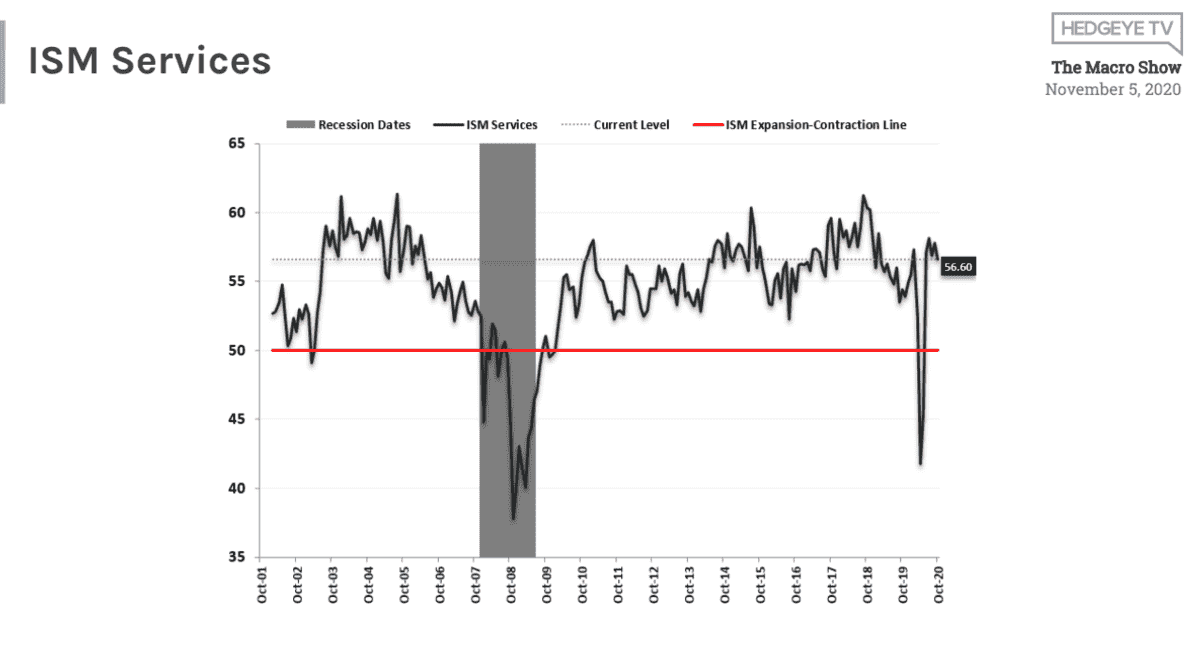

Unbeknownst to the Robin Hoodies or HODLers, they don’t know what’s happening in the bond market. Two of the biggest things that matter in the U.S. economy are employment and consumption. The ISM Services hit the lowest level since May. The bond market said, ‘Holy s#!t, that’s terrible.’

And by the way, COVID is accelerating. So COVID accelerating is not good for future employment growth and it’s certainly not good for the Services economy into November.

That’s what the bond market figured out yesterday. Which gets us to point number three in my Macro notebook this morning. This is one of the biggest 2-day moves ever for the bond market. Ever is a really long time. Remember on Election night around 8 o’clock when everyone started to say, ‘Look at the bond market it’s collapsing.’ From that point in the 10-year Treasury yield, it’s down literally about 20 basis points in 48 hours. I’ll say this again. That’s one of the biggest percentage moves ever.

That is the bond market telling you that we’re not going to Quad 2, an environment of growth and inflation accelerating at the same time. In that environment, you’d be shorting Gold and Treasuries and buying Financials (XLF). The Financials got walloped yesterday. Regional Banks (KRE), which I’m short, was down -6% on the day. The market got it right. When you’re in Quad 3 you do not buy the Financials.

Those are your top three things.

McCullough: After we do the top three things I go into the set-up in our Risk Ranges. Let’s get into it. So we have this thing called “instantaneous volatility” – what’s happening right now. What do you do right now? No matter what you did yesterday, you have to deal with now.

The Risk Range on the S&P 500, using yesterday’s closing price, is 3220 to 3496. So essentially the market is going to go right up to the top end of its range on the open. There are a lot of investors that will transact at the top end of the risk range – at the edges of uninformed volume – because they just don’t know better.

Don’t forget that yesterday’s close relative to the downside of 3220 in my range is -6.5%. Add in another 1.5% to 2% upside to the top end of today’s S&P 500 risk range and you’ve got even more downside. What do you have on Friday? Guess what? There’s a Jobs Report on Friday. And guess what? The ADP report was half of what expectations were.

Don’t get so sucked into what’s happening right now and act viscerally or emotionally or politically. Don’t do that to yourself. Deal with what you’ve got and try the best you can to embrace the uncertainty that you don’t know for sure what’s going to happen tomorrow. But you do know what the probabilities are setting up to be.

McCullough: This is really important. Let’s take the VIX. It went out just north of 30. Anytime the VIX is north of 30 and rising Captain Stockpicker dies. Their stock picks don’t work so well anymore. Equally important is when volatility breaks down below 30. Captain Stockpicker gets a bid.

The Risk Range on the VIX is 27-41. What happens if volatility rips up to 41? The S&P will fall to the low end of the range. It’s that simple.

So when people say, ‘You can’t time markets.’ Believe them. They can’t. But you can. You can probability weight the timing of markets, which is a much more appropriate way to think about it, upside to downside.

Think about Blackjack. If you want to hit on a six all day, you can do that, but it’s just stupid. You don’t want to buy at the top end of the range and sell at the low end of the range.

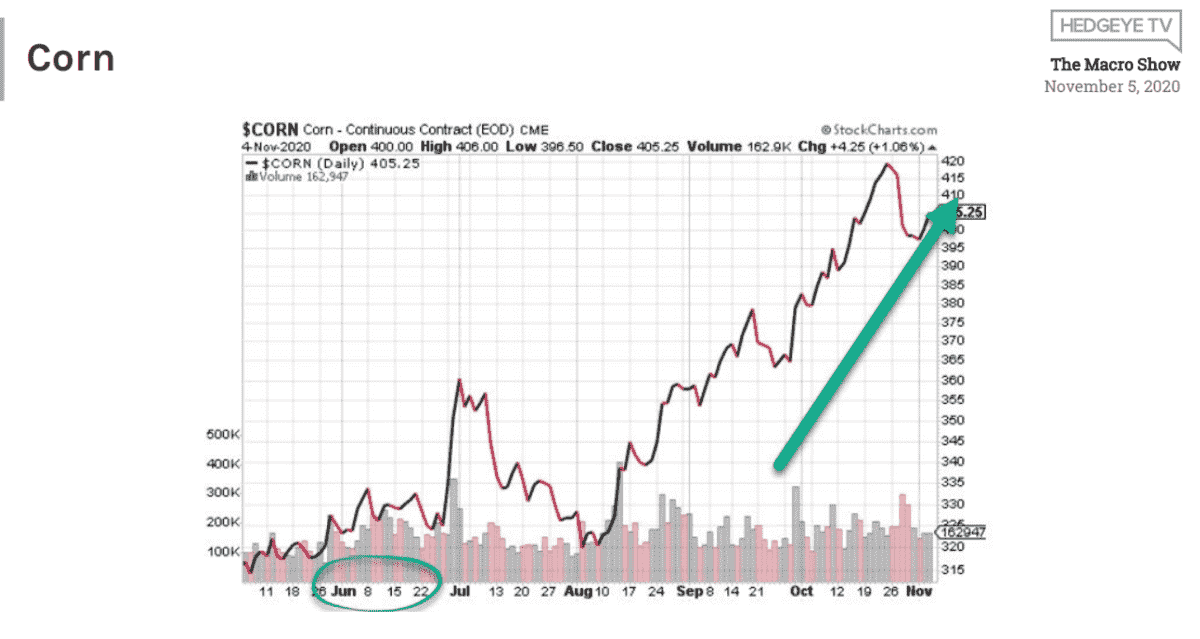

So while Wall Street flounders around with their stocks, why aren’t they long Commodities? Look at Corn. I’ve heard a lot of Wall Street types say, ‘There’s no inflation out there.’ Well, just don’t tell the no-to-low income people that because they’re going to have to eat it.

That’s why it makes me uncomfortable to be shorting Dollars and buying commodities like Corn, Wheat and Soybeans. The people in Bridgeport, Connecticut that don’t have a job are going to eat it. They’re going to pay for rising inflation in a higher cost of living.

Daryl Jones: Here’s the top question in the Q&A from Karen in South Carolina. “REMX, XLK, QQQ are longs now based on the Early Look but they have ripped since yesterday. Is it too late to buy a small amount now or should we wait until another correction which might not happen anytime soon?”

Basically, we’ve had a few long calls that have worked over the past couple days. So thinking about risk management, if you’re not allocated to those how do you think about it from here?

McCullough: Karen, I’m totally with you other than, ‘the correction might not happen soon.’ When everybody thinks there’s not going to be a correction, that’s when the correction happens. The best way to think about this is to not have FOMO.

Don’t forget that I just gave you a Full Investing Cycle, go-anywhere investing strategy. Thank you for mentioning Rare Earths (REMX) or yesterday you could have bought Soybeans (SOYB). Once you realize that there’s always something at the low end of the Risk Range for you to buy that will get rid of your FOMO.

Once you and everyone else thinks you’re not going to get the low end of the Risk Range, you’re closer to the point in time where everybody realizes the low end of the Risk Range. It’s called mean reversion and it happens all the time.